As someone that is the food mostly spice trade prices have started going up in the last 2-3 weeks though prices have not even reached pre pandemic levels. Black Pepper prices have jumped 20+% in the last 20day that price is still 50% cheaper than what it was 4-5 years ago. The largest problem is not availablity of goods rather shipping. I would advise investing in shipping companies if you are active in the stock market. As now days they are charging 3-4 times the freight and still hard to get space so they probably rare raking it in

Be careful with your reliance on BDI. As the name implies, it does not reflect prices for the entire shipping industry (e.g. container ships). I used to have investments in the area as an institutional investor, and it was common to see people not understand this.

Which was all caused by an extremely large drop in the dollar. Anytime there is such a drop, you get global food chaos from a big spike in the price of commodities that destabilizes markets until they're able to adjust. And then you get civil wars out of that inevitably, it helped to cause the Arab Spring as one example.

The US Dollar Index was at 120 in early 2002, and then proceeded to fall persistently until the middle of 2008 when it rested at around 71. An epic collapse by the dollar that triggered all sorts of nasty global effects. Fortunately this time around the dollar drop hasn't been so bad, most major currencies are debasing at the same time. The dollar is merely back to where it was in 2015 and 2018, so far.

I'm just beginning to learn about investing...Is there any book and/or website to learn about how the dollar can affect commodities that you would recommend?

I don't think you need a book. When commodities are priced primarily in USD then a decrease in the value of USD leads to an increase in the number of dollars required to make the same purchase.

Increase in any price can be seen as an increase in item value or a decrease in USD value. It takes a more in depth analysis of the market to determine which is the cause of price increase.

Common stock advice: if you hear about an investment opportunity, you've probably already missed out.

Ex: Bitcoin stocks (yes they're stocks / investment products) are only really reported on when they're at an all-time high. They may go up a little more if you're reading something fresh off the press, but it's not going to go up as much as it already has. I mean if you bought a year ago you could have had a 10x return on investment, if you invest now it'll be 10-20% return on investment at best.

If “hear about” means major media wrote a news story about it because it has gone up then yes. But I’ve learned about profitable investments from places like twitter, reddit etc if you are deeply plugged in to what is happening.

Historically when they reach all time high again after a crash they still go up quite a bit (like 400% last upswing). Obviously not a huge sample size there though

Bitcoin has different fundamentals IMO. For buy and hold I still think 10x from here (over the long term) is possible. This year we might see up to 100k. It’s extremely fickle. We could easily see 5k again. No one really knows, though. The best fundamental analysis that gives a bright future is of Bitcoin replacing some significant market cap for gold. Probably not though.

Yup, stock market is all about factored in valuations and others saw the writing on the wall. Since rises and drops are due to surprises, the only way it’ll rocket further is if things will go even EVEN better than already expected. I sometimes have to repeat all this for myself... it helps :p

CPI is a joke, they do something called hedonic adjustments to things like tech products etc. It's completely subjective and BS. Technology is deflationary, things should get cheaper because we go after producing them in creative ways one demand is high.

CPI is absurd, it only perpetuates consumerism and punishes savers.

We product 2x the food society consumes - mostly wasted away, just with some supply chain efficiency - there's a lot more room for food not to be expensive though.

> CPI is absurd, it only perpetuates consumerism and punishes savers.

Okay okay back up.

The consumer price index is a series of numbers designed to help people understand what dollar-denominated figures mean to ordinary people going about their lives, spending those dollars. If that's "consumerism," well yes, it's a portrait of consumerism.

Many economists, mind you, believe CPI doesn't correct quite enough, and suspect that it overstates the inflation it hopes to measure by around 1%. This is because it tracks the actual prices of a certain "market basket" of goods with specific products in it, and that basket gets out of date, as people substitute products.

But if someone's "punishing savers" and "perpetuating consumerism", it's not the index, and it's not the people compiling the index, and it's not the people trying to make the index more accurate by adjusting for quality. Assign the blame where it's due. You have a beef with the Federal Reserve, and possibly with other agencies or laws which refer to the CPI to make policy.

There's a ridiculous amount of misconception, FUD, and ignorance around inflation / CPI (it doesn't include housing, it overweights entertainent, it exclude food and energy, hedonic adjustments/basket substitutions make everything look artificially cheap)

To professional economists, it can be infuriating to read (I imagine similar as medical professionals reading antivax blogs/comments, or radio engineers reading about dangers of 5G radiation).

I had a good intention once, to write layman exposition to clear most of the misconceptions. But much like the calculation of the CPI itself, it's a lot of work and ultimately not very rewarding. An unfortunate fact is that a very large part of the CPI comes from household survey responses. These are too expensive for non-professionals to reproduce and verify independently, so probably no amount of writing can really convince CPI-doubters.

Is there an index that isn't a 'consumer price index' but a 'cost of living index' instead then? An index that includes the basics of life like food, energy costs, shelter, transport, education, healthcare and some basic consumer goods? I think the issue most have with CPI is it's often sold as a cost of living index by media, politicians and policy makers and it makes people feel unheard as a result.

"My cost of living has doubled but your saying everything is fine since the CPI has only gone up %3!!!" and general 'let them eat cake' style behaviors saying that iPads are 'so much cheaper'[0] is the general feeling I get.

I’ve always wanted to see this + I would love to see two Versions of this, one for a 25th percentile earner, and another for 75th percentile. E.g a) what it costs to rent a modest apartment, drive a Honda Civic, shop at Walmart, have 2.5 kids in public school etc. and B) own a home in a metro area, drive an entry level luxury car, shop at Whole Foods, send kids to private college etc.

It’s my perception that there is not much inflation in some areas of the market (chicken thighs at Kroger) and tons for the “keeping up with the Jones’s” set (organic produce, private school education etc)

My point being that inflation can be quite different based on different baskets of goods / consumption patterns

People constantly cite that CPI excludes things like housing costs, or if we probably dug into it more excludes stuff in strange ways. It's also probably a global thing, some countries do exclude it completely, others do not so it can confuse things:

The CPI does include housing. And my citation for that is the Bureau of Labor Statistics, whose job is to put it together. Here is the document with excruciating detail:

Housing is 42.385%, of which the shelter itself is 33.316%. The rest includes things like "Clocks, lamps, and decorator items" at 0.313%.

That's American data. Maybe the Australian data (your first link) really does exclude it, but the US most certainly does not.

If people think that the basket of goods is skewed, they need to justify that by comparing it against this list. The BLS makes a ton of data available, and it's unreasonable to claim otherwise.

> general 'let them eat cake' style behaviors saying that iPads are 'so much cheaper'

