NFTs were supposed to be an end-run around the Howey Test. ICOs were clearly securities offerings, and the SEC shut down most of those. NFTs were specifically designed to evade that test, by claiming they were really "digital artworks". This one, though, was clearly marketed as Make Money Fast. The Securities Act of 1934 has a "duck test" definition of security - if it is marketed, bought, sold, and held as a money-making thing, it's a security. The contract terms don't matter. This is because creative financial scams long predate 1934.

> The Securities Act of 1934 has a "duck test" definition of security - if it is marketed, bought, sold, and held as a money-making thing, it's a security

That doesn't seem right. You're missing a really fundamental part of what makes a security a security. Let's steal the cut phrase from investopedia

> an investment contract, for the purposes of the Securities Act means a contract, transaction or scheme whereby a person invests his money in a common enterprise and is led to expect profits solely from the efforts of the promoter or a third part

Investing in a common enterprise is a really key part.

A random beeple NFT wouldn't meet that definition, even if marketed as "this hot new thing that's only going up in value". The SEC isn't stopping people buying daft things.

> The order finds that Impact Theory encouraged potential investors to view the purchase of a Founder’s Key as an investment into the business, stating that investors would profit from their purchases if Impact Theory was successful in its efforts

This is where it differed from many other NFTs that aren't securities.

The good news is that judges can read the law and interpret it without having a myopic focus on specific wordings. They also don't use investopedia as a legally-binding source.

Whether an NFT (or any other crypto token) is a security is still very much up in the air, and I am assuming is not able to be uniformly defined.

People making noises like "you are investing in a project" and "there will be airdrops to NFT holders" sure seem like they are trying to run an unregistered securities offering. On the other hand, tokens like LINK (which you spend to do call APIs) and NFTs that are sold purely for the art don't really seem like securities. Even tokens like ETH or BTC could be considered currencies/commodities rather than securities despite all of the "project" language.

People are trying to over-complicate this even though the lines are clear. The intent is here what matters regardless of the implementation. Are you selling a "future expected outcome" or are you selling an art piece (or whatever other junk) with no strings attached. Of course, selling the art piece without a proposition to an increase in value will not attract "investors".

> Even tokens like ETH or BTC could be considered currencies/commodities rather than securities despite all of the "project" language.

BTC is, also according to the SEC. The problem with ETH is that they did an ICO early on the life of the project. I think that's why the chairman of the SEC refused to answer. They don't want to make it not a security so that they don't create a precedent. ETH foundation ICO might be the biggest mistake they ever made. It'll never go away...

Bitcoin is getting a pass mostly because nobody has any control over Bitcoin. There might be a loose community project, but Bitcoin is basically frozen in its current state, with no innovation. It's really hard to argue there is a common enterprise when there isn't really an enterprise at all.

> ETH foundation ICO might be the biggest mistake they ever made

It doesn't really matter if the Eth foundation did an ICO in the past or not, the simple fact that they are a coordinated project with a strong leadership structure who exercise quite a bit of control over the future of Eth is a strong indication that an "enterprise" exists.

The main reason why SEC are hedging their bets over ETH is that they don't actually know if it's a security. It's not the SEC who defines what's a security or not (though they often offer advice). The definition of "security is actually defined by the courts, so the only way to know either way is a court case.

And the SEC clearly wants to create some legal precedent by prosecuting cases that are much more obvious.

Also... the status of something being a security isn't necessarily static.

Just because Bitcoin is considered not a security now doesn't mean it will never be considered a security. If the bitcoin miners decided to band together and take active control over the direction of bitcoin innovation, then its current excuse would evaporate. If they transformed it into something that was obviously a security, then no amount of "But the SEC previously said bitcoin wasn't as security" will protect it.

> Just because Bitcoin is considered not a security now doesn't mean it will never be considered a security. If the bitcoin miners decided to band together and take active control over the direction of bitcoin innovation, then its current excuse would evaporate.

This is a messed up logic. Of course, if you changed the fundamentals of Bitcoin, the consequences will also change. But saying that "Bitcoin is considered not a security now doesn't mean it will never be considered a security" implies that the same Bitcoin can potentially be considered a security. Which is an entirely different premise.

From what I've understood, the CFTC and the SEC have decided between them that the CFTC will worry specifically about BTC and ETH (and a few other coins that can reasonably be considered commodities), and the SEC will worry about the rest.

That is likely why the SEC chairman doesn't want to comment on them.

Footnote in the Supreme Court opinion: “The term 'security' means any note, stock, treasury stock, bond, debenture, evidence of indebtedness, certificate of interest or participation in any profit-sharing agreement, collateral trust certificate, pre-organization certificate or subscription, transferable share, investment contract, voting trust certificate, certificate of deposit for a security, fractional undivided interest in oil, gas, or other mineral rights, or, in general, any interest or instrument commonly known as a 'security,' or any certificate of interest or participation in, temporary or interim certificate for, receipt for, guarantee of, or warrant or right to subscribe to or purchase, any of the foregoing."

The test does not include any specification of what must be an investment contract, though. Things like fields of orange trees have failed to pass the Howey test.

The orange trees are there for the purpose of producing and selling oranges.

In the case of a plain NFT, all labor associated with a piece of art is done before the NFT is sold. There is no enterprise generating profit for the owner. It's just an asset where they hope the value will increase.

Sure it is. And all that language about how you are buying into a project or this will be part of a future game with an economy is all part of that art too, right? And all the promises of airdrops are part of the art done beforehand, as are all of the promises that early buyers will be the "1%" of the new ecosystem?

I would agree with you that an NFT in itself does not constitute a security. An NFT as it was actually used by crypto people is a different story, though. And I would say that the "NFT as a pre-investment in a project" is the norm, not the exception in that regard.

This posts reads like you don't understand the Howie Test. Literally, that decision blew away any offering designed to evade SEC rules. The Test is incredibly general and has never been defeated. Why do you think this time is different?

I don't think it's different. NFTs are not all securities, right? Just because people speculate with them doesn't make them securities just like baseball cards aren't securities. NFTs can be securities, the ones the article is about clearly are.

I need clarification on what that sentence means before I can even look for a good example! Otherwise I'll just point at something that decided to not be a security and never had enforcement. There's a million kinds of collectible that fit that category.

If it means that when the SEC invokes the rule it has never failed, then that probably just means they're going after the strongest cases. It doesn't mean you can't "evade" it.

I really appreciate the way the Howey Test matches the regulatory purpose, its operationalist approach to the question. That it's stood up to nearly a century of scammer "innovation" is admirable.

It does have the drawback of requiring some interpretation, some thought. But I think that's necessary. Rather than requiring regulators to keep creating ever-broader definitions of "security", patching every scammer hole, it throws the burden back on those wanting to innovate. They're supposed to stop and say, "Well what are we really up to here?" And I think that's where the burden should be.

My only real grumble is that the SEC gave the cryptowhatever world too much rope. I wish they had been faster off the mark, so there was less nonsense. But even there I can't complain too much. Generally I want regulators to be cautious squashing new things.

Not trying to kill the vibe of your comment, I just want to point out that the burden of proof historically has fallen on the accuser, the regulator, the plaintiff, (point is: not the defendant,) to prove that some behavior is illegal and problematic. So I’m not sure I agree that it’s good to foster a regulatory regime where everyone trying to innovate is questioning whether the political winds will change in the future and some new hotshot regulator is going to make their career by being tough on whatever they’re currently doing when last year nobody cared. Post facto regulation doesn't really do any good as you’ve realized in your comment—the damage is already done.

So at least I think we need to protect innovators by holding regulators to a statute of limitation on enforcing policy (like no bringing cases against activity that predates some signaling by the regulator that the interpretation is changing), and ideally require regulators to publish guidelines before they’re allowed to take legal action. Or maybe regulators should have to inform an innovator that they’re no longer in compliance with an updated perspective and provide them actionable steps that if taken would make them compliant, etc. prior to taking legal action.

