Sure, there are better systems in privacy terms. However, the bigger story is that the world is changing fast: a huge percentage of the world's population - in China - now lives a reality of instant mobile payment. If you accept that the general population will always gravitate toward functional, reliable, cheap, centralized payment systems unless they have specific needs such as anonymity/illegality, and that those systems are improving rapidly in features and distribution, then the real challenge to future decentralized currency is getting anyone to give a damn.

I still don't understand what problem decentralised currency is supposed to solve.

As you say, I want cheap, convenient transaction at low cost, and specifically concerning privacy I want to know who I send my money, and I want legal recourse should anything fishy happen.

The privacy proposal of crypto in my opinion is bizarre. I am supposed to lay out my entire financial history in a public wallet (which I don't want), but trade with people who I don't know (which I don't want), and have all of it supervised by 'smart contracts', which are anything but smart and make it necessary to essentially put myself under surveillance?

The problem it solves is that it enables two parties to exchange digital values automatically and without interference.

The problem manifests itself in full view in situations where citizens are asked to leave their money or possessions in a country before they are allowed to leave or in situations where the inflation rate makes surviving on a fiat currency next to impossible (ie: Venezuela).

In the western world, the problem of interference in your ability to do commerce with whoever you wish might be harder to detect but just recently SWIFT decided to enact the US government's capital controls on Iran for EU companies, despite the EU having declared they would stand by the agreement... For a EU based company or individual there is now very little chance to do legal commerce in Iran, Venezuela, Cuba, North Korea, Syria, Myanmar and a few other countries because of the US's influence on the money markets.

There are many problems cryptocurrencies solve. You can make a list just by noting where actual turnover in the real-world crypto economies goes in practice:

* How do I receive payment for illegal goods I am selling without going through traditional regulated entities that want to attach my real-world identity to the payment in their records?

* How do I provide gambling services to customers in jurisdictions that prohibit this?

* How do I profit from people willing to put their money into transparent pyramid schemes or straight-up scams, without risk of recourse from traditional police / legal systems?

* How do I launder money?

* How do I skim from the shadow economy i.e. in entities engaged in all of the above activities, without committing an obvious crime myself?

Legal oversight can be an unwanted transaction overhead that introduces risk, and laws restrict freedom.

Ask instead what problems decentralised currency is supposed to solve that are legal and moral to solve and cannot be solved more cheaply through traditional systems involving a regulated third party subject to the rule of law.

Lets list them by assuming that I want to buy a legal product or service:

* When it is cultural and social taboo.

* When the act can be pulled out of context.

* When it can become a false positive for correlation in police investigation.

* When it can be abused in order to influence and apply pressure, by example advertisers, politics or different sides in a court.

* When it can harm a third party, like a dependent.

* when it can give unfair market power to those who know more about you than competitor with better product or service.

All of those have some grey zones and illegal areas but for most it is up to the consumer to be aware. So long the legal system demand that the individual take responsibility for personal information, and the legal investigation system has false positives, and the court and political voting system depend on asymmetrical information, and influences like advertisement is legal, and we have cultural and social taboos for legal behavior, well then we have a legal and moral problem that a decentralized currency could help to solve.

While there is some truth in your argument, you are very clearly only focusing on one-side.

The problems that crypto-currencies attempt to solve are more to do with monetary policy. E.g. - you can't have things like quantitative easing / manufactured inflation if your money supply is dictated by a tightly controlled algorithm.

Whether or not that is a desirable overall policy is a wholly separate argument.

>The problems that crypto-currencies attempt to solve are more to do with monetary policy. E.g. - you can't have things like quantitative easing / manufactured inflation if your money supply is dictated by a tightly controlled algorithm.

If that's what you want... the extralegal aspect of cryptocurrencies is a big problem. I still have a few hundred bucks tied up in e-gold, which was perfectly setup to do what you want, and backed by real gold, but as a side feature was also convenient for black market transactions.

The bitcoin supply is increasing, at high, but shrinking rates, however its purchasing power is still increasing despite that inflation.

This suggests that demand for bitcoin is exceeding the supply rate.

If the demand continues, and the supply rate of bitcoin will be almost exhausted in a couple of decades, then the value of bitcoin will likely rise in response.

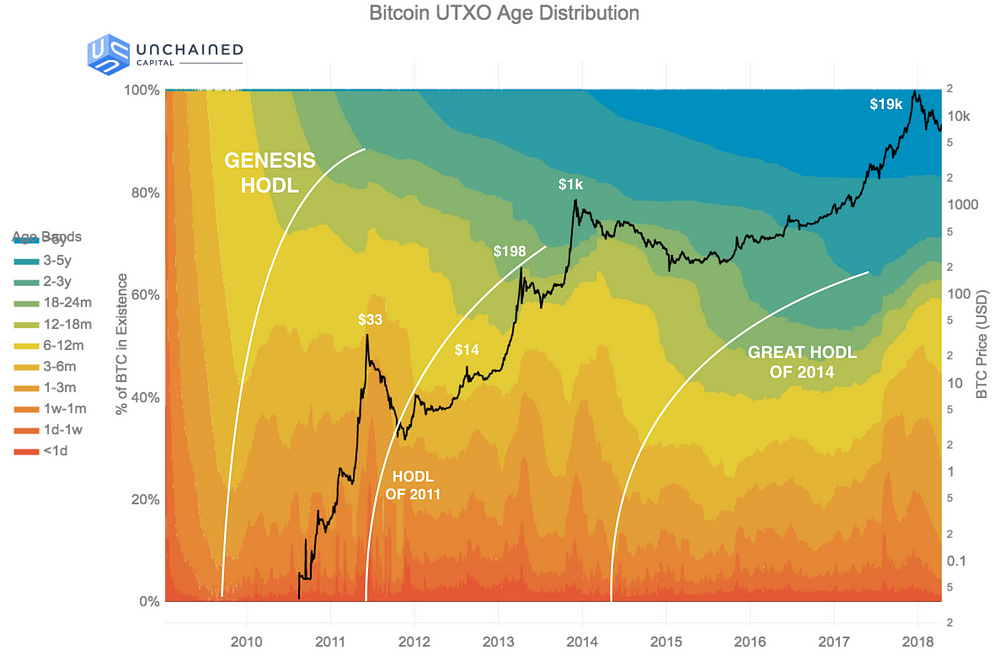

This is of course, ignoring that volume of bitcoin in circulation is actually shrinking with time[1], because people are hodling rather than trading it. Evidence that Gresham's Law is playing out as usual.

> You do realise that Bitcoin is experiencing much more inflation in its supply than the USD or the EUR, don't you?

So, I argue that it seems likely this would happen; someone will figure out how to fractional reserve the stuff, the gain is too great. But do you have evidence that it did happen? what was the mechanism?

> someone will figure out how to fractional reserve the stuff, the gain is too great. But do you have evidence that it did happen? what was the mechanism?

If the transaction is not on the blockchain or is not directly tied to a blockchain transaction (like with LN/payment channels), you MUST assume there's a fractional reserve going on, as you have no way of confirming otherwise.

If it is tied to the blockchain, it can't be a fractional reserve.

Fractional reserve is not about transactions, but about backing for the underlying assets these transactions are "moving".

LN/payment channels are payment methods (think checks or credit cards), while traditional "cryptocurrencies" are systems or records or ledgers (think banks).

The assets are fiat cash and cash-equivalents (electricity, hashing power) inflows. I.e. when somebody mines or buys Bitcoin - money flows into the system, when somebody sells Bitcoin - money flows out of the system. So most cryptoassets today are fractional reserve.

But my impression was that actual blockchain transactions were cumbersome and slow to verify, and that most people, especially most investors, have some other party holding their coins or otherwise invest indirectly.

