I really like cash for a few things. For instance local buying and selling. It's so much more convenient to just hand someone a $20 and walk away with the item than to spend the 5 mins dallying on venmo trying to look up their handle, with terrible cell service, and hope you don't misclick on a total stranger who won't return your money if its missent. When I'm selling I prefer cash in hand too. I don't want to find myself in some elaborate scam using these electronic transfer apps.

Cash also helps with tipping. If I hand a waiter cash, I know it goes to them. If I write a tip as a line item on the check, who knows how management is skimming that pool.

Then there is the security aspect. Credit card info can be leaked or scammed many ways. Meanwhile, with a cash payment our relationship is severed the minute I leave the establishment. There is no opportunity for you to collect my info, or for a hacker to steal my info through you, or to take any more money from me than the finite amount I already gave you.

Plus there is the human aspect too. Many people beg for cash, but also many small business owners cannot afford to work over the table. I'm talking things like food vendors in trucks or simply on tables on the sidewalk. I love me some al pastor, and I know that should these businesses have to go from grey market to white market they wouldn't nearly be so viable. Cash makes these sorts of businesses possible and provides a lot of opportunities for plenty of people that for many reasons, do not currently use electronic means.

> spend the 5 mins dallying on venmo trying to look up their handle, with terrible cell service, and hope you don't misclick on a total stranger who won't return your money if its missent.

I think all your other points are valid but this one is odd to me; it just seems like bad Venmo UI. I've never used Venmo and I live in East Asia where most systems use QR codes to identify the vendor. The chances of sending money to the wrong account is slim to nil and it takes less than a minute. I'm currently sat in a cafe where I can see 5 QR codes lined up on the counter for different apps.

Venmo also has QR codes. I have never entered someone's handle manually when in the situation described above. The person opens up their code, you scan it. Takes like 5 seconds.

Venmo also allows using QR codes quite easily (tap "Scan" on the home screen and then scan a code or tap "Venmo me" to show your code), but for some reason many users don't seem to know that and end up trying to look people up by their username instead. I think it's because QR codes really never caught on in the US.

QR codes are clumsy and inconvenient, moving to NFC was the right move for the states and most of the developed world. However, Starbucks uses QR codes for its app if you pay in store (but you can mobile order and not pay in store at all, so I rarely bother).

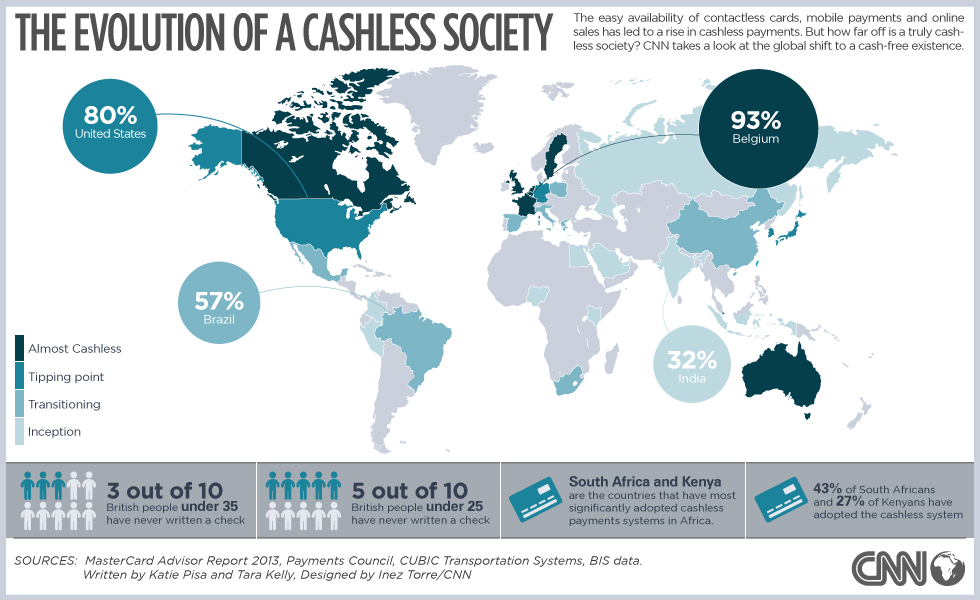

China built its cashless system using QR codes, since it doesn't require any additional hardware beyond a smartphone and the clumsiness is just another thing you get used to over there.

I could be misremembering since I lived in China a long time ago, but I feel like QR codes were wildly popular in Asia long before digital payments became really popular. So it probably made sense on several fronts to adopt them for payments as well (everyone already used them anyway, they're effectively free, etc.) rather than build a new system.

I didn't think they were especially popular until they were used for mobile payments. I'm not really sure about other countries in east Asia, they tend to grow completely different ecosystems from China.