I’m not saying there’s no room for interpretation practically, but this deal where the SEC sits silent on whether “crypto assets” are securities or not and the only way we’ll know is if they sue one of the innovators doesn’t seem particularly healthy either. It’s exactly why you can’t be held criminally accountable for something you did before it became a crime, and we should hold regulators to the same expectations.

The burden of proof to prove a crime still falls on the accuser. Nothing has changed there.

I also don't think the interpretation has changed at all. We're still using the Howey test. The SEC took no immediate position on the cryptoetcetera community's various inventions, but they certainly didn't give anything their approval that they have since withdrawn. I'll note how much the more socially legitimate end of that community have been asking for "regulatory clarity".

The problem is that they now have clarity and don't like it. And I'm sure they don't. They were hoping to sweep aside the regulatory regime set up in 1934, which was in response to the crash of 1929. But I don't think we need any particular safe harbor for people who tried to dodge regulators and lost.

> The problem is that they now have clarity and don't like it.

Yes. Any hope for looser rules from Congress went away when Sam Bankman-Fried went to jail. (He's currently complaining about the jail food in Brooklyn.)

If you want to know if the SEC will allow something unusual, you can ask the SEC for a "no-action letter". Three token issuers have obtained such letters.[1] Those are for game tokens, not Make Money Fast schemes.

There's also the route of registering your new thing with the SEC as a security. A few companies did that.[2] The STX token is a registered security. Didn't do much, but it's legal.

Registration is no guarantee of success, but it forces enough disclosures and auditing that a "rug pull" is less likely. Enough is on record that the people ripped off know who to go after.

I have very little skin in the game and certainly haven't dabbled in the NFT world. And I “don’t like” the idea that a regulator can essentially leverage ambiguous language to prosecute after the fact just to leave innovators on their toes. This is required to achieve your goal of innovators asking “should I be doing this”, because otherwise there are clear guidelines and nobody is left wondering.

Nothing has changed about the legal system, you’re right, but you expressed a desire to live in a more ambiguous regulatory regime where people are unsure whether they’re committing crimes or not because we’re okay with a changing interpretation of how regulations apply. That rubs me the wrong way and frankly feels pretty dystopian.

Yeah I agree that practically it’s good to not have a bunch of buffoons running around doing quasi-legal securities offerings by a different name. But would it really have hurt to have the SEC say “we’ll be applying the Howey Test to NFTs, if you plan to sell one we’d recommend consulting a lawyer versed in securities law before proceeding”. Were consumers really damaged when their founders keys weren’t worth anything? Who in their right mind even treats a founders key as an honest security? Seems like there’s some blame on both sides here.

It’s conversely not great to have consumers not using their brains, applying zero scrutiny, and buying into whatever the new street fad is then wailing for the Uncle SEC when their little crypto tokens became worthless.

In short, I don’t think you need an ambiguous regulatory regime to achieve a climate of healthy innovation. You just need the SEC to not drag its feet on action and a little up front “hey don’t be idiots we consider this stuff a security <insert reminder of penalties for violation of securities law> so do your homework”.

> But would it really have hurt to have the SEC say “we’ll be applying the Howey Test to NFTs, if you plan to sell one we’d recommend consulting a lawyer versed in securities law before proceeding”.

They did that a few years back for ICOs, sending out "You seem to be doing an ICO. Tell us why you don't need to register this as a security". The ICO market mostly evaporated. A few ICOs did a securities registration.

Embarrassing questions have to be answered in a securities registration. Like "Who are you?" "Where do you live?" "What's your previous financial experience?" "Do you have a criminal record?". Crypto people are scared of that stuff.

SEC contacting ICO issuer regarding need for registration.[1]

Form D, for small (under $5 million) issuers with a limited number of stockholders.[2] Free to file. Useful for legit small businesses, but not so much for crypto, because crypto issuers want a big "market cap" and lots of HODLrs.

Form S-1, for large issuers.[3] This is the classic paper form as a PDF, but today you file this as an XML document. Software to format the XML file is available from several companies.

Anyone can download those files and analyze them, plus, at last, the SEC web site has a decent web search interface that displays the financial info. Filing fee is $110.20 per $1,000,000 raised.

Misstatements on a form S-1 are felonies. One of the main reasons crypto bros hate this process.

I honestly don't think a year and a half from conception and marketing of the assets to charges by the SEC is all that slow, especially in a new market.

> It’s conversely not great to have consumers not using their brains, applying zero scrutiny, and buying into whatever the new street fad is then wailing for the Uncle SEC when their little crypto tokens became worthless.

I disagree.

A few centuries of experience make it pretty clear that there's a spectrum between highly regulated markets and unregulated markets. The highly regulated markets are a social good and beloved by both investors and people running actual decent businesses, because they enable effective matching between spare capital and the places where it can be effectively deployed. So I think it's great that most investors feel safe enough to invest in things. It makes the world better.

Think of it like the market for food. You can walk into pretty much any store in the US, buy pretty much any packaged food item, and safely eat it. Is it bad that you aren't applying your whole intellect to decide whether that muffin is safe? I'd say no, it's in fact good that you don't have to think about it. But that's only enabled by some pretty intense regulation on food.

Some would argue that it's interfering in the marketplace to keep people from selling shoddy discount food, and that we should just let the invisible hand work it out. That people "wailing" when they start throwing up is just them being crybabies, and that they should caveat emptor harder if they don't like blood in their stool.

But I think free market fundamentalists like that are deranged. I think markets exist to help fulfill human purposes, and that we should minimize the extent to which scammers, jerks, and monsters can parasitize them. And I think that for all the hue and cry about "innovation" in the cryptowhatever space, I've seen very little that's actually a significant socially positive improvement. In contrast, over the same period that Bitcoin has done approximately nothing useful, we've seen things from M-Pesa to Venmo actually serve millions and millions on a regular basis.

OP is missing “common enterprise” part of definition, which covers commodities. Security futures are securities (jointly managed by SEC and CFTC), commodity futures are not (as they are a derivative on a non-security). The main inconsistency is that bank loans are not securities.

> if it is marketed, bought, sold, and held as a money-making thing, it's a security

No, sorry, no such legal language exists and how absurd of a law would that be. Anything which goes up and down in value could be bought or sold as "a money making thing" including collectible video games, books, Pokemon cards, .com domain names, pork bellies, houses, bar codes, imported goods, rare sneakers, wholesale products, golf club memberships, Picasso paintings, etc.

There is a Supreme Court precedent called the Howey test which specifies 4 criteria for which all 4 must be true in order for something to be a security. You cannot have 3 of 4 and be considered to be a security:

1. An investment of money

2. In a common enterprise

3. With the expectation of profit

4. To be derived from the efforts of others

Notably, speculative flipping of owned assets is not considered to profit derived from a common enterprise. Speculative flipping happens everywhere in all supply chains you participate in on a daily basis. Everyone is attempting to buy low in an attempt to sell high. Everyone loves to compare crypto to the tulip mania in the Netherlands from the 17th century. While that is true in some cases, you certainly can't make the case that tulips should be regulated by the SEC.

That seems to reinforce the grandparents characterization of this as an evasion of the Howey test, not refute it. You really think the technical distinction of a unique number defeats the idea of "common enterprise"? Doesn't the fact that all the initial profit goes to one enterprise clearly make it "common"? Conversely, aren't traded shares of common stocks on NYSE merely "speculative flipping" unless they're specifically paying dividends?

Meh. I mean, fine, you can make that argument but I don't think this is nearly as clear as you think it is. From my perspective: I mean, duh. Of course these are securities. "Give us money for this thing and you'll get more money later" isn't a hard idea to understand as the spirit behind securities regulation.

> Doesn't the fact that all the initial profit goes to one enterprise clearly make it "common"?

Maybe, but you're not tied to the enterprise after the initial purchase.