I know this is true when the debt is issued by the currency issuer & denominated in that same currency, such as in the case of the United States.

Is that also true in the case of say, Italy's debt denominated in Euros or Illinois state debt denominated in USD? I have been meaning to read Steve Keen's work on this

the 20T will have to be paid back. Unlike personal debt the fed can just print the money. There is currently around 6T in existing money supply (though I havent checked recently).

The question is how will the debt translate to increased money supply over time (inflation).

> Unlike personal debt the fed can just print the money.

A part of why the Fed (and the same is generally true of independent central banks generally) exists (and why the Fed system is comprised of large private banks) is to provide a check (and, more important, confidence among lenders) against Congress simply monetizing the debt by separating the locus of decision making for monetary policy from that for fiscal policy.

Historically that often doesn't really happen with such debts. Instead the debt falls a percentage of GDP due to GDP growing, at least in nominal terms.

>Inflationary economies can survive in the long term

Is this true? I only know western history, but between Rome and every successor state, inflation is a short term fix and usually leads to the end of a government and currency(over centuries)

Because a dollar is not always worth a dollar. A bitcoin is always worth a bitcoin.

The dollar doesn't have a "reference rate," as it is subject to arbitrary inflation. The dollar has had several reference rates in the past, based on weight in silver, and later, gold. The purchasing power of a dollar has declined rapidly since these reference rates were abandoned.

A bitcoin has a reference rate which is eventually 1 in 21M. There is an initial inflationary period until it reaches that, but we're already 1 in ~18M, so most of the inflation has already occurred. We will be very close to the 21M in another 13 years, and after that we will only be adding small fractions.

If you had a dollar in 1918, it would be worth only a small fraction of a dollar today. 1/16 or 1/40, depending on what estimations you use.

If past performance is anything to go off, then a dollar in 2118 will be worth 1/16th of a dollar today. If you hold onto 16 dollars today, they will have the purchasing power of 1 dollar in 2118.

On the other hand, if you hold 16 bitcoin today, you have 16 of 18M of the bitcoin supply. In 2118, you will have 16 of the ~21M total supply.

In the same 100 years, bitcoin will inflate by most 16%. The dollar will inflate by 160% in the same period, if the past century is anything to go off (it isn't, this century will be much much worse).

Or put it in to shorter timeframe. If inflation is approximately linear over the 100 years, then every 6 1/4 years, your bitcoin will lose 1% of its purchasing power. In the same timescale, your dollar will lose 10%.

Which of these are you going to save money with?

The above is based on the assumption that demand for bitcoin will not increase in relation to demand for the dollar. Given Gresham's Law, this is highly unlikely.

That only pins the value of a bitcoin in relation to other bitcoins - it does nothing to pin the value of a bitcoin to real-world goods. And the only practical value of a bitcoin, in the long run, is its value in relation to real-world goods.

It's also worth remembering that once the inflation of bitcoin stops at the 21m mark, it can only ever deflate from there as wallets (and their associated coins) are lost. As bad as inflation is, a deflating currency is not any better.

Of course, the proposed solution to bitcoin deflation was (at least at one point) just to inflate the bitcoin currency by effectively moving the decimal point to the right (one bitcoin becomes 10, etc).

> That only pins the value of a bitcoin in relation to other bitcoins - it does nothing to pin the value of a bitcoin to real-world goods.

This is true, but it's also true for dollars. No goods are inherently pinned to a dollar value. Goods are priced in dollars with the expectation that the seller will earn a profit if sold at a given rate.

But if that dollar loses its purchasing power, mostly due to it being inflated by central banks, then the price of goods in dollars will have to increase for the seller to earn the same profit. It is not sufficient for the seller to just increase their goods at the rate of inflation either, because the cost of all their expenditures increases too. To earn the same profit after inflation, they need to increase their revenue more than the rate of inflation. This has a ripple effect over all industries.

On the other hand, if the non-inflationary currency is not losing its purchasing power over the same periods, then merchants will prefer to obtain the non-inflationary currency over the inflationary one. If they obtain both, they will use the inflationary currency first to purchase new materials, and only dig in to the non-inflationary currency as and when they run out of the inflationary currency.

If eventually, businesses decide to price their goods in bitcoin, rather than the dollar amount of bitcoin at the current market exchange rate, then they might be able to expect that they will not need to keep raising prices annually for inflation, but might instead be able to lower them, or keep them at the same rate and increase their profits for as long as a cheaper competitor does not appear. However, if these goods are priced both in bitcoin and USD, then while the bitcoin value remains the same, the dollar value must continue to increase for inflation.

Since bitcoin also enables a certain level of transactional privacy too, it will also be used for grey and black market transactions, which make up 10-20% of economies. Most people interact either directly or indirectly with these markets for saving money or generating additional profit. Cash has traditionally been used in these cases, but as the effort of states to make money digital, under mass warrantless surveillance increases, the practicality of using cash decreases. Bitcoin is well suited to fill the gap being created.

> As bad as inflation is, a deflating currency is not any better.

I often hear strawmen arguments against deflation, but never any real sources or evidence of how terrible it supposedly is. I'm led to believe that people won't spend money in a deflationary economy, but peoples need to eat and drink suggests otherwise.

An example of deflation in action is in Moore's Law. If I buy a computer now, it will be half as powerful in 1.5 years. Why would I not just wait 2 years and buy a computer then? People continue to buy new machines all the time, and they don't wait 2 years for the next iteration, because they know that in another 2 years, that one is out of date. People will spend for as long as they perceive the transaction is worthwhile now for the labour effort they put in to acquire that amount in currency. In a deflationary economy, people simply make better decisions, because they're not simply comparing the amount to what they earned recently, but in any significant transaction they need to weigh the importance of the transaction against their future self.

I think the real complaints about deflation are from socialist types who worry that the rich will get richer. Too bad for them, they can't prevent this any longer. The state no longer has the capacity to steal people's bitcoin if they take the right measures to secure their keys. The rich might get richer, but anyone can get better off if they shift to a low time-preference mindset, instead of being stuck in the debt spirals that are encouraged by high time-preference economies.

> Of course, the proposed solution to bitcoin deflation was (at least at one point) just to inflate the bitcoin currency by effectively moving the decimal point to the right (one bitcoin becomes 10, etc).

The "bitcoin" denomination is really just cosmetic anyway. All of the values in the bitcoin protocol are measured in satoshis, as a 64-bit integer. It is not trivial to change this denomination as it would affect the entire UTXO set of transactions. On the other hand, moving the decimal place for the cosmetic appearance of satoshis could be trivial, but it doesn't change much.

Dollars have one major advantages over bitcoins (in the US): They are legal tender for paying all debts, private and public. Bitcoin requires the merchant to accept bitcoin - something they are not, and will never, be required to do.

Bitcoin also has a cost associated with it that the dollar does not - a transaction processing cost (yes, there are costs for the handling of money, but it's both significantly less than bitcoin transaction costs, and is relatively constant).

WRT deflation, the biggest problem (that I'm aware of) is that it disincentivizes spending, something generally considered to be a bad thing for the economy. Sure, people may buy the necessities with a currency that is deflationary, but they're disincentivized by the currency itself to do anything more than that.

In other words, why would anyone (not just the rich) spend more than the bare minimum when not spending means their net value increases?

Any form of investment that can't accrete value faster than the currency itself becomes a wasteful product. Stocks, bonds, houses, cars, bicycles, startups, family businesses, education - all have the potential of losing all their value when compared to hording currency.

> Dollars have one major advantages over bitcoins (in the US): They are legal tender for paying all debts, private and public.

