Burry is wrong far, far more than he's right (this is the guy who held a short position on TSLA through the entire rally), but he gets a lot of credit because of his big trade back in 2008 and the movie that was subsequently created about him. Also, as a crash approaches the final capitulation wave, you will see more and more people saying things like this. It's necessary, because the final capitulation of a crash requires people to believe that the system is permanently broken. This is the type of thinking that led to traders on Wall Street throwing themselves out of windows during the 2008 crash. If you want to take advantage of a crash, you have to have the clarity to understand that the masses are going through a bout of mass panic. If you join the crowd, you'll be too scared to do what you have to when everyone is selling.

All of this said, these things do take time. This kind of rhetoric will slowly spread until it reaches a fever pitch, likely sometime in the second half of 2023.

If you’re so confident, why don’t you short the stock? And if you don’t dare to short, then what value does your confidence have?

I’m sure that Burry, too, still thinks he is right and the market is just being irrational longer than he can stay solvent. But that doesn’t change the outcome, which is that his bet went terribly wrong for him.

Well, I mean there is always the good old: “The market can stay irrational longer than you can stay solvent.”

But there definitely is something strange with Tesla valuation. It’s above their 5 biggest competitors combined. Plus their multiples are way off compared to the other players in their market. It doesn’t look particularly sustainable to me.

I understand that people have different opinions about Tesla. That’s not only fine, that’s also important. I just find it really weird when people have been saying the same things since 2016 (frankly, for much longer), proven wrong time and time again, about demand, production and stock price, among other things, and still do not concede even the possibility that there just might be something that they have been overlooking.

> still do not concede even the possibility that there just might be something that they have been overlooking.

I will bite. What do you think make Tesla special compared to their competitors?

They clearly had a first mover advantage on EV which served them well but now that all manufacturers have good electric cars on offer what justify Tesla valuation?

This argument has been made back in 2016 and before. Many people who looked beyond those two metrics back then have become millionaires. You can say, of course, that these people just got lucky. Just as you can say that Burry was just unlucky that the market remained irrational for so long.

To me, when something consistently does not behave in the way that I predict that it should, then that’s a strong indicator to me that I must be overlooking something. There’s a fine line between saying that, in the short run, the market is just a voting machine rather than a weighing machine (which is true), and arrogance (which will cost you dearly in investing).

Well, what good is debating me? If you‘re confident in your prediction, find a way to profit from it. If you can‘t profit from it (say, because you cannot predict the timing), move on to another place where you can. Otherwise, what good is all that learning and thinking that you‘ve done on this topic?

(Unless, of course, you‘re in it for the sympathy of those who share your viewpoint. Then publicly debating makes a lot of sense. Although then you‘d be following the same mimetic impulse that you rightfully criticize in those who buy stocks based on memes and fashions, wouldn‘t you?)

My feeling was that you already had your conclusion. I.e. that Tesla has not technological advantage, and that the stock's 20x really is just a function of it being a meme stock, fueled by Millenials with FOMO.

I really do not know how much research you have done on Tesla, or whether you are actually participating in the market.

Also, I think you might have an allergic reaction to what one might call the Tesla fanboy crowd, which I can very much understand.

The thing is, dealing with an opposing viewpoint is a computationally expensive operation. One will only do it if one has a really, really strong incentive to be "less wrong" about this particular topic. Otherwise, in areas in which one has no real skin in the game, it really is just easier to stick to one's guns and treat the discussion as as a form of entertainment.

And even when there is an actual incentive to learn, doing such discussions in a public forum is even harder, because there's an audience. On HN, you also have the "paper trail". Nobody likes to see themselves of having been wrong about something. Much less about something that could have made them literally millions. It's already painful if one comes to such a conclusion by oneself. But having it rubbed in your face by someone else - how can that not trigger hostility?

Also, discussing the past has little value, because there's nothing you can change about what has already happened. The only value that there is in discussing the past is if one uses the past to tune one's mental model in a way that, when the next opportunity arises in the future, one's chances of success will be higher.

That, and not Tesla per se, is actually what made me react to this post. People standing there explaining away their failure (literally "apologizing" = "talking something away") - be it about Tesla, be it about women - that just seems so out of the Hacker culture to me. I mean, if my Python program throws an error, I don't argue with the interpreter. Instead, I look for my mistake and find a way to fix it. In fact, I don't even bother to feel bad about having made the mistake in the first place. I just keep on being focused on the goal I want to achieve, and will find whatever workaround or mental shift will give me what I want.

This post is already long enough. You may feel that I'm just pontificating and evading the question. But I think before any data can be exchanged, one needs a proper "handshake" to ensure that one agrees on the premises that make any form of exchange possible in the first place.

I really do not want to go through a list of arguments about the value of Tesla as a company here. These cannot be discussed in bullet form, because it will just lead to endless recursion. I would either bore you to death by being too verbose, or I'd be inviting ridicule by sounding naive. (If anyone is genuinely interested, feel free to email me. There recently was a post here about the benefits of talking to strangers, and I'm very happy to use this topic as a vehicle to talk to people I wouldn't meet otherwise.)

But I will give you one higher level argument that people might be seeing about Tesla that those who focus on P/E are missing:

People are insecure about the future. Few people know whether, ten years from now, their job will still exist. In a such a world of insecurity about the future, people tend to flock to those who seemingly can not only see the future, but actually create it.