> Conversely, aren't traded shares of common stocks on NYSE merely "speculative flipping" unless they're specifically paying dividends?

The value is tied to the company and can be extracted in a multitude of ways, and the company has a duty to the shareholders. The expectation of profit in a stock goes well beyond just dividends.

> I mean, duh. Of course these are securities. "Give us money for this thing and you'll get more money later"

That depends on where the money comes from.

The people selling gold say the exact same thing, and gold is not a security.

There absolutely are gold-based securities, though, and most of the "invest in gold" scams are likely subject to securities law. It's true that gold objects themselves haven't been traditionally considered securities, but that's not a blanket statement.

Which is to say, again, that it's complicated and there aren't any free hacks to evade regulation if you're trying to scam people with an obviously fraudulent security

Actually, Pokemon cards fit all four prongs of Howey as does Yu Gi Oh etc. SEC would have a slam dunk against these sales (to children, no less!) but they just chose never to pursue that.

1. They buy the cards

2. The Pokemon show and franchise

3. They keep them in MINT CONDITION and don’t open them

4. If the show fails to entice more kids in the future then everyone will forget about that special charazard card, so it all depends on the show and movies to keep the pokemon franchise kickin

So really, all the holier-than-thou types should realize how many of the counterexamples who never got sued are just SEC exercising their discretion

The purchase of the cards is not engaging in a common enterprise with the Pokemon show and the efforts of others aren't the cause of the rise in prices.

If not for the show, the cards wouldn’t be worth as much. The show is what is spreading the memes and driving the demand for show related merchandise. That IS the business model!

It sounds like your whole defense would hinge on hoping the SEC won’t be able to convince a court that it’s a common enterprise. I looked it up and “common enterprise” is not very well defined in either statutory law nor case law. I have been over this with many people and made them realize that you can’t possibly predict “this isn’t a common enterprise” defense would work in a court or law. SEC has argued many novel concepts, just this year with LBRY for instance. And they were successful. If they want to say it was a common enterprise, and the term is not even well defined, then they will make a strong case. It’s not up to you reading your own opinions into definitions, it’s whether a judge or jury makes a decision in a case, and / or whether the SEC exercises their restraint.

> The show is what is spreading the memes and driving the demand for show related merchandise. That IS the business model!

I'm actually not sure how true this is. Given that there are non-pokemon examples (like magic: the gathering) that don't have cross-branding, and there exists a competitive pokemon TCG scene independent of the show, and the cards maintain a secondary market value as long as people want to play kitchen-table or collect them as collectibles, which will be true independent of the success of the Pokemon company, the common enterprise thing falls apart.

I don't purchase pokemon cards as an investment in The Pokemon Company^tm with the expectation of profit. I purchase them as a toy to entertain me. That fails prong two and three.

That a secondary market exists, and that particular objects have a high secondary-market value doesn't make the whole thing a common enterprise for profit, and I really doubt the majority of pokemon card purchasers do so with the intent to profit, same with MTG. Most people want some cool cards and entertainment, and throw them away.

(And this is backed up by data: with MTG, which has astronomically higher demand and card prices than pokemon, their market research shows that, by far, their largest consumer segment is entirely casual players who never attend sanctioned events. They buy packs or precons. So concepts like the secondary market value are immaterial for the majority of the consumers)

Sorry but it's not about what you do. Even if it fails prong 2 and 3 for you, the SEC can still successfully argue that the vast majority of sales are securities.

This was the dangerous precedent set in their victory over LBRY in December 2022. They argued that if at least some people bought the utility tokens with expectation of profit, then the utility token sales were securities -- and the judge bought it!

LBRY's arguments sound like yours: LBRY argued in support of its motion for summary judgment that LBC coins are not securities because (1) they are consumptive in nature, with purchasers using LBC for on-chain activities rather than investment purposes; (2) the “primary focus” of LBRY’s promotional statements and materials was the utility of LBC, not its potential price appreciation; and (3) LBRY stated explicitly in marketing materials that LBC was intended for consumption on the LBRY network, not as an investment.

The court also rejected LBRY’s argument that the purchase of LBC for consumptive, and not speculative, use by some of its buyers suggests that LBC is not a security for any of its buyers. The court suggested that the intended use of the token by a subset of LBC purchasers was of limited relevance to the overall analysis, which ultimately indicated that LBC was a security under the Securities Act.10

But this is where judges come in, who can analyze things like real world intent. And stuff like "At launch, LBRY retained 400 million LBC for its own use" doesn't to me imply that these things are the same. TCGs do not function like securities. If I am a securities issuer, I make money primarily when the security goes up in value. If I am a TCG producer, I make money when people buy more of the product, irrespective of the value of it. The goal of a securities issuer is to, over time, inflate the value of the security. The goal of the TCG issuer is to reduce the value of the cards (on the secondary market) by producing more of them.

Konami stock goes the more blue-eyes white dragons are printed. That isn't true for LBRY, and that's what the "common enterprise" bit is about. Hasbro and Konami and the Pokemon company aren't keeping a stockpile of additional secret super valuable cards to go up in value over time, because they aren't securities and they don't act like securities, and the companies will just print more of them if they want to. But that isn't true for LBRY when they keep a hold of the asset they create and bet on its value increasing over time!

And of course this is why we have judges. They can look at the evidence and see that The vast majority of LBRY investors were investing with a profit expectation, LBRY was treating the token as an investment that people could use to profit from the platform's success, etc. The difference is that with LBRY, people treating it as a security was the norm, but with TCGs, treating it as a security is done only by exceptional investors, and the companies don't condone it, even tacitly[0]. And the actual filings in the case make that abundantly clear. You don't have the CEO of Hasbro or Konami or The Pokemon Company releasing press releases about the market value of cards.

Like in the past I'd seen some of these arguments and been somewhat convinced (especially around the whole secondary-market and tax issues), but this feels really cut and dry.

[0]: (except perhaps with MTG's reserved list, but that still fails due to condition 2 above, Hasbro/Wizards and the "investors" in the Reserved list cards have different interests. They aren't invested in a common enterprise. Wizards would love, I mean absolutely adore reprinting reserved list cards, and they try all the time in sneaky ways (silver or gold border, near-functional reprints, digital versions, etc.) because reprinting those is good for the company. What it is bad for is investors in the cards. Those are distinct incentives, not a common enterprise, not a security.

So it's clearly not horizontal, right, and your argument is that there is a vertical common enterprise?

I don't think it's all that poorly defined, but either way, for a vertical the 11th circuit required that you must "show that the investors are dependent upon the expertise or efforts of the investment promoter for their returns."

That's just not the case here. The show could end completely and "investors" (I don't think they are investors, either, but I'll go with you on this) continue to see returns.

You've also got issues of control over the cards and the fact that people purchase them without intending to profit from them, both of which strike against you.

Just because a show could hypothetically end and the assets would go up, may not be a convincing argument. Hypotheticals could go either way.

One company owns the IP, the rights to the characters, to produce shows, they have the expertise, and it is exactly the show and the brand that drives the demand for merchandise sales. This is well established. They advertise the merchandise.

Now, without the advertisement, there could remain a niche group of people who would pay a lot for collectibles, but nowhere near the amount of people or capital under their management than during the heyday of the show actually airing and constantly making the memes (pokemon, yu gi oh, whatever) relevant and driving demand.

By your argument, LBRY the company could fold and people would continue to use LBRY tokens. Which is exactly what happened. So does that mean it wasn’t securities sales after all?

As for the other issues you mentioned, the court explicitly stated that just because some people buy the cards for consumptive use doesn’t mean they all do. You could buy 100 tickets to a ball game, but intend to only take your family, and scalp the rest. One of the criteria for a securities sale is did you buy more than you could ever conceivably use? And if you keep the cards in mint condition unopened that’s pretty much textbook definition of investing into collectables. Then the only question us how much are you relying on the expertise of the company producing Yu Gi Oh content to… continue to produce Yu Gi Oh and keep it relevant.