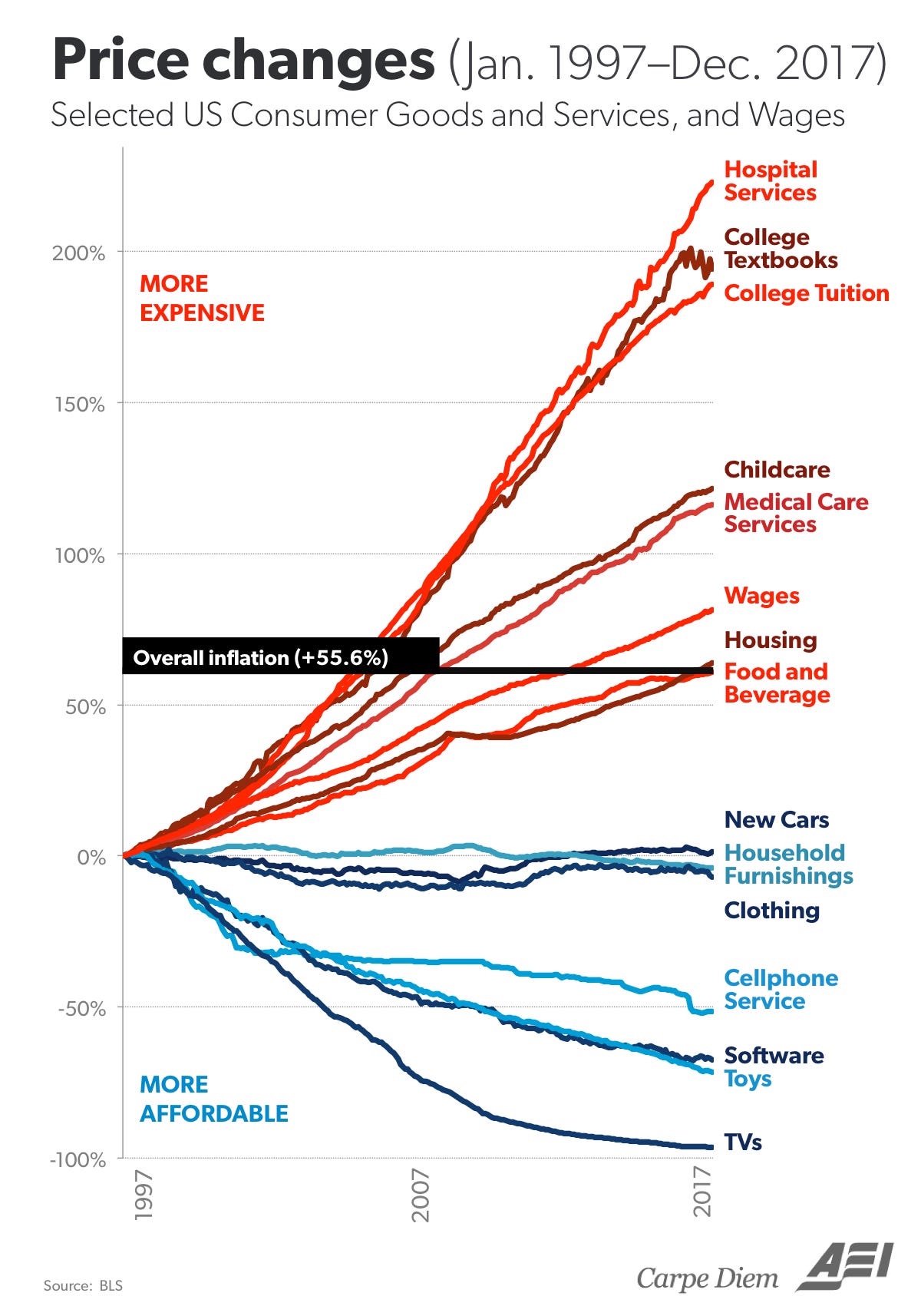

This is a good visualisation of which things got cheaper and others got more expensive, over the last 20 years in the USA. It shows how a "consumer price index" in which, for example, the price of tobacco is weighted at >50% the price of education, can make it seem like it's all okay.

1. The current BLS weights for Education is 3.033%, for Tobacco and smoking products 0.608%, that's 20%, not >50% [1].

2. There are around 20mln Americans in college, versus around 34mln adult smokers. Be careful about peer-group bias: how many of your friends smoke, how many went to college?

It seems like for TVs, it's more that you get a better TV for your money, not that people are spending less on them? A cursory Google search suggests $500-$1,000 was the norm in the 90s, and that seems to be about what people are spending these days too. I can find a nice 24 inch one for $100, but I expect you could find cheaper TVs in the 90s too.

That is a wonderful and very telling graph. Also interesting to note that everything that has becomes cheaper is optional spend (except clothing) that one can do without. Everything above the line which has become more expensive are things which are more necessary.

Maybe the Libertarian in me is coming out when I look at that chart, but it sure seems that the sectors of the economy that increased in price the most are also the most regulated and subsidized.

Without delving into the data, wouldn’t a plausible explanation be that we regulate and/or subsidize those industries _because_ they are the most inflationary? Industries with downward price trends don’t often need consumer protections.

The counter argument is prices come down with increased supply and competition-driven innovation. Regulation inhibits supply. How would regulation make them less inflationary?

My layman understanding of inflation is that it is the measure of change of purchasing power a unit of currency has over time. I think most laymen, including myself, questions how this rather theoretical concept is actually measured in real life. Eg. I think it is a sensible expectation that if inflation was said to be 2% for 20 years then I should be able to buy a house that cost $200K 20 years ago for ~$300K now. This expectation is worlds away from reality which then prompts people to question the way inflation is measured.

I know you wrote that you don't really have the inclination anymore to educate on the topic but I for one would be grateful for any pointers how to explain the above discrepancy?

Good X and Good Y both increase in price over some period of time, but one does by 2% and the other by 4%. What is the true value of inflation? 2% or 4%? Or is it 3%? Or is it 3.5% because you buy one of the goods twice as often as the other? That's a question of first philosophical origins, and there's no "right" answer.

Particularly if one of those is a house and in the period of time mentioned houses not only got more expensive but they changed in character, being more resistant to earthquakes because of reinforced foundations, and because the fire departments built near them got new hoses for their trucks. So if houses were the one that went up by 4% but they also increased in quality, should we "count" them as having gone up by 4%? After all it's not like your money buys you 4% less house since it actually buys you a slightly different house but for 4% more. Now multiply the number of products and dimensions by a thousand or hundred thousand each and we have the true problem of compiling CPI.

> Good X and Good Y both increase in price over some period of time, but one does by 2% and the other by 4%. What is the true value of inflation? 2% or 4%? Or is it 3%? Or is it 3.5% because you buy one of the goods twice as often as the other? That's a question of first philosophical origins, and there's no "right" answer.

Shouldn't the solution basically be how much monthly or yearly does an average consumer spend on x good, and then that is included in the calculation of inflation by that amount.

So if the average consumer spends 30% on housing, then housing should be 30% of the measurement.

Yes. What then should happen when Good Z is invented and grows from 0% to substitute for 25% of Good Y?

How should a measure of inflation track that?

What if Good X becomes half as expensive per unit but people consume twice as much of it as a result? Should that be reflected as a reduction of inflation? If housing per front door goes up by 100% but only up per square foot [or room] by 50%, should the inflation rate of housing be 50%, 75%, or 100%?

TBH looking at my budgets I think this type of argument is missing the point.

Excluding savings, My budget boils down to discretionary and non-discretionary spending. Roughly 1/4th of my budget is fully discretionary and will vary year to year with what I like to do, tracking inflation on the discretionary portion seems like a high difficulty activity which ultimately doesn't matter to my perception of prices.

The remaining 75% of my budget is non-discretionary covering items like

- Housing ~1/4

- Childcare ~1/4

- Food ~1/8

- Non-discretionary expenses (repairs, car, phone, computer, etc. ) ~1/8

I'm fortunate that my healthcare is inexpensive at the moment, but it's pretty straightforward to calculate my future expected health costs and my previous education costs. I'd judge that calculating inflation on the non-discretionary portion of my budget should be trivial, small items like phones/computers simply do not add up to much relative to the big ones like housing, childcare, food, health, and education.

Ironically the CPI seems to focus on the magic basket of goods and not what will actually move the needle for perceived costs by most individuals.

Even discretionary and non discretionary is a contentious item and in a CPI has to be defined.

For example: is TV service discretionary? Is Internet service discretionary? Is broadband Internet access discretionary?

I just checked. Bell TV + Internet is advertised as $120CAD right now. Cell service combined with that add $70CAD. Per month. With taxes on top that's round about $2,620 per year if we are talking Single person household.

Now it depends on where you are and whether you live alone or not and such. In Toronto as a single person at the median income this alone can be 4.5% of your net income. I'd say that moves the needle. I pay less than half of this with a different ISP and cell provider + Netflix. Of course the precise calculations change as we move between cities and provinces as well as single person vs. families etc. as base costs get shared.

The hypothetical single income earner that we are debating would pay an average rent of $2250/mo for a 1-bedroom in Toronto. Roughly 10x the cost of TV, internet, and phone. This cost has risen from ~$1750/mo in 2017 at roughly ~10% per year.

For perspective, our hypothetical individual would be experiencing house price inflation equal to a new TV, phone, and internet bill every year.

Absolutely agreed that there are worse categories than your phone/internet/tv bills. And yet even this relatively small and apparently I Yunsignificant non-discretionary (or was some of it discretionary? Or all of it?) item still makes up 4.5% of your net income. That I still call significant.

Once I have a house the inflation on that also doesn't affect me that much any more (sure, evaluations increase my tax bill - which btw is a NA thing that is irrelevant in Germany for example as long as you have a mortgage) but other items do.

The underlying problem here is that one of our numbers must be wrong. The options I could see are

1. The marginal cost of housing has little to do with what individuals pay in the short-term.

2. The median income earner requires or will require substantial subsidies or raises to keep pace with the increased costs of their home. Roughly 3-4% per year assuming that housing is the only item inflating.