What Tesla has done is that they have demonstrated to the world that an electric car can not only be sexy, but be better than a gasoline car in pretty much every respect (noise, user-facing emissions, safety, acceleration, traction, etc.). You just have to watch the GM Superbowl ad to see that other carmakers are basically reacting to Tesla, and trying to catch up.

I am not saying that Tesla is going to succeed because they were first. But I am saying that Tesla has done something that is the very prototype of capitalism. They went Zero To One. Instead of competing on faster horses, they invented the automobile (the thing that "self-drives", if ya catch my drift :-P). They drilled for oil long before the rest of the world even had an idea what to do with this gooey stuff. They proved themselves as those who re-evaluate all values, as Nietzsche would have said.

They not only predicted the future. They created it.

And so, in a world where noone seems to know where we're heading, some people put their trust in Tesla.

And this is closely connected to something else:

What did Paul Graham say about the most important trait in any entrepreneur that will predict his long-term success?

He said that it's determination.

And I believe that many people think that there few people on earth today running a company that are as determined as Elon Musk.

Who else has bet his entire fortune on his company, at a time when most people agreed that it would go under? Who else has been ridiculed and litererally spat at for trying to build a private enterprise rocket company, and succeeded in doing things that, to this day, not even big governments have been able to day (say, landing and re-using rocket boosters)?

If you read Ashley Vance's Musk biography, there's that one scene that has stuck in my mind ever since. It's about how Elon, back in the days of PayPal, agreed to join his colleagues for a bike tour up some very steep hill. I'll leave it up to you to find and read that story. But that, to me, is all you need to know about the level of determination people see in Elon Musk.

There's other stories like that. Like Talulah Riley telling how Elon got up in the middle of the night and walked through the snow clothed just in a T-Shirt to pick her some flowers.

Now, you can think Elon Musk is a showman and an imposter. You can say he is just floating all of these stories because he read too much Napoleon when he was young and is merely trying to create a myth surrounding his personality, in order to amass wealth and power over people.

But the fact that some people out there are going to see in Elon Musk and in Tesla both a vision for the future and the determination to pull through is something that you better take into consideration when you think about betting against this company.

No, there is another option: this person is here to potentially learn what they were overlooking, from a thought-out debate with others who have a different viewpoint. That would be more constructive than pontificating or looking for sympathy, which was rather uncharitable of you to assume as the only options.

> If you’re so confident, why don’t you short the stock?

The IV was too high when I seriously considered puts late last year. Everyone else was thinking the same thing and enough were acting on it to make the trade unappealing. You can be certain a stock will go from $X to $X/2 and still not find the dynamics of shorting it worthwhile.

Actual short-selling has unlimited downside. You can hedge around that of course, but why bother when there's a route that limits downside in the first place?

Well, options have the added risk that they'll just expire. With options, you've got to get lucky about your timing even more so than when shorting.

Anyway. Nietzsche had a saying. Which is, "Where you cannot love there you shall pass by." Why try to make money by betting against a company when you can just find a different company to bet on instead?

I wouldn't have been betting against Tesla; I would've been betting on a frothy market coming to its senses. Shorting isn't per se a bet against a company, just a prediction that a number will go down. Why it goes down may and often does have nothing much to do with the company. This is also true when the number goes up.

Anyway, that's a saying of Zarathustra's, not Nietzsche's. Author and character are not the same. Deleuze had a saying: "Good destruction requires love."

Because you have a magical thing called a stop loss? Options involve an entirely different slew of variables that require way more complex thinking to take advantage of successfully.

I haven't followed this guy. Or Tesla. But the covid stock market seems like a govt/fed creation. Not to mention gas prices benefiting Tesla like that. I don't blame anyone for not predicting the appearance of giant and unprecedented interventions and their effects.

You're talking contrarian investing when it comes to buying at the time of "peak fear". Yet you don't respect contrarians doing the opposite when there's peak exuberance.

This is false on it's face. The man has rarely spoken publicly. When he did, he has been correct. I'm not saying we should treat him like some sort of prophet, but saying "he's a perma-bear" is just dishonest or ignorant.

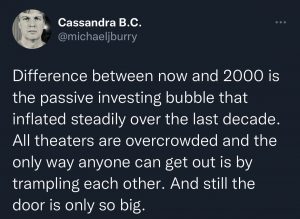

Michael Burry believes that passive and blind investing into index funds is destroying the proper functioning of a market based on valuations, earnings, and future cash flow. True value is no longer priced in based on fundamentals. Another signal of a bubble.

Here's my issue: indexing isn't a single stock or bond - it's compromised of companies who got large because other more active investors already analyzed their fundamentals and found them worth investing in. Passive investing provides inertia to markets, but it isn't totally divorced from them. Companies that have a dramatic fall cough Meta cough will get punted, and the passive investors will only get their feathers singed. It's kinda parasitic I guess of the average indexer like me, but I'm giving up wild gains for a long term commitment to perhaps being a little later to the party than guys like Burry. If the entire index crashes, like, 95%+, we are gonna have MUCH bigger problems globally than people losing their retirement accounts. You're talking about enough companies failing because of the interlocking economy.

I think a big part of the point he's making is tracking error. Your index fund is not the index. It's a fund that attempts to track the index. Many S&P500 funds have a very good benchmark so far, but that needn't be the case in periods of extreme volatility when things like counter-party risk come to bear on moving in and out of large positions.