Now, if Yu Gi Oh was in the public domain and lots of entities could keep the memes going, sure. It would be super decentralized (although a strict reading by the SEC could nevertheless see a “common enterprise” horizontally across all of them, much as they are considering now for Ethereum!)

But since all these initiatives (Teenage Mutant Ninja Turtles, the music and movie industries etc.) work off massively relying on copyright protections, so they are the ONLY ones authorized to use / license the characters, then yeah you’re kind of relying on the efforts of a third party promoter to make sure a lot of people give a crap about your mint condition charazard collectibles!

Do the following thought experiment … if some group were selling the same exact type of trading cards in the form of NFTs, and creating Telegram channels to promote them, creating all kinds of episodes featuring those characters, are they a “common enterprise”?

>By your argument, LBRY the company could fold and people would continue to use LBRY tokens. Which is exactly what happened. So does that mean it wasn’t securities sales after all?

No, my argument is that the performance of the show is not directly linked to the price of the cards, among other things. LBC did not have continuing returns after the announcement that they were folding, and the theoretical use of the coins outside of investing is gone with the company. There's also the fact that there is no contract or common enterprise between purchasers of the cards and the makers of the Pokemon television series.

LBRY had other functions that made the coins look more like securities. For example, they used LBC as security for debt, they promoted it as an investment opportunity, they acknowledged its growth aligned with their company and they encouraged people to hold on to the coins so that they would appreciate in value despite new issuances. The entirety of the value of the coin was based on the performance of the company.

> the court explicitly stated that just because some people buy the cards for consumptive use doesn’t mean they all do.

Sure. Most people buy the cards for consumptive use, though. It's not a small number. Some people do invest in them as collectibles, but that doesn't make them a security.

> if some group were selling the same exact type of trading cards in the form of NFTs, and creating Telegram channels to promote them, creating all kinds of episodes featuring those characters, are they a “common enterprise?"

Do you mean the group that made them, sold them and promoted them? Sure - if a group of people made some products, marketed and sold them together then they would likely be acting in common enterprise. It could be a partnership, especially if they pooled their sales. That's not really what is happening with Pokemon cards, though. I'm not arguing that The Pokemon Company or Nintendo can't issue securities, I'm just saying the products they make and sell for consumptive purposes are not in themselves securities.

> and the theoretical use of the coins outside of investing is gone with the company

Gone? Theoretical? LBRY has been and continues to be one of the most—used utility tokens out there. The tokens are used in a decentralized network to pay for streaming video. That’s the whole point — if the company has folded but the network continues then that proves there was a strong utility case.

I am saying that just because there is utility doesn’t mean many of the sales weren’t also securities transactions. And the same goes for Yu Gi Oh. It doesn’t matter if there is a direct link with the price of the cards. When Yu Gi Oh is off the air and no one is advertising the toys and cards, are you really going to tell me demand will be unaffected? Children grow out of the toys, and new children will be marketed toys by OTHER groups that rise up after Yu Gi Oh. To say their efforts, expertise, advertising etc have no link to the demand for toys is a very dubious argument, some might even consider it preposterous.

> if a group of people made some products, marketed and sold them together then they would likely be acting in common enterprise

That was the prong of the Howey test that we were discussing. You claimed that there was no common enterprise with Pokemon. Yet the company behind Pokemon did all those things you mentioned — and it is in fact the exclusive rights holder to the IP, so no decentralized ecosystem can even legally rise up to dilute this common enterprise. That is how ALL of these media + merchandising plays work.

Finally, using assets as security / collateral for debt doesn’t mean that the assets are investment contracts. I could use lots of commodities and other assets as collateral for debt. They could even be pegged to the dollar, and still be worth a dollar. USDT for instance could hardly be considered an investment contract, right?

>When Yu Gi Oh is off the air and no one is advertising the toys and cards, are you really going to tell me demand will be unaffected? Children grow out of the toys, and new children will be marketed toys by OTHER groups that rise up after Yu Gi Oh. To say their efforts, expertise, advertising etc have no link to the demand for toys is a very dubious argument, some might even consider it preposterous.

I am actually saying that, yes - the value doesn't come from the current show, it comes from nostalgia, rarity and the drive to collect things. I'd bet that most people with Pokemon card collections, for example, do not currently watch the cartoon series.

>Yet the company behind Pokemon did all those things you mentioned — and it is in fact the exclusive rights holder to the IP

Yes, Nintendo, the Pokemon Company and its shareholders are engaged in common enterprise. Purchasers of Pokemon cards are not.

>Finally, using assets as security / collateral for debt doesn’t mean that the assets are investment contracts.

I didn't say it did. It was part of the argument that the company believed the coins had appreciating value. What about the rest of it? "promoted it as an investment opportunity, they acknowledged its growth aligned with their company and they encouraged people to hold on to the coins so that they would appreciate in value despite new issuances." Does the Pokemon Company do that?

So now you are claiming that people’s nostalgia drives the sales today now that the shows are (temporarily) off the air. And therefore it is not a security. And also the original sales while the shows were running were never a securities transaction.

I am not sure I buy that argument about the original sales of securiries, and the SEC and judge in the court might not either. In fact, the LBRY and Ripple cases both have the judges saying secondary sales later on are not securities transactions in the crypto case also, but the issue is whether the original ones were.

Because the nostalgia is only widespread BECAUSE of the efforts of Pokemon to promote their IP, including getting the TV show syndicated, telling the kids to “gotta catch en all”, so now when the kids grew up, they have nostalgia. And also the cards (some of which were explicitly bought for investment purposes and their rarity, like the rare / limited edition charizard or the rare Yu Gi Oh Exodia combination etc) are in circulation through an “ICO” - an initial card offering and subsequent offerings haha. At the time they were conducted, the “investors” were totally relying on the efforts of the IP holders to promote the cards and make the rare ones worth something, or combinations or collections worth something. So at that time they might have been buying an investment contract. Again, I am simply applying the SEC’s currently MADE arguments in the LBRY and Ripple cases, to trading cards!

By analogy, if a crypto company today sells NFTs with different properties and emphasizes their use only in battle, yet also has rare special edition NFTs, promotes them online for years through Telegram channels and metaverse ganes etc. then you’re claiming the SEC cannot prove any of those rare NFTs were purchased relying on the efforts of the promoter to make the game’s network effect grow to such an extent that it would increase the demand for the rare NFTs, even after the promotion efforts ended. The form of whether it’s a trading card or crypto shouldn’t matter, only the facts and circumstances matter.

And if a new TMNT movie comes out then sure, you could again claim that all the action figures and cards being sold are for consumptive use only. But the LBRY case explicitly said that there could have been people buying it for INVESTMENT purposes and therefore it sets a scary precedent for the crypto industry, that, if applied to those industries would make Pokemon and Yu Gi Oh cards just as much securities sales for that same reason. But SEC didnt take them to court or make arguments like that, because it exercised its discretion to not bring suit. That’s what government agencies do. When Obama said he would direct ICE to deprioritize DACA cases, that’s what he was talking about. Or when police see a Police Benevolent Association card for a minor offense. The government selectively enforcing things is common.

> Does the Pokemon Company do that?

You mean the company that puts the phrase “gotta catch em all!” everywhere including its shows and jingles? It certainly encourages “collecting them all”. This is what happens when you do:

> LBRY had other functions that made the coins look more like securities. For example, they used LBC as security for debt

======= DIFFERENT QUESTIONS

Just out of curiosity, if you still think the original sales are not securities, would you also be just as optimistic with regard to allowing the people to play games and do battles on a smart contract to win actual ETH? Would this violate the FTC’s restrictions on lotteries? Would you say it is a lottery because there is an element of chance when you get a random card? Or a game of skill because a karebo used properly can defeat a blue eyes white dragon? And is a company putting up prize money on the blockchain enough to satisfy the bonding requirements if it is a contest / game of skill instead of a game of chance?