This is true, but the practice is such because the government has previously granted a monopoly on the issuance of money to certain private entities which have little accountability to anyone. Previously, it was not possible to compete with this monopoly, because the state enforced it through the threat or use of violence.

The money issuers now have competition, and the government has no way of "shutting down" the competition due to the way it was designed. Merchants now have alternative options in terms of what currency they're willing to accept and how they can save money, rather than simply spending.

If it happens that the new competition is more desirable to possess than the previous money (due to lack of inflation, meaning it is more likely to retain its purchasing power in the long term), then people will save in bitcoin, and spend in dollars.

The result is that a large amount of wealth will essentially "disappear" from circulation which the state thugs can levy taxes on via use of violence. Economies will take a hit as a result, but the people saving in bitcoin won't be impacted as heavily as those who don't. In fact, it could have the effect where each hit taken by a national economy drives more people to bitcoin, pushing up the demand and value, making those who were smart enough to accumulate it earlier even more wealthy than before the economy took the hit.

As long as there are liquid enough markets (whether those are AML/KYC compliant, or black-market) for people to trade some of their bitcoin back into USD for the purpose of paying taxes, then the dollar is not going to retain its advantage.

> Bitcoin also has a cost associated with it that the dollar does not - a transaction processing cost (yes, there are costs for the handling of money, but it's both significantly less than bitcoin transaction costs, and is relatively constant).

Transaction fees in bitcoin are not consistently high. Some fees were high last year due to the sudden increase in speculation, poor fee estimation in software, and services which were not making efficient use of block-space, at their own cost, or the cost of their clients. Much of this has improved, although we have a long way to go.

The main developments are in the more scalable technologies pinned to bitcoin, which aren't competing entirely for a share of the limited block space. Fees on the lightning network, for example, have a base rate in satoshis (per transaction), and a proportional fee of 1 millionth the value transacted. The fees total fractions of cents. Bitcoin transaction fees are only paid in the creation and destruction of payment channels, which may be very infrequent.

> WRT deflation, the biggest problem (that I'm aware of) is that it disincentivizes spending, something generally considered to be a bad thing for the economy. Sure, people may buy the necessities with a currency that is deflationary, but they're disincentivized by the currency itself to do anything more than that.

The reason that reduced spending is seen as a "problem," is because governments can't cover the interest on their debts unless people are actively spending and paying taxes on those transactions. Governments are not really paying their debts off - they're paying off the interest, and kicking the can down the road even further. The debt will never actually be paid. It is impossible to pay off. At some point, who knows when, your government is going to default. This is inevitable.

> In other words, why would anyone (not just the rich) spend more than the bare minimum when not spending means their net value increases?

People spend because they want something, and they're willing to let go of something else which they value in exchange. For some that might be the bare minimum. For others, they might want to continue wealth-signalling with expensive cars and watches.

Think about that one. The value of that car depreciates by about 20% immediately upon purchase, and then by a further X% every year. It has a lifetime of around 10-15 years before it is basically worth the value of its scrap metal. Yet people are still buying cars frequently. Could it be that people still spend money on products and services which provide them value now, and not just save everything like the deflationary scaremongers suggest?

> Any form of investment that can't accrete value faster than the currency itself becomes a wasteful product. Stocks, bonds, houses, cars, bicycles, startups, family businesses, education - all have the potential of losing all their value when compared to hording currency.

Some of the examples you pick, like cars, bicycles, houses (sometimes), actually depreciate in value over time, which throws away the argument that people won't spend money if they don't see a monetary ROI.

Consider renting a home as another prime example. People will continue to put money into an "investment" which will eventually net them zero return when they move home or get evicted. Yet people still rent.

Many "investments" are simply full of rent-seekers who do not provide any real value to society. If people stop throwing money at these, it won't be missed.

Education is an example of something we can't even measure the ROI on. We just know from observation that the better educated a society is, the higher its productive capacity appears to be a few generations down the line. We also know that some academies do a better job than others, and that some people are willing to pay more to have their children educated at those academies, with no guarantee that they will see a ROI. (The child could turn out rebellious, or just not smart anyway). People still invest in education despite there being no obvious profit motive - their child's future is more important than the value of the money.

The real difference in investment when it comes to deflation is that people simply make better decisions. The incentive is skewed more towards saving than spending, but this is not absolute. People will spend, but think twice about buying that useless gadget that they didn't really need, but they bought on impulse because they had $1000 burning a hole in their pocket.

The argument against deflation is essentially the same as saying "people won't save money if there is inflation," because money is depreciating over time. The incentive is towards spending, but people still save money. The only time they don't save is during hyperinflation, when the value of the money depreciates more rapidly than they earn and spend it. The reverse is true for a deflationary economy. As long as deflation is low, people will still spend, but with more preference to save. It is only if hyperdeflation occurs that people will "hodl" and only spend the bare minimum to survive. Hyperdeflation will occur as bitcoin gains adoption, but it is not the eventual state. Once peak adoption has occurred, the rate of deflation will begin to decrease, with the eventual state that it will be relatively stable. In the even longer term, bitcoin could become inflationary by accident, if the human population as a whole begins to decrease rather than increase - because demand will be reduced.

The inflationary money is bad in comparison to the non-inflationary money, because the inflationary money sees people's purchasing power lose value from the labour they underwent to acquire the currency, over short terms (a few years). The non-inflationary money however, sees people's purchasing power remain the same as their productive effort to acquire it, if not, increased from when they obtained it due to deflation.

When two forms of money exist and one is better than the other, people will save the better money and spend the worse money.

People do save with currency, usually in limited amounts or limited times, in large part due to its inflationary nature. Inflation forces a high time-preference on labour because the non-spender loses value over time. Putting money into stocks is not the same as saving, but it is investment, with varying degrees of risk. None are guaranteed to even preserve value, let alone profit. At present, Bitcoin behaves like a stock because its value wrt USD is so volatile.

Gold is only valuable because of it's perceived scarcity and historical use as a store of value. It is not priced so highly due to its intrinsic properties as a metal (it is neither that useful nor that scarce), unlike some other commodity metals.

Bitcoin is the digital equivalent of gold. Its value is based on scarcity and perception of value due to the ability to find someone who will trade it at an expected market rate for other currencies or for goods.

(3) It is better to encourage saving than to encourage spending.

(4) Bitcoin is a better non-inflationary currency than gold.

1 and 2 -- sure, agreed.

3 -- This is the most important part of your argument yet you have not explicitly stated it, nor argued in favor of it, anywhere. It is unclear to me why it's good policy not to encourage investment.

4 -- You are right that neither bitcoin nor gold has intrinsic value (not counting the value that gold would naturally have as an industrial material). Both are only valuable because other people perceive them as value.

However, people have perceived gold as valuable for thousand s of years. The fact that gold has value is deeply rooted in human culture and therefore not likely to change in our lifetime.

None of that is true for bitcoin.

So, what are we left with? The only advantage of bitcoin that I can discern in all of this is that it can be transferred via the internet in a censorship-resistant way. I do not think that advantage is important enough for most people to outweigh the disadvantages.

I would modify (3) to say: It is better to encourage saving than to encourage spending on useless shit that won't last.

The problem with today's "investment" is that it is almost entirely on shit that won't last, and is for the purpose of short-term monetary gain than for investment into infrastructure which will last generations. An "investment" today is concerned with the next quarter, 6-months or perhaps even a year. Most companies do not concern themselves with anything longer than 3 years, or anything to do with the well-being of the societies in which they operate. Most companies simply can't operate on the time-scales needed to build and eventually profit from creating infrastructure. Instead of building something with the intent of breaking-even in 10 years, one will instead still be paying back interest accumulated on loans taken out 10 years ago.