That's very good, but it's not nothing. If liquidity really crunches, that could theoretically skyrocket. Wouldn't be the end of the world likely, but you could see some non-negligible losses as MASSIVE funds have to move 60% of their portfolios, and all the other traders know it. It could basically put passive investors on the wrong side of the GME nonsense.

Not saying it's really plausible, but it could theoretically happen if the markets moved so fast that spreads effectively stopped trading for long periods.

Ok, but what about the point in the article about the underlying not being traded in 96% of the index trades? Isn’t this hiding valuation, liquidity, or some other aspect of the underlyings?

What's the alternative? Some people have extra cash, and they are willing to risk it in hopes of return.

Is it going to consequentially drive valuations higher than they've ever been compared to history? Sure. But isn't that more of a paradigm shift than a "bubble that may one day pop"?

With more and more people having easier access to investing in index funds... why would it ever go backwards? You'd need people to be sick and tired of risking their money and not having anything to show for it (aka no/poor returns).

The premise to this section strikes me as begging the questiom:

All stock prices move based on supply and demand not theories and strategies.

Well, why do people demand a given stock? One word: dividends. This may seem obvious (or not!) But Robert Schiller in a MOOC some years back made this basic truth clear to me: if a company would hypothetically never pay a dividend, no investor would ever want it. Stocks do not need to trade in large volumes to bring people profit and be desirable. They just need to bring dividends, either now or in the future.

Right. But the person they sell to at some point down the trading line has to believe dividends will be forthcoming. Foreclose all possibility of that, and no one would want stock.

But no company can grow faster than the overall economy forever. At some point spending profits on attempted growth is a waste of money that could've been returned to shareholders (see: Zuckerberg, Mark and the billion dollar quest for the virtual legs).

I didn't see this said in the article explicitly but if the index funds start selling rather than buying, stocks like Apple will probably be OK, but some other stocks that have been propped up by the index funds may have no bid and they can crash. This of course leads to more people exiting those stocks and potentially a vicious spiral. I supposed this could also effect the whole index.

I'm not saying this to try to patch things up with up with you, (because I want my grammar to be correct and will admit a mistake) but it seems the transitivity of the verb is neither as cut and dry as either of us thought.

From the link above:

Although it has been in use since the late 18th century, sense 2 is still attacked as wrong. Why it has been singled out is not clear, but until comparatively recent times it was found chiefly in scientific or technical writing rather than belles lettres. Our current evidence shows a slight shift in usage: sense 2 is somewhat more frequent in recent literary use than the earlier senses. You should be aware, however, that if you use sense 2 you may be subject to criticism for doing so, and you may want to choose a safer synonym such as compose or make up.

I'll probably avoid using the word altogether in the future if it's so contentious.

If stocks are so over priced, can anyone show an example of an fund that's making a killing off of these mispricings?

Why would active management have failed to find and exploit these mispricings before?

Not saying these don't exist but it seems like this is a broad statement that is proven "right" if the market continues to dip and "the market remains irrational" if the market rises. Any claim that can't be disproven should be looked at with a lot of suspicion.

I feel like every crash you hear later about a few places that made a killing. So I'm not sure I understand where you're going with your rhetorical question. I'm sure there are people betting against the market now, too. Maybe they will make a killing. We can't tell until later.

You can never prove statements about the future right or wrong. The closest thing we get is putting your money where your mouth is. If someone does that, I may look on their statements with surprise, but not suspicion.

> The closest thing we get is putting your money where your mouth is. If someone does that, I may look on their statements

Burry certainly is:

“Michael Burry has exited all his positions which as of March 31st, 2022 had a value of +$200 million. Private jail operator GEO Group was the only stock he held as of the end of the second quarter of 2022. This position brought his portfolio exposure down to only $3.3 million”

…

“He is calling for a huge economic recession and market crash that will bring stocks back down to real intrinsic values in the coming year. He’s not bullish on the stock market or current valuation levels.”

Yeah I got a really big kick out of The Big Short. I don’t know how anyone who was a home owner or potential home owner in 2005/2006 could not see what was happening. We sold our home in San Diego in 2006 because it was obvious to me the real estate market was a mirage. I wasn’t some high flying hedge fund manager, just some shlub that could do basic math.

He's right in the long sense... but I still think he's probably wrong today.

But my problem with Burry's logic here, is that there's no "obvious" reason why index funds are unsustainable at 20% of the market. What if the instability point is 40%? 50%? 60%? 80%?

-------

When only 20% of the market is buying-and-holding with index funds, it means that you're still facing 80% of active investors. (That is to say: 80% of your buys, and/or sells, are "against" an active investor).

Even then, I'm personally largely a passive investor. Still, I've moved my money to cash and bonds more heavily, as interest rates have risen. Its not like I've checked out my brain entirely. I still make decisions, just with index-funds as my instrument.

If all the homes in your neighborhood are overpriced people will simply not buy them, and others who are less price sensitive will.

It’s very difficult to “make a killing” off overpriced equities.

Even lay analysts who read financial reports know most marketable securities in the US are overpriced. The ones that aren’t simply aren’t attractive investments.

Go peruse a few hundred US companies and read their financials. Tons of unattractive investments available today.

In the parent's example, "shorting" the overpriced neighborhood may never produce a return since overpriced houses can remain overpriced for a very long time (decades).