And how about deploying a smart contract allowing people to wager ETH and then have it go to one or more winners based on some on-chain battles or rules which are primarily based on skill? (Nevermind that an AI could trivially try all the combinations to give an unfair advantage).

Yeah, well the SEC also has rules from the 1930's stating that brokers who sell shares to clients and fail to deliver them should have their license suspended.

Guess how often that rule was applied since the 30's?

Zero. And that's not because fails to deliver don't exist.

So yeah, there's a massive regulatory crisis going on and SEC rules are applied however the future employers of the SEC decisionmakers want.

Care to offer some evidence of that? I haven't heard that and I am in the vertical. I agree that Impact Theory was selling securities, and I think it's pretty clear. But bored apes a security? I don't think many share that opinion. How is it any different than art or pokemon cards? People buy both all the time with the expectation they go up in price.

If the buyer's expectation of profit from the common enterprise pushes something closer to being a security, wouldn't that kind of money extraction move it further from being a security?

Its great to see commissioner Mark T Uyeda also dissenting, because for some time it was only Hester Pierce that would take these views on digital assets, and for her views to be elevated to head commissioner it requires a Republican President to make that nomination, as she is Republican.

There are many people that are not Republican that would aim to get her appointed and do whatever it takes. Which means casting a vote for a Republican Presidential candidate no matter who that is, simply because the power is imbued within that person.

Mark T Uyeda's existence as a Democrat makes this a lot simpler, for people that would find the above to be awkward, as Democrat leadership could also nominate him for head commissioner.

Bipartisan dissent is great.

It really isn't enough to just not like digital assets or the industry, to establish jurisdiction over them for enforcement.

Oh no people lost money.... because they couldn't resale a consumer product?

> We do not routinely bring enforcement actions against people that sell watches, paintings, or collectibles along with vague promises to build the brand and thus increase the resale value of those tangible items.

exactly, its either go after all of them until Congress rescinds the agency's charter completely with this outstanding application of Howey, or show the exact distinction that crypto asset creators can follow to act solely as a consumer product.

You’re right, I agree, I’m more so glad that they are willing to use this as a place to point out other unanswered questions and incongruencies in SEC actions

I agree that the dissenters bring up a lot of good questions that need answering.

However, if you believe their fundamental argument that NFTs aren't really securities... what regulatory body should prevent this kind of behavior? Or should rug-pulls effectively be legal, and buyer beware?

I don't think NFTs as a whole are breaking any FTC related laws. However, the way that they are marketed or sold could break some laws if the communications are deceptive. For example, a rug pull might be considered illegal under US Law Title 16, Chapter 1, Subchapter B, Part 238.4 "Switch after Sale":

crypto consumers should be far more discerning than they are

even the term “rug-pull” is not discerning enough, it refers to a dozen distinct behaviors, of which a few would still be illegal while the other many behaviors are just a misalignment of expectations

removing liquidity? thats not illegal under either consumer or securities framework and most commonly called a “rug pull”. communities can provide their own liquidity as a feature of the crypto space, and in no space do purchasers have an expectation for liquidity

ceasing to continue making press releases or taking down a website and community channels? also not illegal under the consumer or securities framework.

taking other people’s provided liquidity out of a staking contract without saying thats whats going to happen would be illegal under both frameworks. that kind of rug pull is theft.

collecting funds and promising to do X and then not even attempting it, thats prosecutable under both the consumer and securities frameworks, in more ways under a securities framework

Let's start by looking at what typical tokens are.

A fungible token is simply a store of the following records:

(public key, amount)

There is a stored procedure that lets anyone with the private key to lower the "amount" value on their row and increase the "amount" value on another row by the same amount. There's no tracking of which part of the amount came from where, the "tokens" are fungible.

Now let's look at what a non-fungible token is.

It's a store of the following records:

(public key, id)

Whoever has the private key can change the public key field in the record.

That's... it.

You can add a table that has

(id, metadata, url), that's common and what you see with most shown NFTs. There's some helper functions but really that's the essence of it.

None of that necessitates it being sold as an investment in a common enterprise any more than selling bits of paper with a number and a signature on them does. Signed prints by an artist aren't securities, your place in the line in a queue isn't a security, a concert ticket isn't a security.

You can obviously however treat the above data structure as representing some kind of security. This is true with fungible tokens too, a list of shareholders is essentially the same structure. So it comes down to how it's sold.

Not all ownership denotes a security. If you own (and own can often be interpreted simply around having control over) a thing, you can sell it without that necessarily being a security. That's why the test is not "can it be sold".

If I sell you a hand drawn stick figure for $100, and you buy it because it's "art", then there's no rug to pull. You bought it, and it doesn't matter to the artist whether the resale value goes up or down. If it goes down, it's still not fraud.

But if I sell you a hand drawn stick figure for $100, and you buy it with the mutual expectation that it will eventually be worth more because of the value of the brand/project, and the effort I put in to grow that value... isn't that a security, by definition?

>But if I sell you a hand drawn stick figure for $100, and you buy it with the mutual expectation that it will eventually be worth more because of the value of the brand/project, and the effort I put in to grow that value... isn't that a security, by definition?

This seems equivalent to buying a baseball card of a specific player with the expectation that the player will put in effort into the game and thus increase the value of the card. People buy cards of specific players on the assumption that they can buy in cheap and sell when the value of the player's brand increases.

The player does not issue the card. The player does not profit from any "appreciation" of the cards. The amount of player cards sold is nowhere near that of NFTs so the potential damage is limited and the history of player cards has always been for "collector" value and not a real investment. The history of NFTs has been since day one for Investment.

> The history of NFTs has been since day one for Investment.

I'd argue that there was a brief moment -- right at the start, when NFTs were a novelty and most of the ones being minted were one-offs which purportedly represented unique things created independently from the NFT, like a YouTube video or a tweet or a piece of art -- where one could conceivably argue that NFTs could be collector's items and not investments.

The moment that groups like Larva Labs started minting runs of thousands of NFTs with images stamped out from a template, though, that argument became much harder to support. Nowadays, it's thoroughly dead.

perhaps the player isn’t the important bit really. It’s the card manufacturer in fact. If I print a Nolan Ryan card no one cares. If a name brand does, and also promises to grow their brand and that will make it more valuable, maybe that is more closely related?

By that definition, anything purchased with the intent of reselling for a higher price in more favorable market conditions would be a security -- real estate, product inventory in a warehouse, etc.

its either go after all collections with this outstanding low hanging and untenable application of Howey, or show the exact distinction that asset creators can follow to act solely as a consumer product like the fine artists and watch collections

it is also accurate that if following a consumer protection framework, most activities and behaviors would not be fraud.

so for a creator or secondary market operator or promoter, not knowing which branch of theory to follow makes all of their behavior bifurcated and prosecutable under one framework, a securities framework, but not a consumer protection framework. and vice versa.

The partisan assignments are explicitly partisan, but independents can be appointed too. There is a limit to how many commissioners can be from a single party.

There seem to be a lot of people out there with paper cryptocurrency gains who are happy to use them for absolutely anything that will make more money.

This is how the free market works, however. You can sell yourself a pencil for 1mil and it will be technically valued at 1mil in the public market, but good luck selling that to someone else. Same applies to NFTs, just a bit more marketing (edit: and dumb hype i should add) is involved.

No, because your $1 million pencil was never on the market; your hypothetical self-sale was a fake transaction. With NFTs it was often deceptively represented that someone paid $1 million, disguising the fact that these were bogus self-sales.

I really enjoy a lot of Tom Bilyeu's content, but I've noticed he seems to lack a filter for great ideas from charlatans. And in some regards fair enough, it can be hard, but he's also building a brand and company around some folks who seem to be exaggerating their claims. For example Raoul Pal.