Yes, that’s why the Chinese chose the technology. Whereas America was already used to POS’s everywhere, and square makes relatively affordable receiver NFC POS hardware for phones.

Venmo UI used to be a lot more serviceable, but they recently updated the app to add crypto speculation to it, and I have no idea where things are in the redesigned layout. Even then, the requirements are that I need cell service at least, and data service even where I live in a county of 10 million people can be quite spotty. Not to mention I still don't have an unlimited plan and am sometimes throttled before my billing cycle resets.

Granted we’re on a startup forum and most of us develop services:

> It's so much more convenient to just hand someone a $20 and walk away with the item than to spend the 5 mins dallying on venmo trying to look up their handle

Wouldn’t this be solved at the matching level ? You probably found that person online, checked the photos and description and decided to make the transaction. If there is a “complete the purchase“ button you just click, there would be no thumbling in Venmo. And this is exactly my experience with local marketplace sites.

> If I hand a waiter cash, I know it goes to them.

It might be different where you live, but they can be requested by contract to add it to a pool. The same way when you pay your meal you hand the waiter cash but it doesn’t go to them.

> Credit card info can be leaked or scammed many ways. Meanwhile, with a cash payment our relationship is severed the minute I leave the establishment.

Wait, have you ever been scammed by paying by card in an offline setting ? Or have the transaction replayed or reused ? How would it work ?

> I know that should these businesses have to go from grey market to white market they wouldn't nearly be so viable.

This is I think the most prevalent point. Going forward I’d only see prepaid offline system to cover this, and we’re not there yet on the user to user money exchange side (it currently only works in a centralized setting as far as I know)

Another issue with Venmo is the possibility of shady buyers using stolen credit cards. So a week later, the transaction is reversed and you're out $300 and the item you just sold. As a seller, I'd rather just take cash. The new IRS $600 reporting limit for 2022 is also a joke.

The focus on Venmo is because you are in the US I guess ?

The credit card reversal part is solved by 3D Secure 2.0, where the barrier to get a transaction reversed is way higher (the issuing bank has the responsibility to validate it comes from the customer). I don't know how fast it's adopted outside of the EU, but we're far from the days where you just passed operations with a stolen number and a valid CVC.

You cannot just throw technology at a human problem and expect it to be solved. Scams will always exist as long as there is someone to be scammed. No amount of technology can "solve" this problem.

We're talking here about a case that was introduced by technology (wide possibility to emit chargebacks) and is fixed by technology (severely limit chargeback potential).

> Wouldn’t this be solved at the matching level ? You probably found that person online

Believe it or not, lots of transaction happen without finding someone online - maybe most, for most of the world. I think most of my transactions are offline.

> they [waitstaff] can be requested by contract to add it [the tip] to a pool

I don't think restaurants follow laws that closely.

The discussion is on digital vs cash transactions. If we're setting the stage in Ethiopia for instance, I think there isn't much to argue, realistically you won't be buying your coffee with prepaid digital wallets either way.

IMO I prefer seeing things in hand before buying them usually. I have gone to see things that looked great online and walked away from the sale when I saw the flaws in person, so unless I am truly desperate I wouldn't want to buy something before I can see it especially when its used. I've never heard of the tipping contract thing in the U.S., but even still if I give them straight cash that gives the waiter an opportunity to put some in their pocket and the rest into that pool. I've never been scammed personally, but there was a time when credit card skimmers were bad at my college campus/city back when I went. I at least wiggle card readers as hard as I can now at gas stations and ATMs. Plus these days with all your card info being printed on one side of the credit card, it would only take one person behind you in line to snap a quick photo and they have all the info they need suddenly to make purchases.

>> Credit card info can be leaked or scammed many ways. Meanwhile, with a cash payment our relationship is severed the minute I leave the establishment.

> Wait, have you ever been scammed by paying by card in an offline setting ? Or have the transaction replayed or reused ? How would it work ?

I know a couple people who've been hit by credit card skimmers. It is harder with chip-and-pin but people doing frauds are pretty clever.

{kind=link}

{kind=link}

Cash also helps with tipping. If I hand a waiter cash, I know it goes to them. If I write a tip as a line item on the check, who knows how management is skimming that pool.

Then there is the security aspect. Credit card info can be leaked or scammed many ways. Meanwhile, with a cash payment our relationship is severed the minute I leave the establishment. There is no opportunity for you to collect my info, or for a hacker to steal my info through you, or to take any more money from me than the finite amount I already gave you.

Plus there is the human aspect too. Many people beg for cash, but also many small business owners cannot afford to work over the table. I'm talking things like food vendors in trucks or simply on tables on the sidewalk. I love me some al pastor, and I know that should these businesses have to go from grey market to white market they wouldn't nearly be so viable. Cash makes these sorts of businesses possible and provides a lot of opportunities for plenty of people that for many reasons, do not currently use electronic means.