This is basically saying "it's not overpriced if enough people believe it to be the correct price" which yeah, sure. In that case it's impossible to make money on most overpriced asset classes (other than those you can make yourself).

> The literal point of the article is that too many people dollar cost averaging is why we have a bubble

Yes, I know. I've been hearing Burry make rumblings on this since 2019.

But if Burry is wrong and there is no bubble (with no eventual popping), then by sitting on the sidelines waiting for the (never-to-come pop) you're costing yourself returns:

The options have decreased dramatically since 2008, since cheap money has pretty much caused all asset classes to have inflated prices.

The best course is/was to start your own business and sell it, since the investment market has/had deep pockets and is looking for alpha above a relatively low benchmark anywhere it can find it.

Real estate was really good for a while (until 2011-2012 or so), but that is back to not being so good today. Note that PE started getting into residential real estate, so that squeezed out a lot of opportunities in that market that used to be easier to access.

My tack has been:

1. Invest in things into which I have unique insights. These aren’t that common, and they are not always easy to access, but they exist.

2. I am holding a lot of cash and waiting for things to correct.

3. I am also building businesses and funding others to do so.

I am not a financial advisor, I am not your financial advisor, and this is not financial advice.

Do you have recommended resources for getting into #3, specifically around funding / assisting others in building businesses?

I am interested in doing so outside of the traditional VC models and tech sector, but the signal to noise ratio of information on building businesses is incredibly low on the web.

> Do you have recommended resources for getting into #3, specifically around funding / assisting others in building businesses?

It depends on on much money you have and your personal network, with network probably being most important.

Some examples (trying to do largest to smallest, but things can scale up and down depending on the market):

BUY AND REFORM

- This is the model for some PE firms.

- This scales from 7 digits (maybe even smaller) to 9 digits (maybe higher). This is sort of what Elon is doing with Twitter now, but Twitter is large enough that the inertia may limit what he can actually do. The 7-digit to 9-digit range will often give you a lot of flexibility in terms of reform.

- You will need to be able to find businesses as well as staff them with scrappy teams (often folks who are riding your coattails who can bring a team with them).

- Good ways to find businesses are looking for once-good businesses that have run themselves into the ground or privately owned businesses whose owner died (possible to find good deals this way) or wants to retire (tougher to find good deals this way since owner often overvalues their business). Another good way to find businesses in tech is to buy tech startups that tried to hit home runs in a singles or doubles area of business and failed. A simple way to describe this is distressed businesses/assets.

- Scrappy teams basically means that you need to have worked with people before in some capacity, otherwise they won't follow you unless you overpay them. Really good folks will often take reasonable salaries in order to work for a good boss who lets them do cool stuff.

- There is a lot that can be said about this area. It is a huge range. Some of the more profitable areas require elbow grease from the mastermind.

- An example of this is someone I know who bought a company that works on something related to utilities (leaving details out to preserve anonymity) for lowish 8 figures, cleaned up the back office, bought up a lot of struggling competitors (basically small independently run businesses that sucked at back office), came up with a creative USP, let it grow, then sold to a large multinational for lowish 9 figures. This person is an incredible leader and had a finance, tech, and sales person who did all of the rebuilding. All of those folks followed him to his next endeavor after the sale.

FUNDER AND COMMUNITY BUILDER

- Basically TinySeed (https://tinyseed.com/). Note that the founders have an incredible reputation in the SaaS community, and they have a very wide network. I think that this is a long play, and it is tough to pull off without building a robust community in a profitable domain with a unique (and highly desired) selling point.

MATCHMAKER AND FUNDER

- I think that this scales most naturally to single-digit millions, but it can scale higher in the right industry.

- Basically find someone who can add some sort of value but is helpless in other areas like admin and/or marketing, find people who can do the other stuff, match them together and fund them. You're the CEO, and it's your business. If done well, you can be relatively hands off.

- One example: Money guy (this would be you), amazing winemaker with limited business skills, strong business guy who can do back office and marketing. Money guy buys a vineyard, tells winemaker to focus on making amazing wines, business guy takes care of all of the extras like on-site revenue makers like tasting room, events, air bnb stays, etc. This took a lot of upfront money that neither the winemaker nor the business guy had access to. Examples of something like this are Folktale Winery (https://www.folktalewinery.com/) and Venteux Vineyards (https://venteuxvineyards.com/).

BE HALF OF THE BUSINESS

- Sort of the same as above, but you are the everything else that the value add person cannot or will not do.

- Scope is relatively small.

- An example of this is someone I know who basically tells any house painter in the US that he will set up the entire business from back office to to marketing to sales, and all the painter has to do is show up and paint. 50/50 profit share.

I'm guessing that's exactly what burry is doing. Let's assume that he is right, and the S&P 500 index is over valued. A big reason why it keeps staying that way is because for the past 10-20 years, there has been a lot of marketing selling these index funds. At this point, most people agree that investment for retirement generally involves putting money in an index fund and that's what people are doing. A percentage of their paycheck goes here.

So, for burry to win, he needs to inform the world of the situation. And when enough people act by stopping contributions to index funds and/or sell their positions, burry is gonna make a killing.

> At this point, most people agree that investment for retirement generally involves putting money in an index fund and that's what people are doing. A percentage of their paycheck goes here.