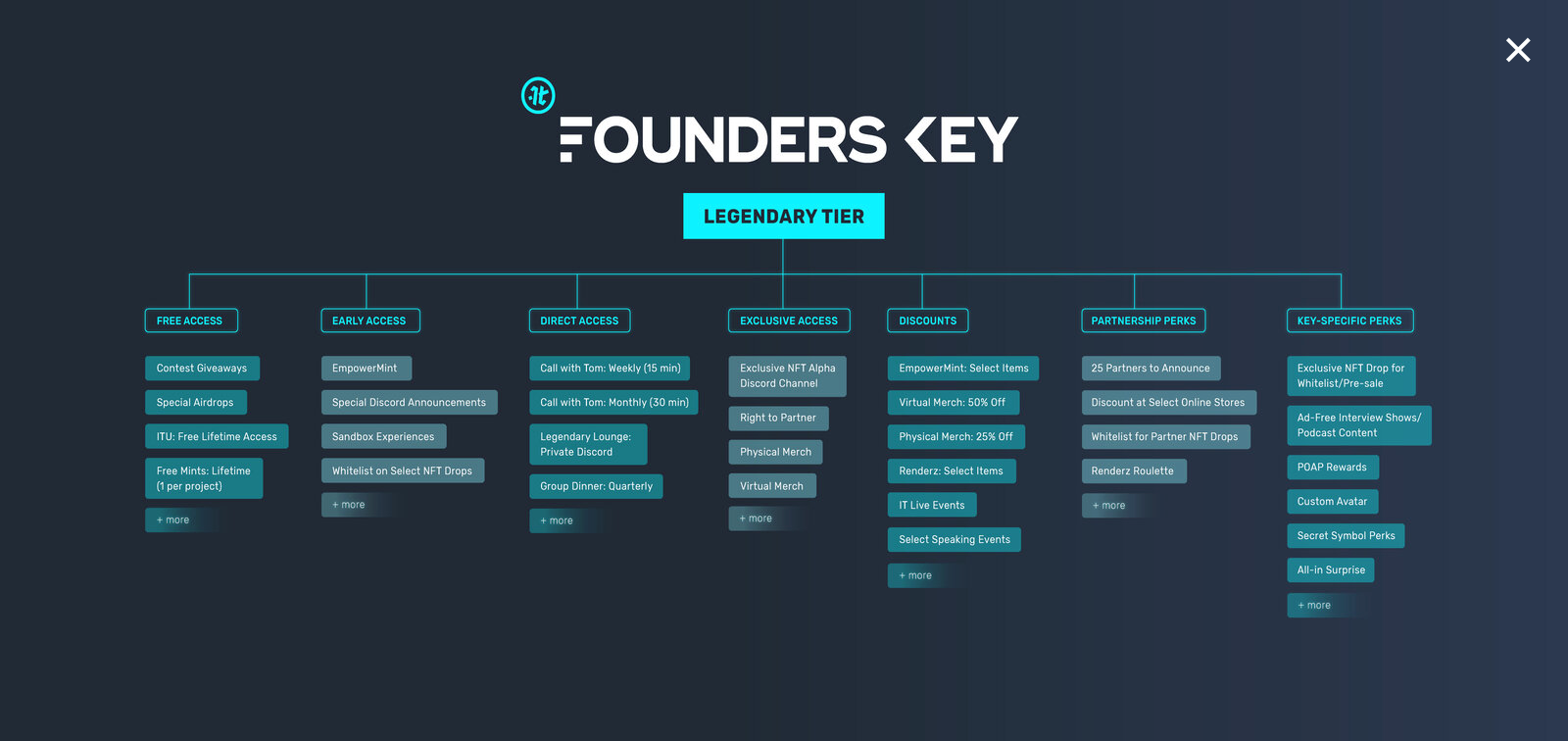

This seems reasonable. From what I am able to pick up, they thought they had found some clever loophole to ICO by selling NFTs. Despite the C&D some of their founders key benefits are still up: https://founderskey.io/images/fk/legendary-key.png

Basically 1. until the platform is implemented the key is basically an IOU. However, it can be sold and transferred for a profit AIUI so it’s not like a crowdfunded game where you get some similar benefits as those can’t be sold for a profit. 2. all your NFT corresponds to is a literal key representing the benefits Impact Theory will make available to you in the future so per the Howey Test you are purchasing a contract (not a specific piece of art or cosmetic) yielding profits from the sole efforts of a third party (Impact Theory).

Honestly, they probably could have gotten away with it if they had been a little less lazy! I bet if they tried to raise money by selling some kind of character art (that currently exists like a normal NFT, not a custom avatar they’ll give you one day) that they’d eventually also display in their final product they’d have been fine.

The interesting takeaway though is that it seems like you can’t do kickstarter-style crowdfunding through transferable NFT ICOs, at least in this form in which you got nothing but a key.

I hate to dunk on this type of art while it's down but

> Impact Theory agreed to destroy all Founder’s Keys in its possession or control

What does this mean practically -- like they delete the files that would allow them to transfer control of the NFT? What even are these things, are they just text files in a distributed file system that list the owner's name or what?

They would most likely "burn" them which means giving control, transferring ownership, of those NFTs to a wallet address that no one controls which means they are out of circulation.

I assume they see using a standard NFT contract which doesn't have any way of taking control of those NFTs once ownership is to that burner address. It would be impossible.

The concept of NFTs stored on a distributed ledger makes sense to me especially for the shitty games that sell skins.

The idea they have some sort of value and can be considered a security, doesn't really. It is no different than the current in-game marketplaces that sell/resell skins from whatever game has skins this week.

At what point does a thing you buy or sell become a security? Are baseball cards a security? Should my local baseball card shop be closed down as an unregistered securities broker?

I don't own crypto or NFTs, so maybe I'm just not informed enough?

From what I'm reading here, the company misled "investors" by attaching the NFT to ownership in the company, which would be considered a security.

"The order finds that Impact Theory encouraged potential investors to view the purchase of a Founder’s Key as an investment into the business, stating that investors would profit from their purchases if Impact Theory was successful in its efforts."

When I purchase a baseball card, I do not have the expectation that there is any additional value attached to the baseball card beyond what the collector's market will pay.

The NFTs did purport to give ownership rights in the business profits of the NFT, as represented by the value of the NFT increasing specifically because of the labor of others acting to increase the value of the NFT.

And that is part of what makes them completely different from baseball cards. Even if the value of the cards are dependent on the labors of others, with the baseball cards, the laborers (i.e., players) are not performing that labor with the intent of increasing the value of the cards; the value of the increase in the cards, if any, is wholly coincidental.

With baseball cards, You have an expectation that the MLB will continue to promote and develop Baseball as a top sport. You purchased an illegal security.

With baseball cards, You have an expectation that the MLB will continue to promote and develop Baseball as a top sport. You purchased an illegal security.

No, you don't. For starters, baseball cards are not sold or marketed by the MLB, the teams, or the players, and buying a card does not entail any ownership in either the MLB, the companies making the card, the store where you bought the card, the players, or the teams. They're not sold by the companies that make them as business opportunities, and in fact most cards aren't worth anything.

But every NFT tells you that you should buy their NFT because their efforts to promote the NFT as a business will lead to it increasing in value. And legally, that makes all the difference.

Rare things are not automatically valuable. I still have "dragon dice" and an original deck of cards from an old lord of the rings game. Basically worthless.

This only would be the case if people continued to care about baseball. In reality, fewer people would care less and less over time. For example, there is not great value in jousting paraphenelia.

Its also worth nothing that the SEC is losing in court, losing the support of Congress and losing the support of the White House

specifically as more people, including judges, notice this lack of distinction and the SEC’s unwillingness (and inability) to describe why there is a distinction

there is either a way to issue crypto collections and collect money for them without being a security, or all other collections sold are securities with unregistered broker dealers operating illegally and fraudulently for the past 100 years

That's not true, just wishful thinking on your part.

Not all collectibles are unregistered offerings, obviously. Being a collectible also doesn't mean it can't be an unregistered offering also. This one clearly was.