3. Either the median income, median rental, or tv+internet prices we've quoted are wildly off the mark.

I'd bet that #2 is the correct interpretation of the statistics. While option 1 is possible, it hides low-quality substitutions and assumes that one can always make a substitution such as living with parents for longer.

All very fair points. I think one thing that makes a huge difference is whether you rent or own. There's obviously so many nuances to this all.

I realize that we (or at least I am) also mixing up various things, even though I chose to quote a particular city's median income for the example.

If you are renting and your rent goes up 10% that obviously has a large effect. If you have a house and rent goes up 10% you don't care at all. If rent goes up like that, it's probable that house/condo sale prices go up too and you have to pay more in taxes. I bet the increase in taxes makes a smaller hole in your pocket, though I might be completely wrong. But this also depends on whether we stick with the example or move on to other countries, where there's no such thing as separate municipal/school taxes or where rent control is in place.

The problem is laymen care about cost of living, not CPI. But news agencies commonly talk about inflation with CPI rather than an actual cost of living. Which is what matters to people living ordinary lives.

Given this, the answers to your questions should be obvious. The answer, as far as laymen are concerned, is 3.5%. Improvements don't matter either. If we eliminated every car other than a Porsche, as far as laymen are concerned then car inflation went up by around 150%.

>Given this, the answers to your questions should be obvious.

If the answer seems obvious, then the question isn't fully understood, because there are trade-offs involved in CPI calculations.

There's no such thing as a "layman." Different people in different regions experience different CPI. Inflation for all goods in the Northeast might be 2.1% over the past ten years, but could be 1.6% in the South for the same basket. that might not sound like much, but that means that inflation is rising 25% faster in the Northeast.

No matter what you do, CPI at a national level won't accurately reflect any group. People in the South will claim it's way too high, and people in the NE will complain that it's way too low, etc, etc.

If you want real numbers, relevant to your situation, then the BLS provides the ability to calculate your own person CPI based on what you buy and where you live.

Yes, because CPI is a product of both market forces and changes in money supply. The former is not controlled much by anyone, while the latter is controlled by some very rough and not easily predictable knobs held by guys at Fed. Guys at Fed are committed to keep CPI at something like constant 2%, so the must turn these knobs, but for that they need a good feedback as to what their movements are doing.

And sure, they could use something different as a measure of inflation than CPI, but what would that be, and why it would be better than CPI? These questions need to be answered first before we move away from CPI.

The Fed's dual mandate is very important here. And there's some movement toward "automatic QE in case unemployment starts to rise" - https://www.stitcher.com/show/voxs-the-weeds/episode/fix-rec... (Matt Yglesias wonktalks with Claudia Sahm, very recommended)

CPI is very important, but the labor numbers are much better (since they are easier to measure), so CPI might become a secondary (high level, target) metric over time.

The problem with applying CPI to an individual's situation is that nobody is average across several dimensions. One person might live in the midwest an have experienced next to no housing inflation, modest food inflation, and be heavily reliant on gasoline (which has gone down in price over 10 years) due to rural living.

The same person living in Seattle might see housing prices double since they rent, food prices explode, since they live in a gentrifying area where low-cost grocers are replaced by high-end organic ones, and gasoline might not be a huge component of their spend because they drive a beater Prius 15 miles a day.

Those are two people, buying pretty similar things who experience inflation very differently than "average." Luckily, the BLS does provide different CPI figures to account for different groups of people -- for example only looking at inflation data for Seattle -- but people generally never discuss those.

> My layman understanding of inflation is that it is the measure of change of purchasing power a unit of currency has over time.

That's loosely correct; but general inflation is the change in purchasing power for currency buying final consumer goods and services, not assets which are intermediary stores of value. Purchased homes are assets (actual or foregone but using a home you own yourself) rents are consumption expenses.

> I think it is a sensible expectation that if inflation was said to be 2% for 20 years then I should be able to buy a house that cost $200K 20 years ago for ~$300K now

It's not. Specifically, that would be the fallacy of division, even if your basic understanding of inflation was correct. The change of an aggregate is not identical to the change in every subset of the aggregate.

Other already gave good answers. The main part is that

a house is not a consumption product - it is not "consumed" (used up) in a limited timespan, but rather, a bundle of a long-durable part (building) and an ultra-durable asset (land). Pretty much all durable assets have increased in price since the 1980s in tandem with falling interest rates[1]. The cause of the long term decline of interest rates is largely unknown.

The BLS largely circumvents this by using rents, actual rents for renters, and owner equivalent rents (OER) for owners. This is done by asking owners what they think their house would rent for, and using those increases for the housing/shelter component of CPI. Rents (which make up 1/3 of CPI) have increased faster than the general CPI, but not as much as house prices[1], likely because of the interest rate decrease.

There are some other complicating aspects around house prices (city prices increased faster than rural, houses sizes grew while household sizes shrank[3], so part of higher prices is just people buying more). But I believe the main aspects is really falling interests rates. A proper decomposition and attribution of most aspects probably takes months of work, enough for a econ Master theses. That's why I mentioned I don't have the energy for that. Nor do most other bloggers/pop-article writers, so they just go for popular appeal and clicks, by telling you why everything is getting worse and more expensive for you.

Wouldn't it make sense for the basket of goods used to compute CPI to try to blend the impact of rents (which are included) with "affordability" of buying a house (maybe measured as the carrying costs of an average property per month, which would exclude principal payments)?

Otherwise, because rents and house prices don't always move in lockstep, it's hard to measure the buying power of a dollar over time.

When thinking about purchasing power over time or between different cities, I often think of it as "assume I'm buying 1/180th of an average house in that city each month" as part of a representative basket of goods.

Not the parent, but the answer here comes down to two simple things:

1. Home prices are not captured in CPI, only rents.

2. The headline CPI is a national number. Home price inflation has actually been somewhat tame overall in recent history (2-3% per year), but it has been very geographically uneven. Some places have experienced basically no inflation, while others have tons of it.

Here is the graph for home price inflation in the San Francisco region: https://fred.stlouisfed.org/graph/?g=BLdf . You can see that it's often double digits, and certainly much higher than any headline inflation rate.

> Home prices are not captured in CPI, only rents.

Yes, because CPI measures cost of buying service of housing. Usually, if housing prices rise, so do rents, pretty much in accord, so monitoring rents already gives you a good view on housing affordability. The extent to which cost of renting is decoupled from house prices is largely explained by changes in interest rates: lower interest rates make mortgages more affordable, which allows more bidding for houses and pushes prices up. However, this on net doesn’t do much to actual affordability of said house: at low rates, the sticker price on a house might be high, but the mortgage payments will still be low. Conversely, in the 70s and 80s, boomers saw many cheap houses on the market, but at mortgage rates of 10-12+%, these were even less affordable than houses are today.

That’s why CPI only includes rents, to make an apples-to-apples comparison.

> Usually, if housing prices rise, so do rents, pretty much in accord

While this would theoretically make sense, it's not actually very true in the United States. There's a significant speculative aspect to housing in some markets that results in price increases far higher than rents would sustain (this effect is actually more prominent in other markets, e.g. Canada).

I think it actually is very true in the United States, outliers like SF notwithstanding. US as a whole is significantly more like Plano than like SF. Sure, that does little to make Bay Area residents feel better about crazy housing prices they deal with, but theirs is by far not a typical American experience.

You're right that we should probably ignore San Francisco and a few others to portray the typical American experience.

But it's still not obvious why for example Atlanta (22.6x) has almost double the price-to-rent ratio of Milwaukee (12.4x) if not due to speculation. Those both seem like fairly "typical America" cities to me. Would you expect Rent in Atlanta to spike heavily in the coming years? Or is the distinction you're making more about urban vs. suburban? (Since my link is just a mediocre blog, it's not clear if those numbers refer to city or metro area.)

> Home prices are not captured in CPI, only rents.

This is literally correct, but misses the essential feature of the housing issue in CPI: A large component of the housing contribution is "owner's equivalent rent" (OER).

Last I checked (now years ago), there is a survey where BLS essentially polls homeowners with the question "How much would your house rent for?" That number is then used for the OER component of CPI.

As the housing bubble was popping, BLS felt it necessary to explain the divergence between rents and OER [1]. The statistic was an absolute mess then, and I haven't seen any reason why it got cleaned up since, although I have not followed it closely in recent years.