The end result is that the role of building infrastructure in developed nations is now almost entirely assumed by governments, or contracted by government, which ends up creating virtual monopolies propped-up or subsidised by the state. Private companies which are profiting hugely from public money, but do not operate like regular companies because they don't have to compete with anybody and have little accountability. It's the worst elements of socialism and capitalism combined into one package.

In the academies, research projects which span 3+ years are now almost unheard of. It's more important to get 3+ publications per year, now matter how garbage they are, else the funding won't come around next year. We're seeing stagnation in many areas of science because research which is not short-term profitable is ignored.

For most of the working and middle classes, the high time preference results in them buying useless gadgets, largely for the purpose of wealth-signalling, eating junk food, getting wasted, anything to fill the requirement to spend the money one has earned, because it is not worth saving the money. For many, paying rent is preferred to buying property, because the latter requires saving to achieve, which is hard when people see their stored value decaying in their bank accounts.

The shift from inflationary money to non-inflationary money will fundamentally affect people's decision making in their purchases. It isn't going to happen overnight, but as people realize they can accumulate wealth without risky investments, they will come to value saving over spending. The companies producing cheap junk for short-term profit will have to change the way they operate to fit the changes in spending habits.

On (4), gold is still inflationary as new sources can be uncovered. It is better than fiat currencies which can be arbitrarily inflated, but it is still worse than zero inflation for anyone who wants to save money.

Gold is not too scarce. It can be more difficult to acquire than Bitcoin in some cases due to red-tape. Gold is not very fungible because it is difficult to separate. It's also difficult to verify that it is real gold. Even under gold monetary systems, a major source of inflation has been to dilute the amount of gold transacted by alloying it with small amounts of other metals. Over time the gold in the coinage has shrunk to fractions of its original amount. This can't be done with Bitcoin.

And the value of transmitting remotely, without censorship or interference should not be underestimated, particularly as governments and technology companies are increasingly pushing towards dystopias in order to attempt to save themselves from their own poor decision making.

Bitcoin also enables a kind of economy that was not previously possible, which is a micro-payment economy for online services. With some of the technology being built on bitcoin, you will soon be able to make instant payments worth fractions of a cent, with transaction fees being negligible. (This can already be done, just not yet at scale).

Since many people are invested both financially, and technologically in this space, it certainly isn't going to go away any time soon. If people happen to have their savings appreciate over that time by holding them in Bitcoin, it will only further cement Bitcoin's future as the next monetary standard.

Good luck sending gold through copper wires. Good luck transporting it without getting mugged. Good luck hiding it when the socialist state comes knocking for it.

I dont think precious metals will survive our lifetime.

Nuclear chemistry might be around the corner with either tech advancements or energy advancements. Only 1 needs to come true and it would kill the price of gold.

I'm still waiting for the hyperinflation Ron Paul and his adherents have been promising for....decades now.

If the best they can do is point to Zimbabwe or one or two other developing nations, then I think the concerns about governments printing money are either overblown or entirely off the mark.

Decades are not very long for debt. People usually hold bonds for decades.

The issue will come in when the cost to pay interest exceeds revenue. We would need debt to pay back debt, it will be THEN that we have hyper inflation.

If you have historical examples where this was avoided without printing money or invading a country, I'm interested.

In last half century, I would say yes. When you get close to 100y ago you get the always-mentioned Weimar, but I don't know about other cases. I would actually like to know more examples other than Weimar/Zimbabwe/Venezuela.

It’s true that well-run countries generally don’t run into hyperinflation, but it’s also true that well-run countries turn into poorly-run countries very quickly (e.g., https://drive.google.com/file/d/0B9_mR_M2zOc4Y2VhNzZkMDQtMDd... , feel free to ignore the first page; I’m only focusing on Gödel’s statements about countries turning into dictatorships).

The first relatively recent, nonobvious, example of hyperinflation that comes to my mind is Brazil during military dictatorship (which, yes, qualifies as a banana republic). According to Greenspan’s “Age of Turbulence,” Brazil paid for 90% of its budget with taxes and bonds like a well-run country, and printed money to cover the gap. Middle class and upper class workers got contracts with automatic inflation pay raises, but lower class workers did not. Those automatic pay raises created a feedback loop and hyperinflation ( http://www.sjsu.edu/faculty/watkins/brazilinfl.htm ). When prices got too crazy, they lopped off a few zeros and renamed the currency (e.g., cruzeiro, cruzado, novo cruzeiro).

The solution to the problem was much more straightforward than I would have expected: (1) stop printing money to cover the deficit, (2) convince people that inflation would go away, and (3) get IMF loans to straighten out the government budget ( https://en.wikipedia.org/wiki/Plano_Real , the loans were quickly paid off).

I was convinced we would have high inflation when the Fed increased the money supply during the financial crisis ( https://fred.stlouisfed.org/series/BASE ). The fact that we haven’t shows that the Fed correctly predicted that people would want more currency on hand because of economic uncertainty, and in fact did a good job predicting the size of the change. I’m impressed that they did such a good job, but I’m not convinced they always will.

I wouldn’t get rid of the Fed, and I don’t have any money in gold or any other inflation hedge. But I don’t expect our current low inflation to last forever (since the Fed has been targeting a higher inflation rate than we’ve seen, I don’t think the low inflation rate is proof that the Fed has complete control of things; it is arguably proof of the Fed’s limits to get what it wants).

Thanks for reminding me of that Brazil crisis, that was definitely too-much-money-printing. But as you point out, it did get handled. Which brings me to my main point why I don't believe the hyperinflation scare:

> I was convinced we would have high inflation when the Fed increased the money supply during the financial crisis

MANY people were. But the "mainstream economist" camp of Krugman, Summers, etc. was clearly proven right in this scenario. Adding to that the Euro crisis in 2012 (which disappeared the moment ECB commited for real to saving the euro) and I became sceptical to supply side economics ... And the doubt never disappeared - once you stop to implicitly believe in "sound money", "gov't intervention is bad" or "inflation is bad" their theories fall apart completely.

And central banks & their actions suddenly start to make so much sense. BTC & other crypto loses it. And I've seen no arguments to convince me otherwise.

So I _do_ believe our current low inflation to last for a really long time. If EU falls apart and there will be another war in mid.east and trade war between China & USA erupts we will get it higher, but that's the only way I can see it getting there. Because we keep appointing way too sensible economists to central banks :)

It's trying to solve the problem of having to involve a 3rd party in on-line transactions. Chargebacks are expensive to deal with. Jurisdictions are expensive to deal with. Standing up a multinational e-commerce site requires a lot of lawyers and accountants.

Will the risk presented by crypto always be greater than the risk of involving trusted third parties? Maybe. Maybe not.

Counterpoint: There's a lot of people who will stop buying stuff online with such a system, once they have been bitten by a system that has truly irrevocable payments. Part of the reason why I trust buying random $25 used video games from eBay (using Paypal) is that I know I'm about 99% certain to get my money back if it never arrives, or arrives in poor condition. I can buy a used Cisco 48-port 1000BaseT/PoE switch on eBay and know that I have some degree of buyer protection. Or I can go to Newegg and buy a new $700 monitor and trust that if something goes terribly wrong with the transaction, Visa's buyer protection/chargeback system can be engaged.

Moving to irrevocable online payments is basically the equivalent of handing a wad of cash to some stranger in a parking lot selling "new, sealed!" ipads out of the trunk of a car.

I totally agree with you in practical terms, but what you're really saying is that you prefer the governance offered by Paypal and the credit card networks to the governance provided by the government: IOW, it wouldn't even occur to you (or most sane people) to file a claim in court over a $25 Atari cart you tried to buy online. In the society these courts are designed to serve (peasant agricultural economies), the courts were where these issues were hashed out, and a fair bit of the "state-iness" of the state derived from its ability to solve these kinds of problems for people. Increasingly, this kind of justice is inaccessible to ordinary people except through "customer support" mechanisms at institutions like Amazon or Paypal or by tweeting at their CEOs.