Withdrawing at retirement does create sell pressure though. The market has to continue attracting new investors for cash out all of the people who are withdrawing later at retirement.

There is a constant stream of people retiring and entering the workforce. There are no cliffs in either, even though people who espouse “boomers!” and “gen z!” would have you believe there ARE cliffs.

> If stocks are so over priced, can anyone show an example of a fund that's making a killing off of these mispricings?

You won’t find them until the market crashes.

The ones who make a killing will simply be the ones who timed the crash correctly. The road is already littered with funds/managers who have timed the crash incorrectly.

> Why would active management have failed to find and exploit these mispricings before?

There is no efficient “buy and hold” way to short the market.

The ways to invest/bet on the market going down are either time-limited or have the potential for margin calls.

Most downside market bets are most efficiently used as balanced hedges rather than pure bets against the market (at least imho).

I'm not aware of any "simply short" ETF. It kind of doesn't make sense. Lets say you've got the underlying asset at $100, what price should the "short" asset be? $100? Well, what happens when the underlying goes to $200, or $300, or $400? The short can't just go to $0, -$100, -$200, -$300. Negative-priced ETFs just don't work (no one will pay up!!)

Instead, "short ETFs" are composed of futures and/or options that move "as if" they were short against the stock. In cases of a rising bull market, the short position is "regularly wiped out" (hits $0), and the assets can rebalance to the new value of the underlying.

Certainly bubbles may stick around for a while and take a while to pop, but how much time should any particular prediction be given before it is busted?

Edit: Pull quote with the central point:

> I thought it was important to clear up the prevalence of index funds, but it isn’t actually even relevant to this discussion. Assets under management do not set prices. Only trading sets prices. The relevant question is not how much of the market is indexed, but how much of the trading is being done by index funds. Since index funds are not doing the majority of the trading, active managers are still dominating price discovery.

This is fantastic, thanks for sharing. Ben makes an argument that stock values are set by market activity (continuous buying and selling), rather than amount held. While the latter may be large for index funds (though apparently smaller than many believe), their activity represents something like 5% of total, so a minuscule amount overall. At the end of the day, stock prices are set by active investors, regardless of how much buying index funds do.

In addition, Felix discussed this in the most recent episode of the Rational Reminder podcasts he co-hosts:

> Are index funds a menace to the market? Are pension funds still a wise way to secure your financial future? In this episode, we discuss index funds, the state-sponsored pension plan in Canada, and much more. First, we unpack the nuances of index funds and take a look at the impact that active and passive investors have on the market. We discuss current index fund trends, when to switch from a passive to an active investor, and the dreaded index fund tipping point. […]

Audio, video, and transcript available. Excerpt (~20m00s):

> It starts with, of course, a Fama and French paper, "Disagreements, Tastes and Asset Prices", which is a great paper that we've talked about many times, including with Ken French, who is very excited that we asked about it. They have this paper that shows that if misinformed and uninformed active investors who will make prices less efficient by trading, switch to market cap indexing, market efficiency actually improves. That's the comment that you made earlier, Cameron. It gets harder to be an active manager, because there's more competition. That's the relative level of competition as opposed to the absolute level is what matters.

> If informed active investors, so the ones that are doing a good job, setting prices that the skilled active managers, if they switch to indexing, then in that case, prices do become less efficient. This is the concern, I guess. If everybody, including the skilled managers go to indexing, then there is a concern about ongoing marketing efficiency. As long as there are some remaining informed active investors, even if there are a few, a small few, as long as they're skilled, and they command a lot of wealth, which they would, and we'll talk more about the empirical side of that in a second. As long as there's a few left and they're competing with each other, theoretically, prices remain efficient, and arguably, even more efficient than they were in the case where there were still some unskilled managers.

The biggest bubble for the past 20 years has been in bonds. Stocks went along for the ride. When you can't get a reasonable return on debt, you'll be fine paying for a zero coupon stock that has the chance of 10xing (Tesla.)

The script has now normalized and may soon flip. Say the Fed unloads it's QE balance sheet from even as far back as '08. Debt will become extremely attractive and there will be a massive allocation out of relatively low yielding index funds into debt.

Right now yields are eye poppingly good, and we're not even quite to the long term historical average of 4.5%+.

Also, there's a lot of fear of certain forms of debt that are actually safer than they've ever been. Mortgage REITs for example are incredibly attractive especially after the post '08 regulations. The shift back towards debt and classical savings is what will drain the market, not some index fund issue--although I do agree index funds will probably underperform some active managers until they rebalance towards businesses with nearer term cash flows.

For everyone screaming about a depression, go out on a Sunday to a restaurant. Everything is packed. Working people are making a better wage, inflation has slowed, and they get better savings at their bank.

Finally, I know there's this narrative that governments will "inflate their way out of debt" which makes debt more risky. Sure this is a possibility. It's just as possible as a company issuing more stock, but it's not guaranteed. There's a political question that needs to be answered. Maybe we solve the debt issue by taxing those who benefited disproportionately from ZIRP more. Maybe we just slow government spending and let the economy continue to expand on its own. We as a country get to decide whether we inflate it away or we do something else along with who benefits and loses from that process.

That's the risk free rate. Go look at other debt instruments. You can find yields on corporate bonds from solid companies in the 10+ range (Citrix), mortgage baskets go even as high as 16%.