> I think it is a sensible expectation that if inflation was said to be 2% for 20 years then I should be able to buy a house that cost $200K 20 years ago for ~$300K now

Housing is a bit particular because it's a good that's almost always purchased on credit. You'd want to look at the monthly costs of housing (mortgage payment) as opposed to the sticker price, since the total cost that's affordable fluctuates based on the interest rate. Twenty years ago, the interest rate on a 30 year mortgage was about 8%, contrast it with the about 3% rates now.

>My layman understanding of inflation is that it is the measure of change of purchasing power a unit of currency has over time

>I know you wrote that you don't really have the inclination anymore to educate on the topic but I for one would be grateful for any pointers how to explain the above discrepancy?

obvious answer: it's not "price index", it's "consumer price index". First paragraph from wikipedia:

>A consumer price index measures changes in the price level of a weighted average market basket of consumer goods and services purchased by households.

Not an economist either, but I think I can explain that one. CPI is a single rate derived from the change of price in a bunch of goods (houses aren't actually included, as another person noted). A change in CPI tells you nothing about the change in price of a particular good in it; it only tells you how much more expensive those goods are if you bought all of them.

Just as an example, let's say milk and eggs are the only thing on the CPI, and they're both at $2. If milk goes up to $3 and eggs go down to $1, the CPI says there was 0% inflation (assuming they don't adjust for quantity consumed). So rent can go up a lot without affecting the CPI too much, as long as the cost of other goods goes down enough to offset that increase.

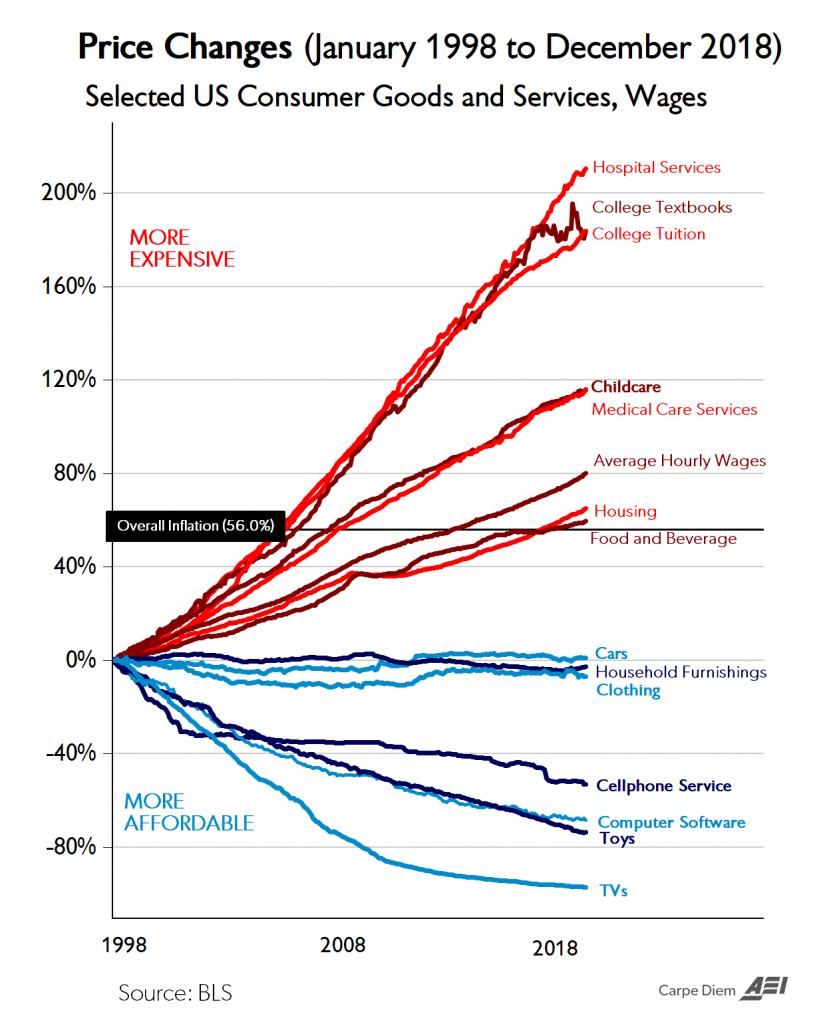

Here's a graph showing inflation of different goods between 1998 and 2018: https://realinvestmentadvice.com/wp-content/uploads/2019/04/... As you can see, a lot of "mandatory" things inflated a lot, but the increase in those costs is offset by the decrease in electronics prices.

The CPI is meant, afaik, to gauge the increase in the cost of living for the "average person". It's useful for driving fiscal policy, but it's not terribly useful to laymen, imo (and that includes myself).

Real wages are more interesting to laymen, I think. Those are effectively wages adjusted over time based on inflation from CPI. Using your housing example again, it doesn't really matter if a house cost $200k 20 years ago and costs $400k now, as long as wages doubled over the same period, all things equal. Inflation is fine (for the purposes of buying a house) as long as wages rise to match that increase.

The reason many people can't buy houses anymore is that real wages have fallen. https://en.wikipedia.org/wiki/Real_wages Wikipedia has some interesting info on that. In an ideal world, inflation decreases the purchasing power of a dollar, but your employer gives you more of them to compensate for that. That never happened for many people.

> Using your housing example again, it doesn't really matter if a house cost $200k 20 years ago and costs $400k now, as long as wages doubled over the same period, all things equal. Inflation is fine (for the purposes of buying a house) as long as wages rise to match that increase.

You are missing one crucial aspect: interest rates. 20 years ago, typical interest rate was 8%, so mortgage payments on $200k house were something like $1400/mo. With today’s rate of something like 3.2%, the payments on $400k house are something like $1700/mo, which is 20% higher. To keep the affordability the same between now and then, the nominal wages need only grow 20%, and if they actually doubled, this would hugely increase affordability.

It doesn't track well with the experience of people on this forum because young professionals tend to live in cities with crushing rental markets, especially Silicon Valley. But the whole country, particularly thoseliving in houses not in New York or California, have a different experience.

it also has real world consequences as CPI is used as a metric for all manners of things, including COLA increases for Social security, as even some private companies.

You forgot the quotes around "economist". Economics is still not science, it's getting closer; but the whole field ignores stuff and deals with spherical cows to simplify complexities.

You know you can be a "professional X" without X being a science, right? It simply means that X is your profession. Some examples of professions that are not sciences: racer, chef, journalist, writer, singer.

Yes, but those professions have agreed upon norms and standards that can be measured.

Did you win, Does it taste good, is it accurate and easy to follow, etc...

Economists are all over the place you an pick and choose different theories to support any Point of view.

I'm sorry, but no, they don't. Out of all of the examples I used, only one has agreed-upon norms and standards that can be measured: racing.

All the other examples I used -- chef, journalist, writer, singer -- can win awards and recognition: Michelin stars, Pulitzer, Hugo, Nebula, Grammy, and such. Those are good indicators of their accomplishments, but that's not the same as having a set of "agreed-upon norms and standards that can be measured".

And if you decide to relax your criteria and say that having those is acceptable, then guess what? There's a Nobel Memorial Prize in Economic Sciences, and a slew of other awards for economists.

Like it or not, studying economics is something that people can and do dedicate their lives to. Would it be better if we had more clarity, transparency, and consensus when it comes to what they do? Absolutely. But dismissing the whole profession out of hand is unhelpful.

I don't dismiss the profession. I dismiss the professionals. They need to provide more proof then identifying as a professional exactly because it is not a science. I also need to understand their biases and agenda.

Honestly it's usually easier to just ignore them and give their opinion no weight greater then anyone else.

I agree with everything you wrote except that last sentence, and that is exactly what I refer to as "dismissing the profession". Understanding their biases and agenda is by no means trivial, or even easy, but it's most likely a lot easier than spending all the time they spent on studying the subject matter.

>The consumer price index is a series of numbers designed to help people understand what dollar-denominated figures mean to ordinary people going about their lives, spending those dollars.

It's done an absolutely terrible job for the past 15 years, for my lifestyle and where I live. I suspect it hasn't reflect many other people's budgets either, hence the common argument of official CPI figures being nonsense.

I don't even have to look at anything other than the changing health insurance premiums/deductibles/co pays/out of pocket maximums to prove it, not to mention real estate, childcare, taxes, and education. It eviscerates any downward effect tech products and grocery prices might have.