One of the very real problems that cryptocurrency enthusiasts are concerned about (but IMO totally failing to actually solve) is that it seems like a really bad idea to leave such basic functions of state in the hands of difficult-or-impossible-to-regulate transnational enterprises. When will these players realize that they've got more "state-iness" than most actual states, and how will they use it?

> When will these players realize that they've got more "state-iness" than most actual states, and how will they use it?

In the brave new decentralized "free market" crypto world you are even more fucked if you have a problem. Who do you appeal to? Who decides if your edge case is worthy of rolling back the all mighty blockchain. The DAO folk got the "hack" stuff rolled back so the "thief" no longer had their money. But what about you and your Atari that never arrived? You think the top of the crypto pyramid is gonna roll back the blockchain for you? It can literally become mob rule!

And sure, you can say "build a better smart contract", but I would say that is impossible because then you have to encode every edge case you can imagine and all the ones you can't imagine. And worse, you still need that smart contract to interface with things outside the "trusted" sandbox the smart contract lives in (i.e. meatspace)--which means you need to trust not only whatever is providing that interface but everything beyond it.

Governments exist for a reason. One of those reasons is to be where the buck stops. A society that scales to billions of people needs somebody to say "this is right / this is wrong". It needs a final authority on conflict resolution.

Smart contracts are seriously one of the stupidest things to come out of the crypto space. It really highlights how some engineers think "I am good with computer stuff, so therefore I am also good at economics, government, politics, finance, monetary policy, contract law, etc". The whole idea is really arrogant.

> In the brave new decentralized "free market" crypto world you are even more fucked if you have a problem. Who do you appeal to?

Simple, if you need the extra safety you pay for the service of an intermediary, like PayPal or eBay or (in cryptoland) Purse.io.

If you don't need the extra safety, you don't.

Escrows can be even better with Bitcoin because of multi-signature transactions, the escrow can hold the payment without holding your money, so all they can do is approve the payment or not, they can't change the destination.

Rolling back the blockchain is like going to the government to reverse your $50 transaction, it doesn't make sense.

You won't need a claim either. Chargeback is easy. So in CryptoWorld, people should go to court and try get their money back from anonymous seller? That'd be a field day for scammers.

Right, this is why its totally unworkable as a solution to the problem of transnational corporations wielding too much power, and a totally crypto-ized global economy would probably just make that worse. It solves other problems fairly well (paying ransoms to anonymous cybercriminals, as an example), but also doesn't even try to solve the problem that ordinary people can't afford (or figure out how) to have small commercial disputes adjudicated by actual courts anymore, which is (IMO) the one of the reasons these corporations hold so much power.

In the neoliberal world order, government exists to ease the flow of international capital ("These regulations make it hard for us to scale our sales beyond the {US,China,Germany}. Please Mr. President, we need common-sense solutions!"). It has jettisoned its role of solving real problems for ordinary people ("Lord Fontleroy, Biff's dog killed two of my pigs.") as it once did.

Many people take extra safety for granted though. Wether it's chargeback or at least knowing who you pay to pursue further legal actions.

Let me rephrase consumer safety in crypto. Food safety regulations is kinda cool and we feel safe eating out. Now crypto food comes. It's cheaper, but seller now follows it's own understanding of food safety. Or not.

> I can buy a used Cisco 48-port 1000BaseT/PoE switch on eBay and know that I have some degree of buyer protection.

This is a basic insurance market. You can still buy the insurance separately if you want it -- sites like eBay would undoubtedly offer it with nothing more than a checkbox for about the same fee as the credit card companies currently charge for implicitly the same thing.

The problem with the existing system is that it requires you to buy that insurance, even when it isn't necessary. If you order something from Newegg, they're ultimately going to send it or give you a refund, because they're a stable business and it's cheaper for them to make good to begin with than have a small claims court order them to. So you lose 3% in processing fees for nothing -- Newegg is no more likely to not make good than the payment processor is to not reverse the transaction.

The existing system also basically makes micropayments impossible because the transaction costs are too high, but it's not actually all that serious of a problem if you get ripped off to the tune of $0.10 from time to time. The amount is small enough that it doesn't need to be insured, and that allows you to get a good feel for what kind of purchases are scams without actually losing any significant amount of money. It also creates an opportunity for curation services to vouch for verified sellers at a lower cost than insurance would have to be to cover the losses from less savvy individual buyers not knowing who to trust (or not caring when the insurance is mandatory).

> This is a basic insurance market. You can still buy the insurance separately if you want it -- sites like eBay would undoubtedly offer it with nothing more than a checkbox for about the same fee as the credit card companies currently charge for implicitly the same thing.

It's not the same thing. With chargebacks, in the case of fraud the payment processor almost always extracts the money from the seller, acting both as a deterrent and reducing the cost of the protection. If it was just insurance, it would be more expensive (because there would be less deterrent to (seller-side) fraud and it would cost more to recoup the costs).

> It's not the same thing. With chargebacks, in the case of fraud the payment processor almost always extracts the money from the seller, acting both as a deterrent and reducing the cost of the protection. If it was just insurance, it would be more expensive (because there would be less deterrent to (seller-side) fraud and it would cost more to recoup the costs).

It's still possible to do that by having the insurer escrow the payment in cases where you want the insurance, if that's actually more efficient.

But sometimes it isn't. Doing it that way subjects you to buyer fraud where the buyer actually receives the item, claims not to have and has their money refunded. The cost of that has to be paid by honest sellers, which then have to charge higher prices to honest buyers.

And an insurer who can't recover their costs from the seller has more incentive to vet the sellers (and buyers) so that they aren't insuring fraudulent transactions to begin with, which could plausibly have lower overhead than sellers eating the entire cost of buyer fraud.

Different choices may be more efficient for different transactions. A transaction between a reputable buyer and a reputable seller will have low insurance costs even without escrow. A seller with less reputation would have higher insurance costs, but can mitigate the cost by offering to accept escrowed payments but only from more reputable buyers. A buyer with less reputation could do the opposite, buying from a more reputable seller at low insurance cost by waiving the ability to easily reverse the transaction.

Forcing everyone into the same box only creates inefficiency.

Counter to your counterpoint: the people selling you those games on eBay also know that you might be able to revoke your payment either fraudulently or because of events outside the seller’s control, thus the selling price is almost certainly higher than it would otherwise be. In other words, both buyer and seller are incurring a cost due to the existence of chargebacks. Whether that cost is worth it depends on the actual probability of fraud or problems occurring, and at the very least, it seems reasonable to have an option for both buyer and seller to agree to not support chargebacks.

> In other words, both buyer and seller are incurring a cost due to the existence of chargebacks

The cost isn't due to chargebacks. It is due to the risk of fraud. Criminal behaviour like fraud extracts a toll on society at large and we all get to pay. The overhead added from chargebacks make both the buyer and seller internalize the potential risk of fraud. Without chargebacks, yeah prices might be slightly lower but society at large would get to foot the bill for fraud.

That's like saying "many people won't meet someone in the desert and sell drugs for cash after being burned by a shady deal." That is very true, but how is that relevant? Some people will still want to meet in the desert to sell drugs for cash, away from prying eyes and ears, despite the risk. The fact that many people still want all the conveniences of modern transactions doesn't change the fact that some people don't.

I'm not even really sure what all these posts are arguing for. Someone asked what problem cryptocurrency is supposed to solve, and the GP answered it with a good and succinct answer:

>It's trying to solve the problem of having to involve a 3rd party in on-line transactions.