You seem to be very keen on making this rather dubious point all over this thread. Certainly more motivated than I would consider “normal” for someone just wishing to weigh in on a topic they care about. Are you connected with this, or just having a particularly manic day?

One key difference between MTG cards (or baseball cards, or most any traditional collectible item) and NFTs: If the SEC shut down Wizards of the Coast and/or caused them to radically alter their businesses, old Magic cards would likely rise in value as a result, rather than cease having any material value whatsoever, as is the case with most digital assets.

Baseball cards aren’t owned by the MLB. That would be a weird expectation like buying Oakland raiders hat and expecting the hat manufacture to stop the raiders from moving to Las Vegas because it would devalue the apparel.

People buy baseball cards to collect them. I have a bunch from my childhood. They weren’t investments.

That seems materially different from an expectation that you will make money on the card, or that the value of your card is determined by MLB's profitability and future earnings.

That's still not a security, because if someone buys all the baseball cards, they don't control anything about MLB or have a right to its profits, for example.

There are companies that use the cards of specific players as a way of investing in that player - they better the player does, the more their cards are worth.

> When I purchase a baseball card, I do not have the expectation that there is any additional value attached to the baseball card beyond what the collector's market will pay.

What about music royalties rights? Those are almost always purchased with expectation of profit. Those are even explicitly marketed on the basis of how big an artist is going to be. Yet the SEC does not consider them securities

> At what point does a thing you buy or sell become a security? Are baseball cards a security? Should my local baseball card shop be closed down as an unregistered securities broker?

The SEC's legal theory is specific to this case, and does not seem to apply generally to all NFTs. Here's the SEC's explanation:

> According to the SEC’s order, from October to December 2021, Impact Theory offered and sold three tiers of NFTs, known as Founder’s Keys, which Impact Theory called “Legendary,” “Heroic,” and “Relentless.” The order finds that Impact Theory encouraged potential investors to view the purchase of a Founder’s Key as an investment into the business, stating that investors would profit from their purchases if Impact Theory was successful in its efforts. Among other things, Impact Theory emphasized that it was “trying to build the next Disney,” and, if successful, it would deliver “tremendous value” to Founder’s Key purchasers. The order finds that the NFTs offered and sold to investors were investment contracts and therefore securities. Accordingly, Impact Theory violated the federal securities laws by offering and selling these crypto asset securities to the public in an unregistered offering that was not otherwise exempt from registration.

This comes back to the core problem of crypto though - I agree that transferring skins would be cool or whatever, but distributed consensus does almost nothing to accomplish that.

A game developer already has to opt-in to the NFT system and then maintain indefinite support for the NFT system, so if you trust them to do that why don’t you also trust them to maintain the ownership ledger?

I guess there are a few concerns here. What if the game developer goes out of business, or dies, or accidentally drops their db? What happens if they decide they don't like one of their collectors and want to wipe their balance clean? (Of course, you could do this with NFTs as well, but you'd have to write it into the contract ahead of time).

On top of that, the developer would need to build and operate their own infrastructure for trading with the tokens. If they were NFTs, then they just slot into existing applications without any extra work.

You can address all of those issues regarding continuity equally as well with actual legal contracts as you can with crypto 'smart' contracts (and you need the legal contracts in either case).

There’s a lot of reasons this mechanism would be interesting for a game developer besides trust. e.g. mitigating payment processor fees.

But to your question of trust, one interesting application would be in distributed & decentralized games intended to be released to the commons, see Dark Forest or Lattice.xyz. For these OSS projects, even if the original game devs decided to stop development, the community could permissionlessly continue to build atop the game’s immutable contracts.

It’s a completely made up problem for which crypto is supposedly the solution

- We’ve known for 2 decades how to do skin or items exchange between games. It involves relational databases. Valve does it for their games or at least could do it at will. There’s not one unsolved technical problem here

- There is zero incentive for developers, publishers and licensors (you know the people that make up the game industry) to adopt any of it. My company dies, the licenses terminate and your items are toast. Technology does not at all change any of it because it’s not a technology problem. It’s a licensing problem. And if I paid for the license, by god no other developer else should get that value for free.

- Developers don’t want other developers to affect their own games, affecting visual design, polygon budgets, performance, power or any other aspect of the game. No benefit, only drawbacks.

- No, we don’t want you to bring your lightsaber or mickey mouse costume (you know assets that people actually find valuable) int our game because that’s a straight visit from the lawyers at the house of mouse and probably makes our carefully crafted game look like ass.

- No middleman is only a problem if you need a middleman or the middleman fails to deliver value. Not if you can be the middleman. People attempt to muddle this down to a payments processor issue, but the last decade has shown crypto is just plain shit at that, from gas fees to security, lack of customer protection and any other dimension. And if it’s not payment, well, we could just as well use a database to share games between developers at the same publisher or valve.

- People bring up demand for external markets like Diablo’s Auction house. But these demand economies are fractions of the overall game value systems and increasing the focus on the fraction very quickly erodes and destroys the main game.

- IP licensors don’t benefit if people carry their IP from game to game unless game and game pay the fee

- Publishers don’t want to give telemetry or data associated with the movement of players to others. Sorry, that’s just not a good idea. And they want to sell you items again, not you hoarding older items.

Even gamers … don’t want it. They understand that this is mostly crypto bro driven attempts of turning every game into a gacha / real world money affects escapism fantasy for people with less money when every rich brat is parading their instagram assets through town.

The only people who think this is a great idea (including Boz) are in silicon valley with a long history of failing to understand games.

I'm not even a crypto bro, but it's honestly more exhausting to listen to someone go on about how private backends with user facing storefronts and relational databases solve the same problems as blockchain, than it is to listen to a crypto bro explain why we can't trust companies to manage records in their own relational database.

Just wanted to point out that one of these things necessarily follows the other, and billions have been wasted by people who listened to the cryptocurrency advocates, but failed to heed the warnings offered within those hyper-verbose responses.

There’s a well-established effect, common enough at this point to where some academic has probably given it a name like “The Twitter Dilemma” or something, that describes how a lie can be much more potent and contagious with exponentially fewer words than are necessary to effectively refute it.

You should feel free to ignore the extended retorts if you find them tiresome, but the modern reality is that you will be more likely to fall victim to a huckster’s scheme as a result. In the immortal words of Matt Damon, “Fortune favors the incurious, who like them apples.”

>There’s a well-established effect, common enough at this point to where some academic has probably given it a name like “The Twitter Dilemma” or something, that describes how a lie can be much more potent and contagious with exponentially fewer words than are necessary to effectively refute it.

Amen. The anti-crypto crowd in 2023 are now the more belligerent of the two (since the crypto crowd have largely gone quiet.)

You can ideologically disagree with it's use a money and I could understand that, but decentralized databases could be used nicely to circumvent the steam store 5% marketplace fees. That's value removed consumers wallet and sent to Bellevue at 99.9999% profit.

It's not a technical problem at this point with the low fee + fast transactions + negative carbon DeDBs out there. It's an incentive problem - no game studio wants to give up their cash cow, and consumers are, rightfully, wary of web3. IMO, it's going to be a long climb back for what we now call 'blockchain', but in 5 or 10 years I believe there will be advocacy for SOME data to be (including digital collectibles) free and open. Ironically, I think AI will speed this up as the major platforms throw up higher and higher walls to keep AI out -- people will realize the only options for control of their public facing works is to self host or use some form of decentralized database. That or we all start using github for social media.

That’s exactly what I am saying. It’s not a technical problem, it’s an incentive problem and the entire industry has no incentive to adopt a the technical solution these people are parroting to investors.

Why do I even bother to reiterate the rest of the paragraph that you did not quote? Game developers and their users are regularly exploited by App Store and payment processor fees. Transfers of ERC721 and ERC20 on an L2 is negligible by comparison:

Google recently changed tack on NFTs, allowing them in the Google Play stores, which means it is now allowed by their policy to circumvent the store fees for this use case.