My anecdote is as valid as your anecdote. Life got cheaper over the past 15 years, not counting changes in family size.

I used to have insurance co-payment, a deduction from my paycheck, and an unreachable out-of-pocket maximum. All of that has changed.

I used to pay about $1200 rent for a crummy house in a dangerous neighborhood. Now, with a paid-off mortgage, I pay just $266 for property tax on a house that is 3109 square feet on 0.39 acres.

Childcare is my wife, so $0 then and now. Income tax remains $0 due to child deductions. Sales tax is about 7%, relatively unchanged.

Education is a new expense compared to 15 years ago when nobody was in school. If I look back more than 20 years instead, to when I was in college, I can see that college has gotten cheaper. Tuition is a tiny bit lower, but the big change is that tuition and books for the first couple years are now free if you get it done in high school. That cuts the price in half.

This is not to say that I pay less. I now have a huge family. Things are cheaper, but I'm buying much more.

Just so we're clear, here, you've already gone from:

> I can see that college has gotten cheaper

to

> I'm not so sure college has gone up in price

You seem to be good at finding system hacks for your own, and/or proximal cases. But you continue to generalize your own experience(s) in a way that almost certainly doesn't broadly apply.

- Student loan debt at graduation has increased 76% since the Class of 2000, a growth rate that outpaces the rate of inflation by 41%

- After adjusting for inflation, the average student loan debt at graduation has increased 326% since 1970

- Since 2003, the national total student loan debt balance has grown by 602.5%

Of course, tuition prices and student loan stats are different things. But the loan stats make it hard to argue that there is much discounting - in general - of tuition prices

> Many economists, mind you, believe CPI doesn't correct quite enough, and suspect that it overstates the inflation it hopes to measure by around 1%. This is because it tracks the actual prices of a certain "market basket" of goods with specific products in it, and that basket gets out of date, as people substitute products.

Please provide a source to back up this claim, everything I've seen says inflation is /under/-stated, not over. CPI absolutely takes into account substitute products and CPI is not simply tracking a basket of items over time.

> Many economists, mind you, believe CPI doesn't correct quite enough, and suspect that it overstates the inflation it hopes to measure by around 1%. This is because it tracks the actual prices of a certain "market basket" of goods with specific products in it, and that basket gets out of date, as people substitute products.

These substitutions are tricky, if hypothetically a consumer can move from eating fresh local produce to preserved canned produce then it's likely they will make the switch under price pressure when fresh produce increases in cost by 2x. You could calculate CPI based on the new realized purchasing patterns - or you could calculate it based on the desired purchasing pattern.

Basing CPI on realized purchasing behavior will lead to errors in how inflation is perceived or where consumers are trading quality for cost. From a monetary policy perspective ignoring this consumer tradeoff could lead to sudden shifts in CPI when consumers run out of quality substitutions.

I'd argue we've seen this in housing in the major cities where first home prices were excluded for rental equivalent, then rental quality fell in both the amount of space available in a unit as well as the overall quality of the unit. Eventually you hit the wall where quality can't be traded off any longer and you're left with many people who can't legally house themselves.

There have been several eras in computing where a peripheral had a surplus of capability that applications were not making compelling use of. Most especially video cards.

Then one day cards are 'good enough' that someone builds an application that leverages this power, and all of a sudden that becomes the new baseline. Over night you went from having a video card that is three times what you need to a third of what you need.

We might consider availability of seafood to be a given now, due to improvements in food logistics. But it wasn't always the case. For sure strawberries in winter were just not a thing one would buy until relatively recently.

If I wanted vitamin C in February before it would probably be in the form of jam or tomato sauce.

> But if someone's "punishing savers" and "perpetuating consumerism", it's not the index, and it's not the people compiling the index, and it's not the people trying to make the index more accurate by adjusting for quality.

I’ve seen this a lot around the net and I’m honestly and genuinely curious. What drives you to defend the CPI?

He's right, defending the CPI calculation is almost criminal. Many people on fixed incomes that are adjusted based on the CPI are negatively affected. This bogus formula will be conveniently altered to stay under 2% if inflation creeps into the basket of goods being calculated.

Perhaps, but the right way to approach this is to point out the factual errors, rather than making thinly veiled insinuations that his opponent is a shill for the BLS or whatever.

>defending the CPI calculation is almost criminal

Ah yes, because the only possible explanation for why people don't hold the same beliefs as you is because they're acting with malice.

Please don't post insinuations about astroturfing, shilling, brigading, foreign agents and the like. It degrades discussion and is usually mistaken.

Assume good faith.

>Many people on fixed incomes that are adjusted based on the CPI are negatively affected. This bogus formula will be conveniently altered to stay under 2% if inflation creeps into the basket of goods being calculated.

All this does is provide a motive for why CPI might be wrong, but stops short of providing evidence or counter-arguments.

I have no intention of refuting his arguments. I have no strong position on the value of the CPI. OTOH I’ve noticed repeated vociferous defenses of the CPI across various Internet forums which seems out of the ordinary for me, so I’m naturally curious in what drives it. This is not trying to dismiss his argument, I just want to understand from where it’s coming because I think I’m missing something.

I have occasionally come to the defence of CPI in several threads. What drives is usually that the critic shows little knowledge about that the CPI is and/or how it's actually calculated. There are real technical issues with CPI estimations. But forum and blog posts rarely reach beyond the level of "everything I bought/want to buy is getting more expensive faster than the CPI, so it must be bogus".

It triggers me in a similar way, I think, as comments like "my (sisters'/neighbours') kid got really sick after his vaccination, so vaccines are very dangerous". A small number of people really do get sick after (and sometimes even from) vaccines, and probably no amount of research will override their personal experience. But it's a bit disheartening if the level of discourse never rises much above personal experiences.

This is because media and government (in various computations) use CPI when talking about inflation, so it is natural for them to become used interchangeably.

Since CPI doesn't reflect inflation, it is natural to criticize it for failing at that. Maybe it was never meant to reflect inflation, but that seems about as futile as trying to argue for the proper, original meaning of the term "hacker", not what media made it to be.

do you realize all the calculations use CPI?

the bond market is highly manipulated because of that, why have a market then?

why are retail accounts in germany, netherland already negative rates? does that make sense to you?

can banks make money that way? danger of nationalization of banking?

personal beef? no. I thought this is a forum for civil discussion and reasoning?

Whose calculations? The Federal Reserve's calculations? The Federal Reserve has access to a variety of data sources, and while the CPI is the one that gets the press, they also use series like the chained CPI, the producer price index, bond yield curves, unemployment (and not just U3, but things like U6 and the labor force participation rate).

If all you hear about is vanilla CPI, well, that's because you're looking at a newspaper.

Anyway, as I said. You have a beef with the Federal Reserve.

> why are retail accounts in germany, netherland already negative rates?

Public policy, as effected by the European Central Bank. Perhaps you have a beef with them too.

> does that make sense to you?

I mean, it makes sense as in "I understand why they do it", not as in "I think this is a great thing".

> can banks make money that way?

I've read that low interest rates do, in fact, squeeze their profits, though with regards to Germany the "three-pillar" system is crufty and weird and squeezes profits too. For instance, here is this lovely article I saw a while back, whose subhead notes "Low interest rates and the three-pillar system squish profits": https://www.economist.com/finance-and-economics/2019/03/02/c...

> danger of nationalization of banking?

I'm not sure what you're talking about any more. It seems very detached from the Bureau of Labor Statistics, or European equivalent.

Does the Fed look at inflation numbers within individual industries and metro regions?

Here's what I'm worried about: if you look at historical examples like say the 1970s inflation, or the post-Cold-War Warsaw Pact hyperinflations, or the post WW-2 hyperinflations in many European countries, prices didn't rise uniformly. Some industry or some region would experience very large inflation, and then eventually it would get transmitted to that industry's customers, or their suppliers. It's basically a network contagion, spread across the links in the economy.

We're seeing the early stages of this happen right now - that's what the article is about.

Powell's public comments are that "inflation doesn't turn on a dime" and "we're likely to see some localized price increases within certain industries, but no generalized inflation." The thing is - I know from history that the former can be false (particularly in wartime, and shifts from a controlled to a market economy, and the recovery from COVID has aspects of both), and the latter tells me that he's looking at the same data that I am but drawing the opposite conclusion. If 5% of firms are experiencing 30% inflation and the rest are experiencing no inflation, the PPI will read 1.5%. If that 30% inflation is in a core industry though (say food, or energy, or labor) and they pass it along to all their customers, then within 1-2 years you could have 30% inflation across the whole economy without passing through the 2% stage.