It works the other way as well, there are some products businesses can't sell and communities they can't service because the risk of fraudulent chargebacks is so high.

Chargebacks from the business side. Rip-off protection from the consumer side. I personally will not be quick to give up the ability to dispute charges. That is a feature that just isn't possible in bitcoin without involving a third party.

There is no way of having charges "deducted from your account" with Bitcoin so there's no need for dispute or chargebacks.

The way cyrptocurrencies work, in order for there to be an interface that allows third parties from charging your account, you would need a smart-contract for counterfactual transactions instatiation.

Right now, I can't think of a "problem" that would require chargeback or dispute resolution and couldn't be solved this way.

You buy a good online from a seller, seller doesn't ship the item and refuses to pay back. What then? With credit cards you can go to the bank and demand chargeback or whatever.

If so, and if you believe the seller isn't trustworthy, I'd recommend the use of a smart-contract that only releases the coins if both parties sign a message.

But how would you protect the seller from the "evil buyer"? The one who receives the goods, but never releases the lock? Sure, he is not getting his money back, but the seller is not getting that money also.

The buyer has to pay to make the order, that's usually the case in most e-commerce transactions I can think of.

If the evil buyer convinces the naive seller to ship products without a payment being executed or a smart-contract based bond, then the situation is exactly the same with or without cryptocurrencies.... the seller must report the buyer to the police and either hire a collection agency or take some other action to recover the goods.

edit: on a second look, I think I misread your comment... are you asking about the mechanics of conterfactual transactions?

If so, the idea is that the contract is entered with the buyer signing a transaction with some form of conditional operation. One the seller ships the product, the shipping code could very well be the condition that allows releasing the funds.

There's plenty to talk about here around game theory and mechanism design, but if you are interested in the topic I can recommend some cool state-channel and plasma contracts we can go over and discuss.

You mean like another lock? But what is stopping the seller from holding buyer's money hostage and force him to release the lock just to get some money back even when he did not receive the goods?

An example of evil buyer would be something like:

1. The buyer buys goods from seller with smart-contract

2. The money in buyer's wallet gets locked.

3. The seller ships the goods.

4. The buyer receives the goods, but never signs the smart-contract.

That way the buyer gets what he paid for, but the seller never receives the money.

No matter how i think about it, smart-contract idea looks abusable.

1) the contract is initiated by the seller (sets amount, payable accounts, etc)

2) the contract is signed by the buyer, moving (or locking) an amount of money in the contract pending one of two situations:

2.1) the seller signs a message that the product has been shipped and the buyer signs a message the product has been received

2.2) the seller signs a message that the product has been shipped and after 30 days of no further message from the buyer's side the contract releases the funds

In this case, the solution is to have a commitment from the buyer that unless they take action (sign a special message to denounce the transaction / pull out of the contract) the seller gets paid. To address the scenario where the seller is malicious, the buyer can use the on-chain commitments from both parties as evidence of malpractice and report the situation.

You're adding pointless layers of complexity without acknowledging the core problem: there's no way for a smart contract to know the true state of the real world without having to trust someone to give it accurate information.

Also known as the oracle problem. Some platforms find solutions to this in a decentralized way, see Augur. The solutions to real world data being inputted into a blockchain is an economic one.

Not all transactions require the smart-contract to know about the off-chain world!

The "oracle problem" is what I think you are referring to but I have a strong view that the problem of low quality data can be solved with existing mechanisms and tools.

My favourite method to dealing with information quality is by providing incentives to good quality sources and having a method that allows a third-party (anyone with an account...) to submit a fraud proof.

The evil seller doesn't ship the item but signs the product shipped message anyway. Who's gonna stop them, it's not like the blockchain knows if they actually shipped it or not. Or maybe they shipped a fake or non working item. Then what?

Your caveat still renders the system vulnerable to malicious buyers. What if the buyer receives the product but "takes action" by denouncing the transaction or exiting the contract?

On-chain, the solution is to have an oracle provide a third vote somehow. Off-chain, the solution is for the seller to report the buyer and its address to the authorities.

I can make a contract that relies on one single third party and in that case you are correct that there is some existing trust relationship. However, the protocols are designed such that the trust you need to have on the service provider is minimised with trusted computing systems and the contract's mechanism design.

Conversely, I can also write a contract that trusts a pool of oracles, or a prediction market (here the trust would be in the prediction market protocol and not on its operator), or a token curated registry where individuals are paid to give accurate information.

Banks are not really necessary.

Even by basic game theory, scamming your customers has long term negative value.

Reputation is worth much more than money.

No you just change your name and try again. And do you want to tell some one who has lost 100k+ to bank fraud when buying a house - a common and increasing type of fraud in the UK

Basic solution would be for seller with low reputation to lower the price. Even if not a lot of buyers take the risk, lower price should eventually attract enough people to allow a legitimate seller to build the reputation.

People already don't trust too low prices, because that's a sign of a scammer. And margins are already rather low. Would you take a gamble save €10 or loose €1000? Even with all the customers' protection in place, I already rather pay 1-2% more if that means buying for a more reputable seller. Without the protection, they'd have to be in scammers' price range to be considered...

In many cases the entrenched players in the market already have good prices. Upstarts who can't use economy-of-scale try to make their way by providing superb customer service or providing a better service in another way. But it's hard to give it a try when you don't have the protection of chargeback.

Well, it's hard to compete in the already established markets.

But you have to, one way or another, usually by providing better value.

Be it lower price, faster delivery or higher quality products.

Otherwise, if there is no initiative for people to use your services, are you really necessary?

I'd argue that competition is mandatory in market economy. Having an easy way to get a basic level of customer trust lowers the entry barrier. Which is good to prevent monopolies and ensure market is functioning properly.

One of the most important values one can provide is trust. A known bad option is many times better than the unknown nothing. An upstart would have to provide much much more value to make up for that.

Yes and there is a converse problem, the seller ships the item but the customer having received the item fraudulently requests chargeback - this is common, sadly.

I lose the item, the money and a fee - bitcoin, like cash solves the fraudulent chargeback problem - but the buyer is unprotected.

Trusted Escrow solves both problems.

The chargeback system isn't good for small retailers. The banks have no incentive to check the system or secure the card as the onus is on the merchant.

The chargeback system is the only reason I’m willing to patronize small retailers at all in many circumstances. If it were really a net negative for them, they wouldn’t accept cards at all.

> That is a feature that just isn't possible in bitcoin without involving a third party.

It's also not possible in fiat currency without a third-party. But Bitcoin not only gives you the option but also provides better solutions on how to involve the third-party. A Bitcoin escrow doesn't need to control your funds, only the permission to approve or deny a transaction, using multi-signature.

1) When a budget airline went bankrupt, leaving me stranded in a country most people can't place on the map (i.e. limited flights out of it.) The full ticket price was refunded.

2) When a music festival I had a ticket for went bankrupt. Full ticket price refunded.

3) When a concert was cancelled, and I'd bought the ticket on a dodgy reselling website which refused to refund (ViaGoGo), saying they'd not been informed of the cancellation. It was widely reported in the music press, and there was an apology on the band's homepage. The bank refunded the money.

Chargebacks are like seatbelts: ideally only a tiny percentage of users ever need to actually use them, but their presence increases the safety of the system for all users.

Right, you need a remedy for the inherent insecurity of credit cards. Is it always a charge back though? In other words, are merchants eating all the costs of fraudulent credit card transactions? I guess either way the cost really gets passed on to us consumers in the end.

> you need a remedy for the inherent insecurity of credit cards

Fraud and theft are fairly general problems. I would direct your attention to /r/sorryforyourloss

> In other words, are merchants eating all the costs of fraudulent credit card transactions?