Investing for retirement shifted from a company taking responsibility to employees taking responsibility with the advent of 401k and similar plans instead of defined benefit pensions. Over time it has been noted that picking individual investments tends to do worse than simply buy everything.

As workers pour money into these non-discriminating investments, hoards of people are blindly investing and skewing away from efficient markets. Everyone (scare quotes everyone) is just buying large swaths of everything all the time without regard to fundamentals.

It's all good as long as this continues, but a shift in enough people no longer believing this, will reduce demand and prices will go back down.

In other words, people just buy everything because there is no alternative. If enough stop doing that, prices will readjust downward because too many stocks are overvalued due to the current wisdom of buy regardless of price.

I'm not an expert but I still don't get it. If everyone is buying everything then the whole market is overvalued? Is it possible for everything to be overvalued? Overvalued compared to what yardstick? Stock performance is also not a direct indicator of future company performance. At the end of the day buyers are still taking an educated guess at the future. If everyone does this randomly aren't we just back to the whole market being invested in? If it's not random and skewed to popular companies like Apple or Coke then isn't that another artificial thumb on the scale?

Isn't Burry in essence saying that if everyone sold all their stocks then the market as a whole is a bubble?

Some missing nuance here is that the s+p 500 is not everything!

It's a subset which has essentially been selected for long term performance. There may be a couple Enron's hiding in the set, but on average they are good choices, with much lower risk than the average company not in the top 500.

Yes, there is some hand waving, but it conveys the general idea that current wisdom and circumstances have made investing in large sets of stocks all the time with no regard to the underlying fundamentals does put an upward pressure on prices.

No the s&p 500 is not "everything", it is one, albeit very popular, index. There are many others, but the underlying concepts are the same. Further, the companies are not selected for long term performance. Ignoring some finer details, the s&p 500 is the largest 500 US companies by market cap. Perhaps you are confusing this with the DJIA which is hand selected, though not selected for long term performance by any means; rather, it is selected in a way to represent the economic landscape - how well it achieves this is a matter of debate for sure.

The comparison he gives is that of a theater which keeps getting more and more crowded but the doors remain the same. In the bull market everyone keeps buying more and more index ETFs which are highly liquid. However, over half of the underlying securities have low trading volume. As long as investors keep piling into the ETFs there is no problem. But when investors start selling the ETF, and the ETF has to sell the underlying equities, then prices may fall much faster due to low volume and no demand.

Isn't there also compounding factor here due to them relying on index and rebalancing that. So selling without corresponding demand means that price will drop more than index thus meaning that funds will sell more of that stock to fix the index. Thus generating more downward pressure.

An index fund is an investment you can pick that is a basket of individual stocks.

They are an easy way to get diversification in your portfolio and historically have beat out portfolios where people actively picked out their own mix of individual stocks.

A lot of the investors in the world are just investing in index funds which has artificially inflated the value of the stocks in each index fund.

When an investment has an inflated valuation that does not match the fundamentals of the underlying business behind the stock, there is a bubble.

Markets are supposedly efficient because people pick to buy companies that are good value for the profits they generate and sell companies if they become less valuable.

If people are buying index funds automatically in retirement accounts they are not making this judgement and thus all stocks in index funds are selling at a premium because of this automatic buying pressure. If enough people do this there is potential for the stocks in index funds to be overvalued.

An index fund is a group of stocks. You buy them all together. That means that you're buying everything regardless if everything is worth buying. If tons of money gets put into the index funds, all the prices rise. This could mean that there are mispricings in the market that could eventually hurt the buyers of index funds.

Index funds are still regarded the best choice for a long term passive investor because of the amount of diversification.

He's stating that too many people blindly believe investing in the top 500 companies in the United States is a good plan. This strategy was recommended by Warren Buffet after he won a very unscientific bet.

Michael Burry believes that these people will later want to exit their positions, and won't be able to because the amount of people entering these positions will be lower than those exiting. At which point, the bubble will pop, as the market won't produce buy offers as fast as people attempting to exit their position.

>Passive investing has removed price discovery from the equity markets. The simple theses and the models that get people into sectors, factors, indexes, or ETFs and mutual funds mimicking those strategies — these do not require the security-level analysis that is required for true price discovery.

Maybe with enough blog posts and Bloomberg interviews, we convince everyone to go back to a culture which prefers more complicated, specific investing strategies. But after you completely destroy peoples' wealth by crashing the index fund plane, how exactly are you then going to convince them to buy into your focused strategies (and importantly, with what wealth)?

Its the stock market. The only certainty you have is that it will always remain chaotic. Specific investment strategies are what helps build index funds. Without that you'll increase risk acossiated with index funds. There IS too much reliance on index funds right now and once the S&P drops significantly you'll run the risk of losing far more than if you hadn't relied completely on its basket.

> Michael Burry has exited all his positions which as of March 31st, 2022 had a value of +$200 million. Private jail operator GEO Group was the only stock he held as of the end of the second quarter of 2022.

Burry had a great play last year of shorting bonds via TLT, unfortunately he was about 6 months too early and his option positions expired before it collapsed. His thesis was based on "hyperinflation" occuring in the USA, and while inflation has increased it's still far from "hyper". Point is, his thesis may be correct, but his time horizon may also be off.

And herein lies the problem with being contrarian. It’s impossible to be both contrarian and correct with sufficient reliability that you beat the market. You will get it right sometimes and wrong other times. But not consistently.