It's giving me COVID tingles from last year, where in March your overall risk of getting COVID in the U.S. was about 1:100,000, but your risk in NYC was 30%. Then suddenly your risk in Phoenix was 40%, and your risk in South Dakota was 50%, and then your risk in LA was 30%, and suddenly about 20% of the country has had it.

I don't really have a dog in this fight other than to point out your initial post was neither civil nor reasoned - and included not citations or facts.

I'm starting to understand what you're insinuating I think, but you still haven't made your point.

The European bond market has little connection to the American CPI. European rates are determined by a complex market of futures and interest rate swaps between various banks and markets. Knowing that, negative interest rates make plenty of sense, because interest rates in Europe are relative to other currencies -- unlike in the US, where interest rates are based in a single currency.

> CPI is a joke, they do something called hedonic adjustments to things like tech products etc.

Hedonic adjustments have very minor effects on tech products (which is one of the few areas I've seen a detailed impact analysis, though not recently enough that I have it at hand.)

> Technology is deflationary, things should get cheaper because we go after producing them in creative ways one demand is high.

And...they do. Hedonic adjustments have an effect on how that is reflected in inflation statistics, but they don't effect the underlying processes.

> CPI is absurd, it only perpetuates consumerism and punishes savers

I think your are (among other errors with that description) confusing measuring inflation with policies targeting a small positive level of inflation. CPI doesn't do either of those things.

Any measure of inflation is subjective. That doesn't make it B.S.

Inflation is a measure on a basket of goods. There is no single basket because people buy different things. This is why there is no single CPI statistic.

Find a CPI that works for you. The federally-provided ones go as fine-grained as income bracket and metropolitan area. They're extremely precise, but may not be accurate if you have unusual purchasing habits.

If they're not giving you a one-page report on the methodology for how they arrived at each individual point-in-time price figure that they recorded, well, I'm sorry, it's true, their methods are in that sense "hidden".

The input to CPI is secret shoppers visiting a variety of retail outlets, and buying things (or write down the advertised prices for things) without telling the retail outlet what they’re doing.

Publishing the particular products looked at, or even the particular stores visited, would invite market manipulation of the CPI figure by re-pricing the included goods.

Keynesian economics kool-aid, all the Phd Econ guys worship guy who had done some really shady stuff in his life.

Nobel prize in economics was started by Sveriges riksbank in 1968, just to perpetuate same ideaologies.

Shady af.

Non-Keynesian economists, like the neo-classicals for example or the market monetarists or even the more serious of the Austrians, don't disagree here.

The Fed uses PCE instead of CPI in their calculations. It might make your argument more convincing if you included an critique of PCE in addition to CPI.

> Technology is deflationary, things should get cheaper because we go after producing them in creative ways one demand is high.

And as a consequence the wages you earned by making tech year ago should have less value than the wage you earned today. You should expect small inflation. If you want deflationary money, wages should decline year by year.

If you want to be prudent, hold land, stocks, or bonds. Buy-and-forget with stocks, on average, outperforms both inflation, and actively managed portfolios.

until you need the money to pay big emergency bills, which at he wrong time can wipe you out no wonder there are half a million bankruptcies per year because of medical bills in the US

and 40% of people have no savin

and another significant portion doesn't have enough saving to spend time to invest in stocks, bonds and land(land also comes with perpetual high property taxes in most places in the US)

In the unlikely event you end up with giant medical bills, despite having health insurance, it doesn't matter whether your money was invested well, or poorly. The hospital will happily take every penny.

For the other overwhelming majority of life events, you should invest your savings prudently, instead of stuffing them into a mattress.

If you have no savings, this is a moot point - but so is inflation. Why do you care that money is losing value if you don't have any?

If anything, if you are in debt, you want inflation - because it lets you inflate your debt away.

More or less the author argues that stable nominal spending, ie a constant level of nominal GDP, is pretty much ideal. And would lead to falling prices as you suggest.

If you replace constant level with 'target a level of nominal GDP that rises 4% every year' you have pretty mainstream position.

Inflation measures are indeed somewhat subject. Nominal GDP has less suggement calls.

(It's still useful to try and measure inflation. But perhaps it should not be a policy target.)

I wouldn't call it 'both sides'. For one, there are more than two sides. For the other, George Sergin is very much some-kind-of Austrian. Perhaps the most interesting one.

Assets are items that generate cash flow. If you live in it, it's a liability and not an asset. Just because its value increases in relation to funny money doesn't mean it's generating cash flow. How much bitcoin do you need to buy a house?

Because you have to pay something to live somewhere (that's how gravity + weather works) there's a cost.

If you own vs rent you transfer that payment stream into servicing an asset. Assuming the asset goes up that's generating an implicit cash flow (one you will have access to later when you sell the asset).

If you can buy your house with cash then your "housing" cash stream is suddenly freed to be spent elsewhere, so you "gain" a cash flow you didn't previously have.

You can make a fair argument that this is a semantic quibble or one of the usual human self-deceptions but this is how people implicitly think of it.

I would disagree with that. Stocks that don't pay dividends don't generate cash flow either. Assets are items that are bought with the intention for them to generate value. That value might be cash flow, or it might be an increase in value so that you can sell it later. Not all assets generate cash in real time (most don't).

A house is an asset because a) it allows you to pay your liabilities for housing into an equity generating account, and b) people generally expect them to increase in value.

To put it another way, if they weren't an asset, people wouldn't care if they depreciated. I don't care that my car depreciates because it isn't an asset; I don't expect it to increase its value or hold its value.

> If you live in it, it's a liability and not an asset.

That's not a disqualification of an asset, if devaluation is outstripped by increased valuation over time. eg I live within a parcel, that parcel is not transformed into a liability.

>Housing prices reflect the cost of shelter for literally everyone who doesn't already own a house.

Right, but using the raw purchase price of the house isn't a good measure. Mortgage rates dropping would cause housing prices to go up even if monthly payments stay the same. What actually matters is how much you spend per month on rent, or if you owned your house, the imputed rent.

>Shelter is much closer to "food" than to "a piece of paper representing a stake in part of a corporation".

From a finance perspective there's no difference between a house and a share in a corporation. They're both productive assets that provide returns. In the case of a house, it provides shelter as a service, which can either be consumed by the owner (by living it it), or by selling it (renting it out). The only difference is that with a house, the relation to you is more direct, as opposed to a tiny fraction of a multinational entity.

> From a finance perspective there's no difference between a house and a share in a corporation. They're both productive assets that provide returns. In the case of a house, it provides shelter as a service, which can either be consumed by the owner (by living it it), or by selling it (renting it out). The only difference is that with a house, the relation to you is more direct, as opposed to a tiny fraction of a multinational entity.

From a finance perspective, theres no difference between food and a share in a corporation. They're both productive assets that provide returns. In the case of food, it provides sustenance as a service, which can either be consumed by the owner (by eating it), or by selling it (on the side of the road, or in a restaurant.) The only difference is that with food, the relation to you is more direct, as opposed to a tiny fraction of a multinational entity, and it depreciates much faster.

/s/

when you have a hammer, everything is a nail. When you see the world through finance, everything is a series of cashflows. The ability of a worldview to be applied to many things does not mean it is applied well to those things.

The primary purpose of a house is to, well, house people. Shelter is a necessity. People who are most vulnerable to inflation are the poor, who mostly rent, and thus pay current market prices. They also pay the most for healthcare on a per care instance basis, and often pay for college with expensive debt (5%) if they go to college.

If CPI, etc, are not measuring these price changes, perhaps we should use another measure that does.

>From a finance perspective, theres no difference between food and a share in a corporation

Clearly not. After you eat a bread, it's gone. After you live in a house it's still there. A better analogy would be something like a farm, which continuously provides sustenance as a service.

>The primary purpose of a house is to, well, house people. Shelter is a necessity. People who are most vulnerable to inflation are the poor, who mostly rent, and thus pay current market prices. They also pay the most for healthcare on a per care instance basis, and often pay for college with expensive debt (5%) if they go to college.