If the goods cannot be recovered, then yes, the merchant eats the costs.

> I guess either way the cost really gets passed on to us consumers in the end.

Someone will always be left holding the short end of the stick when fraud occurs. The alternative to shifting the liability to the merchant is the consumer being directly accountable (rather than vicariously as you're suggesting).

Remember that you don't need to use it often precisely because every party knows that you have that option. So people don't try to scam you because they know it won't work. They know it is a solved problem, a means of security they can't breach. They know that if they misbehave, the other party won't be harmed (they'll get their money back, if harming them was their intention) and they themselves will be punished instead.

Escrow is far more expensive than chargebacks. And if we're involving a third party either way, I'd rather have the regulated, battle-tested, already existing banking system.

Chargebacks essentially are escrow. The merchant can't stop them from happening because the money is taken from the merchant account reserve, i.e. a minimum balance that the merchant can't withdraw. Sounds similar to money held by an escrow agent doesn't it?

And credit card transactions are also expensive, between 1.5% and 3% and even higher[1]. It's just that the cost is hidden from the consumer by accounting for it in a higher product price. (Some merchants like gas stations may offer a cash discount, which can be used as a rough estimate of that hidden cost.)

On top of this, merchants get charged a hefty fee (on the order of $50) for each chargeback that they receive.

Only applies to consumer cards and only the interchange (ie. the part that the bank of your card gets). MasterCard and Visa fees are still quite substantial.

A regular merchant would now pay < 1%, so quite a bit cheaper than before.

That system that you use, while international, is only available to a small fraction of internet users. Entire countries, and billions of potential customers, are cut off from transacting with you under that model.

Smart contracts are a bet on our ability to write code that is free from flaws. History suggests that the odds of that are not good. I'd rather trust a bank and the legal system.

> History suggests that the odds of that are not good. I'd rather trust a bank and the legal system

Which is the silly part about "smart contracts" in the first place. Any smart contract dispute will just "devolve" back into the meatspace legal system. Anything that isn't a dispute because it is just "routine execution" (eg: moving money from account A to account B automatically) can simply be called "business automation" that consist of a bunch of "business rules"--basic terminology that has existed since the dawn of computers.

Smart contracts do nothing but add overhead to any transaction.

The code that runs on your bank and "legal system" was written by people who make mistakes as well.

Writing smart-contracts isn't easy (and I author and audit them for a living...) but it's doable.

Your trust on a new technology grows as you get used to it. Anecdotally, I remember how hard it was to get OS virtualisation accepted in corporate environments just a decade ago and my last enterprise customers where already using all form of virtualisation (net, storage, os, etc)..

There are nuances to the type of third parties we are talking about here.

The type I'm discussing, something like the Lightning Channel and Plasma operators, these are roles that have cryptoeconomic properties that don't allow them to take over your wallet or refuse your service.

edit:

The base premise of having a smart-contract being itself the escrow is perfectly achievable. This doesn't mean that such a setup is the best solution to every use case and I believe that we'll see plenty of developments in this area in the coming years.

For now the best approaches use game theory and computer science to reduce the amount of "trust" the parties must have in each other and the system itself but they are very much under active research & development.

That's not correct. You can have a third party that is trustless, ie that cannot perform any action on its own that would favour or harm you.

Take for instance the role of Plasma operator or Lightning Channel operator; The role allows for a third party to have the costs of setting up infrastructure for you to use, but at no point are your funds held by the operator and you are always able to exit a contract if you submit on-chain evidence of fraud.

That's not the case in many (most?) of the cases I mentioned.

In plasma for instance, the operator and seller could collude against the buyer but any "illegal" operation they do on-chain is enough for anyone to trigger a mass-exit and cause financial and reputational loss to the operator.

A common theme in all the on-chain payment technologies I mentioned is that they do not put any one party in "charge" but the volunteers who run staking channels of any sort (plasma, lightning, etc) can and will suffer financial damages (loss of deposit, etc) if proven to act maliciously.

The problem there is, nobody likes using escrow for everyday things.

Example: Renting a car. The rental companies want a way to recoup costs from any damage you do by, e.g., smoking in the car. They give you two options for how this can work: You can either pay with a credit card, which has a way for htem to do that built-in. Or, if you don't want to pay with a credit card, you can give them a bunch of extra money to hold in escrow.

Guess which option people basically never choose, when both options are available to them.

I would assume that merchants feel similarly about chargebacks vs escrow, and for similar reasons.

Chargebacks are also insanely useful. If my card is stolen I can get my money back, if my merchant tries to defraud me I have a recourse. I will never use bitcoin for consumer transactions for this exact reason.

On the other hand they are mostly related to the limitation of cards: you give the merchant a number with which he can draw an arbitrary amount, any time, and pass it on (or leak) to someone else. An authorization token for a single transaction to a specific party for a specific amount could probably work without chargebacks.

> An authorization token for a single transaction to a specific party for a specific amount could probably work without chargebacks.

1) This is precisely what you get from EMV transactions. A cryptogram covering these details, signed by your hardware token (card). Online transactions don't do this, it's true, but that's why we have the verified-by-visa type stuff. It's imperfect, I agree.

2) Chargebacks are still necessary, because it's not just about merchant overcharging or unauthorised transactions, it's about what happens when someone fails to ship, or sends you broken goods etc

1 was true, but is increasingly less true. You can purchase things on the web using Apple Pay, at least on some sites, which also produces one time use tokens.

A significant number of sites also use stripe, which produces merchant specific revocable tokens. This doesn’t eliminate merchant fraud risk, but it does vastly reduce the risk of your CC details being leaked.

on 2), the token must be for a specific amount, a merchant shouldn't be allowed to double dip or charge more unless he specifically asks authorization to do so.

On the merchant not delivering, I think this is really wrong. If you have a conflict with a merchant, I appreciate that reversing the payment is a convenient way to apply pressure but I think is not the fair way to do it. It should be legal process really (if it ever gets that far).

With EMV transactions this is the case. I'd like to see the system of home card-readers spread, though it would add friction to online purchases.

> On the merchant not delivering, I think this is really wrong.

It's not only a perfectly fair way of doing it (if the merchant wishes to dispute it they can go to the courts), it's often the only way to do it, as merchants often disappear or make themselves uncontactable, or may feel no need to comply with legal process in the purchaser's country of origin.

We have thousands of years of history of merchants ripping off consumers - "Caveat Emptor" for example. This is a measure to prevent the worst of it, and it creates a much safer market. Without it many people would just not transact with new entrants to the market, if at all.

Your card being stolen has nothing to do with chargebacks.

Your mobile could be stolen with your cryptowallet inside and you could do a remote wipe of the device. You can also use multi-signature protections for large transactions, etc.

Likewise, if you hold some bank notes in your wallet next to your credit card, an attack will deprive you or your money. The bank might cover any charges made on the card pending some admin and police work. For that service you pay a fee to the bank.

I carry two digits worth of cash in my wallet. Losing that would be more of a frustration than an actual financial setback. Honestly I'd be more pissed about losing various IDs than the actual money.

Losing all the cash deposits I have would be so much worse, which is why I do business with a FDIC insured bank that will protect me against some contingencies, including account takeovers. Bitcoin offers me significantly less protection than my current setup, and would require far more mental effort to maintain my security.

"So long as the cryptocurrency hasn't gone already. If it has.. well whoops, bye bye money."

This was the comment I replied to. It says money and I'm talking about money.

Bank cards represent account holdership, not money. Losing a card entitles you to get a new one for a small charge. Your bank held funds are protected by law, and you can expect somewhere between 75% and 100% of your assets being covered from fraud.

In response to your stuff about chargebacks and lost phones. Let me retread the steps -

You said - "Your card being stolen has nothing to do with chargebacks.