Everyone should go and read A Random Walk Down Wall St and Irrational Exuberance. For a retail investor, the first book teaches you that beating the market is a random process, so there is no point in trying. Any advantage you gain from being smart will be paid for in time invested in being smart enough to beat the market.

Irrational Exuberance teaches the retail investor that markets go through long, yet unpredictable, periods of irrational behavior. Even experts struggle to explain the movements of the market, so as a lowly retail investor, you’re unlikely to have any chance at winning the game.

Ultimately, while each book looks at the world in a contrasting way - one assumes investors are collectively rational and the other assumes the opposite - the lesson is the same for a retail investor: just live your life, invest passively, and give up on trying to get rich quick in the market because it’s random whether you’ll succeed.

If I was advising someone fresh out of college starting their first job, I would suggest they start a 401k and put 100% of it into stocks. They have so much time in the market that anything else seems unwise.

I am genuinely curious what better alternatives are on the table? Sticking retirement money into other vehicles seems guaranteed to have more tepid (if consistent) returns. For someone at the start of a 40 year career, the additional volatility seems well worth it.

Additional volatility is worth it until you hit a 50 % drawdown where someone who was only partially invested would have a 20 % drawdown and then rebound faster.

Remember that investments compound, and it takes as long to go from 10 to 100 as it does from 100 to 1000. Avoiding drawdowns is critical for long-term growth.

You want a significant fraction of your wealth in stuff with tepid and consistent returns. In fact, you want this fraction to be constant over time. That will outperform any one asset class as time goes by.

Consider me still dubious. A 25 year old to 35 year old, starting from $0 with annual contributions of $12k in a 100% stock vs mixed 50% stock and others, I would bet 9 times out of 10 on the full stock.

I would have to see some models to contrast, but I still suspect that given the timeline, the stock heavy portfolio is going to outperform if only because of DCA.

I heard this argument before 2020s crash. I exited early before it because I feared his prediction. Did it hold up during 2020 crash? In March 2020 everything crashed very fast but also rebounded extremely fast when the fed turned on the printing press.

My personal opinion is that what matters is just the Fed. Index bubble, everything bubble, crypto bubble. It all doesn't matter, what matters is just what the Fed is doing. And the Fed is a few mistake prone officials who could forget to turn on interest rate for an entire year, so whatever Jerome Powell had for breakfast might end up being more important than what an experienced economist says.

If your concern is that equities are priced above fundamentals of how much the underlying businesses will return, cryptocurrency is no salve: the underlying fundamentals of cryptocurrency are zero.

Bitcoin is a scarce asset, there will only ever be 21M. So based on the number of people on the planet and Bitcoin’s growing adoption with both individual and institutional investors, I’d say the fundamentals look pretty good.

A worthless stock (no underlying fundamentals) can be a scarce asset too.

We can all decide that shares of Worthless, Inc. are worth a bunch of money and collect them. But we can't really expect dividends or an acquisition premium in the future.

Not really, I could fork bitcoin and mine bitcoins that no one wants. Which you might argue is unfairly representing your particular cryptocurrency but you'll have to admit that any better cryptocurrency at any point can reduce the value of bitcoin by 100%. Just because it has never happend doesn't mean it cant.

This differs significantly from real estate or gold, which is backed by a tangible representation. With a virtual currency, there is no floor to the amount of losses. Theres also no dependent economic activity to support it right now and any dependent economic activity could be replaced all the same.

Who knows what's best to buy right now in this environment.

I'm just making the point that, if stock A trades for $10, and one is concerned because they believe the "true" net present value of its share of the business of $5... that the situation isn't improved by buying asset B that trades for $10 but has a zero underlying net present value.

(Asset B may very well do better, because underlying values are not the only reason we buy assets...)

From an investment perspective, bitcoin does not have a significant advantage as a store of value as you would think. Its expenditures are in energy+equiment hash rate, which is going up at the rate of value being put in. and its profits are based on transaction costs, which are also going up in tandem with the value put in.

Take away the speculation and you'll have a zero-sum game which always leverages power costs trough transaction processing. So the store of value is a benchmark of computational energy.

index funds will have better track records than bitcoin, even if all index funds drop 50% tommorrow.

Bitcoin is a negative sum game. In an ideal world without a supply shortage of mining hardware and without regulations the Bitcoin price would match the production costs of a block. Next to all profits then go to electricity providers, thus leaving the game.

don’t the incentives drive miners to cheaper sources of energy? how does that non linear variable factor into your zero sum argument?

re speculation— I don’t think you can remove it from the equation. Equities are highly speculative. The market can remain irrational longer than you can remain solvent. I can’t count the number of times positive earning reports are expressed in negative movements.

If your source of energy gets cheaper, you would capitalise on that by increasing your hash rate in order to get an advantage in the hash checksum lottery. The profitability of bitcoin mining has always been your hashrate/cost, and your cost has always been the total cost of ownership of your equipment. That includes power.

Speculation would be fine if it helped price discovery but it has become clear to me that bitcoin is far too irrational for me to partake in other than keeping the little exposure that I've had so far. I'm sure there is some mathematical hash algorithm/proof of stake/distributed accounting that could serve a better job as a financial tool than relying on government-issued currency with a high risk of inflation as a result of poor debt management. But no crypto can satisfy all factors that investors would like.