But the more obvious solution here is to not use the walled garden app stores at all, if you plan to monetize and distribute assets via crypto. Thankfully we do have the web and PWAs.

It depends on exactly how the system is decentralized, but let's imagine that the tokens contain sufficient information to generate the e.g. skins. And now imagine some company decides to stop supporting this group of tokens, or perhaps goes bankrupt. In a centralized system that's the end, but in a decentralized one another company is now free to take advantage of that gap in the market and offer to support those tokens.

There's some pretty neat possibilities here, but they'll take a while to emerge. Not only is there no immediate profit motive (for a company on the complete up and up) but there's an active anti-profit motive since you're voluntarily ceasing otherwise profitable/powerful control for ideological gains.

> In a centralized system that's the end, but in a decentralized one another company is now free to take advantage of that gap in the market and offer to support those tokens.

You’re saying the new company makes a new game to support the skins?

Other than “making those skins be worth money,” why do we need to spend so much effort on proof of ownership then? Couldn’t the new developer just make those skins available for free and improve everyone’s lives?

People like to own things. It's the entire point of tokens. They enable one (in the optimal scenario, which exists for some but not all tokens) to own digital things in the same way you might own a hammer. You can transfer it, sell it, use it as your company logo or whatever else you want. And all of those rights are transferred alongside the token.

In this case a new company could support those tokens, but not without the owner's permission. So they could not make the skins available for free, even if they wanted to. It's kind of akin to how when you post on this site, what you post is actually legally copyrighted by you. The reason HN is able to publish it is because in the terms you agreed to, there is a clause where you license your text to them for display, and much more. But you could sue HNClone.com for copyright infringement if they chose to publish your text, without your (or YCombinator's - due to the extremely permissive license we grant them) permission.

The test for “is it a security” revolves around the idea of investing in a common enterprise with the expectation of returns. Sellers of TF2 skins or Football cards at no point advertise that they are an investment and that buyers should expect returns

> At what point does a thing you buy or sell become a security? Are baseball cards a security?

I don’t know about baseball cards, but the way Wizards of the Coast handles their policy around rare Magic: the Gathering cards makes me think their lawyers are definitely concerned about this kind of stuff.

WotC's steadfast refusal to publicly acknowledge the secondary resale market in any way gets comical at times, but they are a good example of how you should behave if you suspect you might have accidentally created a security.

In the case of Magic the Gathering in the 90's (the early days of MTG), Wizards of the Coast released a print run of cards the "Chronicles" set which contained reprints of cards from the earliest days of the game.

This caused a large controversy because the chronicles print run was massively larger than earlier print runs and suddenly there was an influx of cards in circulation where previously due to the limited print runs of the early sets these cards were exceptionally rare. This tanked the value of the secondary card market.

Due to the bad PR and negative attention this caused at the time WotC ended up publishing "The Reserved list" a list containing around 550 cards which they guarantee will never be reprinted.

This means for an iconic MTG card like "Black Lotus" there is a limited number of these cards in circulation and no new Black Lotuses will ever be printed.

The reserved list somewhat mollified the people that were baying for Wotc's blood at the time but now 30 years later it is more or less regarded as a mistake. There are a lot of armchair lawyers etc speculating on if they could ever renege on the reserve list and if it even represents an enforceable contract. WotC have basically refused to comment (possibly lawyers have told them not too).

I am not a financial person. This is speculation on my part. Please correct me where applicable.

It seems to me the operative difference between crypto assets and other collectibles is the market-making aspects and the original promises. Full-stop, the vast majority of NFTs and crypto assets are being hyped as investments. This covers the original promise. The market-making aspect is in how these collectibles accrue value. Most collectibles rely on a secondary market, whereas crypto assets don't seem to have an appreciable difference in secondary vs primary markets. This means the same asset is meant to accrue value in the venue it is originally purchased, among the same conceptual group of purchasers. I also wouldn't be surprised to find out that the utter uselessness of most crypto assets plays into their status as securities (or not).

> The concept of NFTs stored on a distributed ledger makes sense to me especially for the shitty games that sell skins.

NFTs are/will be really useful to account for transactions involving unique assets or bundles of rights associated with unique assets. They're perfectly suited for things like writing digital deeds to real property, transferring ownership of IP, validating chains of provenance for various items, etc.

The problem is that the current use cases are all spurious. NFTs used for "artwork" are neither transferring ownership of a unique fixed form of media nor used to convey any IP rights associated with the artwork. In these use cases, the NFT itself is non-fungible, but it encodes a reference to an external item that is both fungible and intangible, which makes it little more than a novelty.

That's exactly what we've been trying to build at Ultra.io

The push back from gamers has been non-stop and intense. I don't get it. They are willing to buy digital assets which can't be resold on an open market. They are not willing to buy digital assets that can.

Because there's no guarantee that those assets will be respected.

At any point the game maker can say "V1 assets aren't supported in V2". Or they can flood the market with "rare" items. Or they'll buy an item which was "stolen" and have it unilaterally revoked. Or... the list goes on.

There's also zero possibility of cross-game use. If ID releases the BFG9000 for free, is Skyrim going to let you shoot that at dragons?

But, here's the thing, don't listen to me. Listen to your (potential) customers. If they're all telling you that they don't want to buy what you're selling then take that as a sign.

Just to expand on your last point, I read their ad copy and once you strip out all of the meaningless filler text you have this key quote: “with the permission of the developer”. If they weren’t going to do it before, this can’t force them and if they were, they don’t need it.

As a game buyer, that sounds like doubling the number of companies who need to be paid and whose business decisions or failure will break things, add additional fees, etc. “Our incredible journey” is another way to say “you’re going to get server errors if you try to use your purchases”.

As a game developer, that sounds like I still have to do almost all of the work but now I’m locking in payments and giving up some control of my business to another party whose interests only partially correlate with mine or my partner developers’.

In both cases, there doesn’t seem to be enough value to support a sustainable business. Any two game developers are going to need to collaborate to share anything between games, and there’s a really upper bound on how much money they’ll pay before cutting out the middleman starts to look really compelling. Similarly, many gamers don’t like pay to win and won’t pay anything for cosmetic items so you’re chasing the percentage of people who both do and are willing to pay more upfront and more later despite not even knowing what future games would offer that option or how much they’ll charge.

There is push back because it's not a viable business plan and will never work with the most popular games. Games are controlled by publishers. They want to completely own the market for skins and other virtual assets. Why would they ever share their revenue with you guys? What's in it for them?

If you want to succeed with this scheme then ultimately you need to produce your own games. And those will have to be games that people actually enjoy playing, not just grinding for worthless coins.

> They want to completely own the market for skins and other virtual assets. Why would they ever share their revenue with you guys?

Or, even worse: why would a game publisher share some of the revenue for in-game purchases with customers who have lost interest in the game and are selling off their items?

Or, even worse: why would a game publisher share some of the revenue for in-game purchases with customers who have no interest in the game and are simply trying to profit off the customers who do?

Gamers spend millions on registering assets in marketplaces: game skins, mods, extensions, assets, it is all just buying records of ownership, but in a centralized company-owned database rather than distributed ledger.

People do not want to think of the things they buy as sellable assets. It’s just a shirt. Just let me buy it. I give zero fucks about your choice of backend data storage.

I see—you are saying gamers don’t really care about whether an asset is sellable; but the same is true of most things we purchase. When we buy a book or a vinyl record, we don’t think about its market value, until the day we stop needing/wanting it and realize selling could provide us some return. In those moments, it’s nice that there is no company that can block you from selling on the open market. Many gamers would appreciate this (and do, when they are given the ability to refund digital purchases they no longer want/use).

Most gamers aren’t whales. Most gamers don’t want NFTs polluting an already stagnating games industry as they recognize those psychological levers preyed on through MTX mechanics are just wrong and at their worst reflect the worst aspects of the gambling industry.