Your mobile could be stolen with your cryptowallet inside and you could do a remote wipe of the device."

You do this in order to try to establish cryptocurrency as being as secure in that situation as a credit card, i.e. theft resilient. I pointed out that if the cryptocurrency was already used, unlike with a credit card, you're unlikely ever to be able to recover the money. Then you started handwaving about cash. This appears to me to be a disingenuous move of the goalposts.

I'm comfortable with what I wrote though. Bank cards don't represent money and the management framework that allows for chargebacks is unrelated to the card itself, it's law.

I've clarified what I think is a consistent view, and no goalposts are being moved when I point out that cryptocurrencies == money but bank cards != money.

That's all good and well, but you've lost sight of the consumer's motivations. Consumers want to know that they will be made whole if something really bad happens. They're not really interested in the fine distinctions between possession of the currency and possession of the account that contains the currency. They want their money back if someone hacks their account, if their card is stolen, if the bank goes under, or if the merchant doesn't ship the right product as promised.

If bitcoin does not offer these features, I cannot imagine it ever taking off as a currency (as compared to a speculative instrument, which is what it is now).

The thing is, Bitcoin or Ethereum are technologies and the protections and guarantees the "masses" will look for are not provided at protocol level, this is where entrepreneurs step up and offer services based off these technologies.

Well for starters it would have protocol level access to the biggest digital market currently in existence. The tokens launched by blockchain native companies will form a token-economy of their own.

Also importantly, there are functions a bank can provide that you don't need however there's no way of you avoiding paying for it somehow. A crypto based bank could very well be a legal custodian for key material, an identity provider and a lender... it could also be a mashup of several services/protocols that do each of those functions.

The financial aspect is frankly insane. Banks have no problem transferring money today, none. Adding in a wildly unstable asset to “improve” a working system is a classic case of technologists thinking of tech first, real world second.

Backing banks in a different currency than you actually purchase goods in is like declaring that all transfers must be accomplished in Yen. Why should I expose my rent payment to an exchange rate?

One might argue that we’d just use bitcoin as our currency, but that’s just begging the question. Why should consumers want to switch away from their regular currency?

There’s also no compelling reason why identity providing should:

1. Be done by your bank.

2. Use the same technology as your currency.

Long story short: listing a bunch of things you can technically accomplish with bitcoin is emphatically not the same as providing reasons why bitcoin should take over. It’s a bit like hand stand walking; it’s an impressive trick, but just because you can do it doesn’t mean it should become your regular mode of locomotion.

Banks don't have problems transferring money today... are you sure about that? Because I've worked in fintech for 20 years now and I'm convinced that is not the case.

The role of banks as identity providers exists today, you need a bank account to access certain services. Banks actually make for great KYC providers. I don't understand how you don't know this but still want to have a discussion on this topic...

My bank verifies my government issued ID. The government is the provider of ID, the bank just verifies that. Some other services might leverage the banks for this too, but in no way does this mean that the bank is providing the ID.

I also have never seen anyone else verify my ID with my bank. I have seen them verify income, but that’s not surprising since that’s where I store my money. When someone demands to know who I am, they usually require my drivers license, passport, or SSN, none of which are bank issued.

And again, consumers send money all the time, using banks and other regular financial institutions. If they couldn’t send money, the economy would have ground to a halt.

So again: why should I want to switch to bitcoin, or have my bank built on bitcoin? It’s perfectly reasonable to say that banks are going to make protocol changes under the hood to make things smoother, that happens all the time. But to say we’re going to use a whole new currency needs justification to the end users who will notice the change.

Those aren't free, they drive up prices by a few percent and frankly fraud only matters for large transactions and/or untrusted merchants. Bitcoin is cash, not credit, and avoiding 2-3% of fees tacked on by credit card companies is more than enough reason to want internet cash for purchases where you're not concerned with fraud.

The baseline price for payment processing is well below 2-3%. In the EU, credit card processing fees are capped at 0.3%, and these companies are still able to make a decent profit despite.

What those high fees really come from is the need to cover the cost of all those rewards programs that are so ubiquitous in some countries such as the USA. Those would probably disappear pretty quickly in the presence of a law allowing merchants to add any processing fees (perhaps above some nominal baseline cost) on to the bill. 1% cash back doesn't seem like nearly so great a deal when you have to reckon with the fact that what's really going on is that you pay 2% more, and then the issuing bank gives half of it back to you, along with a generous dose of smoke up the ass, and then pockets the other half.

Actually most states do permit credit card surcharges by the merchant. California, Colorado, Connecticut, Florida, Kansas, Maine, Massachusetts, New York, Oklahoma and Texas are the ones that ban it. Some of those states have pending litigation against those laws. Some of them also allow discounts for paying cash (as if it's any different than a surcharge for processing)

There was a time from 2013 to 2017 that merchants were permitted by processing agreement to do it, but Visa and Mastercard convinced an appeals court to throw it out. A few places in my state still do surcharges, but it's pretty rare.

In practice, I don’t know of anyone offering 0.3% card processing fees. Most POS systems and online payment processors are more like ~2% e.g. Stripe is 1.4% + ~€0.30 to take online payments from within the EU. And chargebacks are passed on to the merchant with an additional fee tacked on.

Can you point me to any cheaper solutions?

I like the idea of having the processing fees displayed prominently on the receipt though (like VAT). If people had to actually pay more to use Amex (rather than the merchant absorbing the blow, or distributing the costs across their other customers), then they might quickly go out of business (and rightly so).

>In practice, I don’t know of anyone offering 0.3% card processing fees

Obviously. They need to pay 0.2%-0.3% to the issuer (ie. the bank that gives you your card), but VISA/MasterCard and the processor want their cut as well.

> Can you point me to any cheaper solutions?

At least in Germany there are quite some cheap POS solutions:

The actual problem here is that rewards programs and universally applied CC fees represent a transfer of wealth from those who use cash to those who use credit.

No, it is the way GP described it. Both transaction fees and reward programs are governed by the same entity: payment processing company. Reward programs were a trick to make people accept high transaction fees, because people fall for the illusion of "getting something in return". In practice, transaction fee is paid by everyone, but many people do not bother to claim their rewards, so it is a net win for payment processors. Also, even people who do claim their rewards usually do not do excesive calculaitons and do not realize that for 3% payment fee they get 0.5-1.5% worth of reward.

Last time I worked at a place that could swipe credit cards, we would get charged one fee for regular cards, and another, much higher fee if it was a rewards card.

(This was back when non-rewards cards were the regular variety, so I'm assuming things have changed since then.)

I know they’re not free, and I’m happy to pay for the service. I can name a large number of smallish purchases I would not have done online if I didn’t know that Visa would make it right should the unknown vendor stiff me.

Bitcoin is piss poor cash, given the wild exchange rate swings and the ability for it to be stolen online. It literally has no property that I desire.

Agree, but I'm not promoting Bitcoin, I think it's poorly designed by someone who doesn't understand the properties of good money. Another crytpo with better properties will supersede it. It's the idea of crypto that's great, not the particular implementation of that idea called Bitcoin.

Once you know an trust a vendor, paying with cash will eventually be a few percent cheaper just as it often is as brick and mortar places sometimes when they offer cash discounts because they too don't like the fees the cards companies force on them.

It's not an either or scenario, it's a both scenario; you should have the option of cash or credit online, just like you do in the real world.

> The counter to your argument is that widespread use of existing payment methods means the market prefers them.

That's not a valid argument. The market always prefers what "is" until a critical mass understands benefits of a new technology. The existing credit system was not designed for today's world, is pull based, and is rife with fraud on both the merchant and the consumer side. Merchants absolutely despise credit cards, we can't wait for something better to be invented.