Should farm (or food producing corporation shares) prices be factored into the CPI as well? Like housing, food is also a necessity, and buying a farm would ensure you're protected against inflation in food.

Also, your point about buying housing as some sort of protection against inflation doesn't tell the whole story. Yes, it's a hedge against future rent increases, but here's no free lunch because the inflation is already priced into the price of the house. If rents are expected to 10x in the next 10 years, you can be sure that housing prices will grow accordingly. That's why price-to-rent ratios are insane in coastal cities.

> Clearly not. After you eat a bread, it's gone. After you live in a house it's still there.

After you live in a house a long time it falls apart. Capital Expenditure restores the asset to its previous value. Bread just depreciates faster. but can still be traded, bought and sold. In Japan houses are often only ever used by one family, and the house is destroyed when the land is sold. I am taking your insistence on a cash flow perspective to its logical extreme to show that it is not always applicable.

Corn is an asset when it is bought and sold. It is food when it is consumed.

> Should farm (or food producing corporation shares) prices be factored into the CPI as well?

I clearly say at the end that if CPI is not measuring these price increases we should use a different measure. I'm not sure you understand what's going on in this conversation, but food is in the CPI.

> Also, your point about buying housing as some sort of protection against inflation doesn't tell the whole story.

Where on earth do I say this? I say that poor people are exposed to inflation the most, especially increases in housing prices. We should have measure for what working Americans are exposed to, and do not.

>After you live in a house a long time it falls apart. Capital Expenditure restores the asset to its previous value. Bread just depreciates faster. but can still be traded, bought and sold. In Japan houses are often only ever used by one family, and the house is destroyed when the land is sold. I am taking your insistence on a cash flow perspective to its logical extreme to show that it is not always applicable.

1. the part of a house that's getting expensive isn't the house itself, it's the land. the multi-million dollar homes in san francisco would only be worth a few hundred thousand tops if they were moved to rural idaho.

2. corporations fall part too. more specifically, their physical assets (eg. machines in factories) fall apart. In both cases they're kept up by routine maintenance. The only difference is that in a corporation the maintenance is paid from revenue before profits/dividends are paid out, whereas in a house the maintenance is paid out of pocket by the owner.

3. it's not a question of deprecation. after you eat a piece of bread it's gone. that's not due to depreciation, it's due to you consuming it.

>I clearly say at the end that if CPI is not measuring these price increases we should use a different measure. I'm not sure you understand what's going on in this conversation, but food is in the CPI.

That's my original point. Rent (and imputed rent) is directly measured in the CPI, so there's no need to measure home prices.

I think the thing you're missing is that affordable starter housing allows people to both meet a basic need and also make an investment.

Consider three people, p1, p2, p3.

P1: works at job making $X and rents home entire life.

P2: works at identical job making identical $X and buys + pays off identical home.

P3: works at identical job making identical $X and buys + misses 10 mortgage payments on identical home.

P1 is WAY better off than P2 or P3. Literally, the difference between retiring and working until you die.

"can afford down-payment and also has enough stability to never miss payments" induces a VERY extreme nonlinearity in outcomes that CPI very much fails to capture.

I don't think anything you've said in this thread even comes remotely close to acknowledging the reality that over half of America lives every day.

> What actually matters is how much you spend per month on rent, or if you owned your house, the imputed rent.

Right, but in most markets rent prices track property values. The long-term upward trend in housing prices is inflation to approximately everyone who doesn't own a house. Which, significantly, includes approximately everyone under the age of 20 or not yet born.

> From a finance perspective there's no difference between a house and a share in a corporation.

From an investor's perspective, perhaps.

But most people are not buying housing primarily as an investment. Most people are buying housing primarily as a way to shelter themselves from the elements.

>Right, but in most markets rent prices track property values. The long-term upward trend in housing prices is inflation to approximately everyone who doesn't own a house. Which, significantly, includes approximately everyone under the age of 20 or not yet born.

and that's fine, because rents are tracked directly in the CPI.

>But most people are not buying housing primarily as an investment. Most people are buying housing primarily as a way to shelter themselves from the elements.

That's what they tell themselves, but from an analytical perspective there's no difference between buying a $1M house that provides you $5000/month return in the form of imputed rent, and buying $1M in stocks/bonds that provides you $5000/month return in cash, which you can use to pay rent.

> but from an analytical perspective there's no difference

Only for embarrassingly impoverished analytical frameworks.

Unless you know of a bank that will loan me seven figures at sub-3% interest rates based on 10% down and my income, and then let me spend that money in the stock market :)

>Unless you know of a bank that will loan me seven figures at sub-3% interest rates based on 10% down and my income, and then let me spend that money in the stock market :)

That does indeed make a x% return in the housing market more attractive than a x% return in the stock market, but has to be considered against all the other factors as well eg. diversification, actual returns (historically stocks have higher returns), risk (10x leverage also means 10x more loss), costs (stocks require no upkeep, houses require yearly maintenance), etc. At the end of the day though, it's still an investment as opposed to something you consume.

you've implicitly bought into the finance perspective, but it's not the only valid perspective by a long shot. consider at least the humanist perspective that people need to live in housing, and that it's not all about money and wealth. this is a critical weakness of many economics perspectives in relation to how the world really works, and an active area of research in economics.

I'll reuse an argument from another comment I made: sure, let's accept that we need to treat housing differently because people need housing. Should we do the same for food? People need to eat as well. Does that mean we should factor in the cost of arable land into the CPI?

you'd asserted a simple statement that houses are (edit: only) assets, which is trivially rejected by showing just one of many other valid perspectives. that there is a spectrum of goods and diversity of economic intricacy among that range doesn't validate your original statement.

the broader point is that asserting a house is just an asset is more a value statement (and more abstractly, an aggression) than a truism. investment has generally become decoupled from its intended purpose of producing value for the many, not just the few (i.e., the efficient allocation of capital), and this kind of misguidance contributes to that kind of misallocation.

>you'd asserted a simple statement that houses are assets, which is trivially rejected by showing just one of many other valid perspectives. that there is a spectrum of goods and diversity of economic intricacy among that range doesn't validate your original statement.

Not exactly, because there are two definition of "asset". From wikipedia:

>An asset in economic theory is a durable good which can only be partially consumed (like a portable music player) or input as a factor of production (like a cement mixer) which can only be partially used up in production.

apologies, you'd asserted a statement that houses are only assets (as amended above). houses can act as assets in an economic sense, but that's not their primary or sole purpose or source of value.

agreed because housing/RE is also used for speculation/investment and not just utility

what portion of valuation is utility in what point in time is hard to tell

How do you quantify waste? If I peel a potato, is the skin factored into the waste? I think there are a lot of foods we waste simply because you can't get all the yield out of the given mass, so on paper maybe you do only use half the pumpkin after you peel it, remove the stem, take out the guts, and turn it into a pie.

"thanks to a combination of poor weather, increased demand and virus-mangled global supply chains."

Seems like a lost opportunity to create so much anxiety with a long piece like this, to then only have this single line to hint at a reason for the rise.

Can anybody more economically minded clarify if this is just post-covid rebound supply chain prices or is this food prices adjusting closer to their 'real' cost?

Also what events do they refer to regarding 'poor weather'?

Have you ever left a city? Even in some suburbs it's possible to take a picture of someone with only a few houses behind them. In my smallish town, only tens of thousands of people, I live next to the busiest road and I could find an equally barren background about three blocks away.

Not living in an urban environment is not devoid of civilization.

For context the photo is actually from May 1, 2012: "two-year-old Aliou Seyni Diallo eats dry couscous given to him by a neighbor, after he collapsed in tears of hunger in the village of Goudoude Diobe, in the Matam region of northeastern Senegal"

Would you please stop posting flamewar comments to HN? The GP may not have been a great comment but "resurrect the idea of “civilizing” people" is a wild and gratuitously hostile stretch. The site guidelines ask you not to do that.

"Please respond to the strongest plausible interpretation of what someone says, not a weaker one that's easier to criticize. Assume good faith."

You've done it before, and even worse—for example here: https://news.ycombinator.com/item?id=26342816. And generally your account has been making a habit of posting unsubstantively and/or aggressively. We've asked you many times in the past not do to that, and we ban accounts that keep breaking the rules this way. If you wouldn't mind reviewing https://news.ycombinator.com/newsguidelines.html and using HN in the intended spirit, we'd be grateful.

So you're a proponent of the "give the fish" and not "teach to fish"? If the supplies flowing to them stop they starve again, so I am not sure you're right.

I think the biggest risk here - and the reason why talking about "bringing civilization" anywhere attracts strong pushback - is that historically, what happened was people ending up held hostage over supply of fishing equipment.

Giving hungry people fish obviously isn't a good solution, because then the fish giver becomes a SPOF. But also because the fish giver now has power over the hungry, and some givers will abuse it. Teaching people to fish doesn't work if they're still hungry. It also doesn't work if you're teaching methods that they can't employ. If your solution to the last problem is giving (especially licensing) them means to do fishing, then we're back to square one, with you being SPOF/risk of becoming exploitative.

The solution has to be helping people build self-sufficiency. That may involve giving money, or donating equipment and know-how - but with no strings attached, including non-obvious ones like "you'll have to buy spare parts from us, because your industry can't make them". The goal here is not absolute self-sufficiency (nobody truly has that), but avoiding the situation in which given society's affairs are being managed by outsiders, under threat of starvation or illness.

You can both give a person a fish, and at the same time teach them to fish as well. It is not, and never should have been presented as, an either/or argument.

Strange thought for someone writing a reply on a message board using a device there's no way they could build from scratch.

We've structured society in a way that not everyone needs to be a farmer (or microchip designer/electronic factory line worker) for people to obtain food/devices that access the internet. Are you a proponent of 'give the fish' because you didn't build the device you are typing in?

Sure, almost all central banks over the world have printed an astronomical amount of money. Even though they may state there is no significant inflation, I dont buy it and neither do many other economists. Stock prices, house prices and now, at last, commodity prices have gone through the roof... But you're probably earning about as much as you were a year ago, or less, if your industry was affected...

Inflation can be created, basically, by two things, an excess of demand respect to what the economy can produce or problems of supply.

Personally, I'm surprise at how robust are the global supply chains that have been able to keep things more or less normal despise what we have been through the last year.

The quantity of reserves created by the Central Banks are irrelevant if they are not spend in the economy. There are two effects to this "printing money": one is that the interest rate goes down facilitating borrowing from the private sector. The second is that governments have the ammunition to spend in stimulus. If the two things happen we could see inflation, but, notice that this the desired effect: compensate for a fall in the normal demand in the economy.

>" [..] central banks over the world have printed an astronomical amount of money. Even though they may state there is no significant inflation, I dont buy it [..]"

It seems to me that, in your model of the world, this should be leading to hyperinflation. If this is the case, my model of the world is wrong and I will make an effort to change it. I wish all the people has been predicting hyperinflation the last 30 years did the same if it doesn't happen. Somehow, I doubt it.

By now, the quantity theory of money based in the fractional reserve banking model should be discredited.

The examples given above seem like a textbook definition of inflation inside of a closed loop economic system.

That is not what the U.S. has and it’s definitely not the situation if a country has a reserve currency. The Triffin dilemma may hold the answer in that as you supply your currency to the rest of the world, you are creating local deflationary effects while essentially exporting inflation.

When the rest of the world begins using other systems than the reserve currency to conduct trade, the end result is that the inflation returns home as demand for your currency drops.

The grandparent says explicitly in the comment "all the central banks". We are not talking specifically about the USA.

Anyway, the "reserve currency" excuse doesn't explain Japan in the last 20 years or the Euro in the last ten. The theory is just wrong. I don't know what more have to happen for people changing their minds.

It's spending what can generate inflation, specifically, spending above what the economy can produce. If Biden tomorrow created a trillion dollar coin and keep it under their bed, there will not be inflation. If the Central Banks create reserves, the interest rate will fall to zero (but not more), and if, despise the low interest rates, nobody is borrowing, there will not be inflation.

I was referring more to your comment that inflation can be caused by only two things. It's much more complicated than that. In fact, if you were able to predict such things with an accuracy matching the confidence of your position, you would be a very wealthy person indeed.

Inflation is caused by somebody asking for more money and somebody else paying it.

That's a failure of competition keeping prices in check, and little else.

The wealthy person you are looking for is Warren Mosler. He retired to the US Virgin Islands many years ago having made a fortune off the back of people who believed in the Quantity Theory of Money

You can read his conclusions in the book "Soft Currency Economics".

Interest rates are at zero. When official inflation starts ticking up they'll raise interest rates which will deflate the stock & house price bubble and cut inflation off at the knees.

We have lots of things to worry about -- inflation isn't one of them.

> We have lots of things to worry about -- inflation isn't one of them.

I really hate this comment. I am worried about not being able to ever being afford a house for my family. Avg income in my neighborhood is ~49k but a 2 bed condo here are selling for 450K and getting outbid by 75k over the asking price. Its insane.

Maybe you already own a house and are happy that prices are up. But its really weird to tell other ppl what they should be worried about.

> Avg income in my neighborhood is ~49k but a 2 bed condo here are selling for 450K and getting outbid by 75k over the asking price. Its insane.

Sure, and your point about housing prices mattering is a good one (see my other comment on this story). But, this describes maybe a few dozen housing markets. Probably only a couple dozen if you cut out resort/ski towns. It's a regional problem, not systemic problem with the national economy.

It also describes the most populous US state. The median housing price is now over $700k in California, while the median household income is around $80k.

$700k is the median. The average is even higher, and especially so in “outlier markets” (where outlier here means the cities and surrounding suburbs where most people live).

Also, more Americans live in California than any other state. So if it’s an outlier, it’s an especially impactful one.

'few dozen' is what like 3 dozens? Assuming its a problem only in 36 markets. Wouldn't that be a 'national problem' ? 36 markets should covers a majority of population in the country.

Because relatively few regional housing markets have non-luxury 2 bed condos going for $525,000 (75K over 450K, per your original post).

E.g., in the Midwest you'd have to be in a nice part of Chicago or choosing the most expensive city neighborhood of a mid-sized city to find a meaningful number of $525K 2 bed condos. And even then, spending that much on a condo is 100% an unnecessary luxury. 10 minutes in any direction prices will crater, and by the time you get to the suburbs starter homes are from the $200s and $525K is a mansion. For the entirety of the midwest and most parts of the south.

Even on the coasts $525K for a 2 bed condo is a Big City thing. E.g., $500-$700K is the going rate for 2 bed condos in most of Boston, but drive an hour away from Boston in any direction? Not so much. Hell, even Wakefield has a 2 bed condo below $300K and that's only a 25 minute drive. And that's one of the more expensive housing markets in the US.

Living 20 minutes from major city centers via public transit has become a luxury, sure. But it's just not accurate to say that $525K for a 2 bed condo is "normal" in the US. It's not. It's quite specific to a very high CoL markets.

Ah yea i see what you mean. that might be an exception to suburbs of altanta. It was just an example of insanity of housing market in USA. I was not implying that the going price of condo.

Our old apartment in Chicago, which was in a nice neighborhood had its rent prices drop by at least $500/month. It might be more now.

When I look at real estate in general in Chicago, it's been dropping a little, not a ton, but it's not like how other are describing the huge increase in housing costs in other parts of the country.

It seems like there are big regional differences going on with housing costs in the US. Supply/demand and policy I'm guessing are making the difference.

This attitude that the market must always go up has never worked out historically, just makes the eventual reckoning that much worse.

Fortunately that mentality means that renters like my wife and I who want our future kids to grow up in a good house in a quality school district can just keep saving money, waiting to capitalize on the inevitable normalization when all the speculators and eggs-in-one-basket people fail to learn from history... again.

But at least the bubble popping would make it easier for the middle class newcommers enter the market.

Just inflating the bubble further, as every European bank and government is doing, to make existing property owners richer on paper and get their votes, is not a viable long term solution.

IMHO, it can't pop sooner. Houses should be for living, not for speculation and hoarding wealth. The younger generations have been screwed enough by the old established wealth hoarders.

I was around during 2008, that's exactly the opposite of what will happen. Financing will dry up and the newcomers will find themselves in a highly competitive rental environment with inflated prices, while the banks and wealthy snap up SFH's for pennies on the dollar.

Maybe the government can raise rates and offer some kind of refund to people who bought their first house in the last year?

Otherwise, the number of people in that "put their life savings as a downpayment on an overpriced house" category is only going to grow, making the problem worse when the collapse eventually happens.

>offer some kind of refund to people who bought their first house in the last year