* Decrease in transaction costs as the new protocol matures

This is historically what happened as technology, computing power, bandwidth improved. Bitcoin would require changes in protocol in order to make this happen, like Ethereum did.

* significantly better balance between early investors and late investors. A million increase in value between early and late investors just destroys the store of value idea as its a pure speculation instrument. A currency with a very stable inflation rate could outperform the dollar if enough markets used it.

* better integration with long-standing agreements like insurance against theft, loss, recalls and other tools everyone expects to be able to use from a functioning society.

I mean from the fundamental Burry warning makes sense. At its heart, a stock market is a way to exchange ownership in companies. The point is for people who want to be owner to buy from others.

If you are buying blindly, pricing doesn’t work anymore. Same with speculation which is tolerated because it brings liquidity and helps prices converge but is very much a by-product.

> I mean from the fundamental Burry warning makes sense.

Does it?

He's not "wrong" to call out the side effect of millions of people "blindly + consistently" pumping their extra cash (savings) into index funds in hopes of return. Sure, this means the market is "crowded" compared to historical times (we're probably at all time high for market participants from a retail/average investor perspective I would guess?)

But... what's the alternative? How are you going to tell millions of people "we'd like you to stop investing in the market/deny you access to the chance for 6-10% index-fund-level returns because you're driving valuations up"?

> But... what's the alternative? How are you going to tell millions of people "we'd like you to stop investing in the market/deny you access to the chance for 6-10% index-fund-level returns because you're driving valuations up"?

You don’t need to tell them to stop. If the sole thing pumping these stocks up is excess savings as soon as the economy slows down it’s not going to be sustainable. Some of these stocks will go down as people remove their money from the market and people will lose money. That’s the heart of Burry warning.

Note: I’m one of the founders in the above. Basically built Pebble to for passive index investors (like us!) who want to be safely/easily diversified but in a manner where we can still express individual ideas/needs. New launch coming soon :)

Outside of Pebble - Fidelity Managed FidFolios will get you close. Not the S&P 500 exactly but their own US Large Cap portfolio which you can customize.

Everyone's reasons are their own. For me personally there are some reasons that are more utilitarian in nature... and some reasons that are value driven.

I removed Tesla because it entered the S&P 500 after a huge run up. I own the car (and love it)... def the future. But I think the stock has been overhyped. There are more diverse ways to invest in EVs being the future vs "just buy Tesla".

On the other side... I removed FB because honestly I just didn't like the company (so a values reason). This was well before the whistleblower, etc. Was not looking at that one through a performance lens. Just wanted nothing to do with the company.

Most of my edits are removing companies that I already have too much direct exposure to.

Imagine an investor who owns $100,000 of SPY. Therefore, they own roughly $12,000 of Apple and Microsoft (together, they account for 12% of SPY)

If that same investor thinks Microsoft and Apple are at their long-term peak, the investor is forced to hedge against their own positions in those stocks because they can't exclude them from their SPY holdings.

I held a lot of PUT options and was shorting TSLA stock in 2021/2022... meanwhile I also owned a lot of TSLA through my index fund holdings (I would have much preferred an ETF that excluded TSLA, rather than owning TSLA via SPY and actively shorting the TSLA position simultaneously). This is something I did in the past, and my gains would have been higher had I had a way to remove TSLA from my index fund holdings without spending money on PUTs or shorting.

The whole point of index funds is that individual decisions - no matter how well reasoned they appear - don't seem to work out long term. The decision protocol that looks good today and may have worked once, twice of five times in the past will eventually lead to a ruinous decision later on that wipes out all the prior gains.

If the logic you describe works for one company why wouldn't it work for two, or five or ten out of SP500?

Heck if you can indeed pick any winner even by just a 2-3% gain than the passive index, why wouldn't you better off by building a fully custom curated SP500 that contains companies that are more likely to succeed? That 3% adds up to massively more money long term.

The whole point of active trading is exactly that, a thinking logical human being, adding all their intellect ought to be more successful than passively doing nothing.

Yet history says otherwise. Even when faced with decades long evidences active traders still believe they can do better than passives.

Past results are not an indicator of future performance.

I think the same trope applies to the classic thinking of “passive investing is always better than active investing”

Historically, yes. But in the future? Who knows! (This is also exactly what the article we’re commenting on is speculating, that the characteristics of ETFs in the market has changed substantially over the past 10-20 years, which is indeed an argument that past performance isn’t proof of future performance.

That is a valid point - no one knows what the future holds

But we have to take into account that the active traders have been repeatedly making the same claim. How many times is one allowed to make the a similar claim before losing credibility...

You can buy an S&P 500 index and short exactly the holdings in the three stocks you want to remove to achieve this. Shorting comes with fees, but it's the closest you can get with normal human amounts of capital

With the direct indexing products many brokerages have rolled out lately, you can now also create your own subset, superset and/or re-weighting of an index and invest in that.

One additional thought is as individuals enter the workforce they’re told to invest in a 401k. I’m assuming most people put their contributions into passive investments. Over the long run I wonder if this is significant enough to lead to a cycle where stock prices always go up.

On the other side you have people in retirement drawing from their 401ks. The population imbalance probably works in the market’s favor now, but that might not always be the case.

This is what the article is saying. As long as everyone else keeps doing that, it will be a good idea for me to do it too. But when fashion changes and it is hip and cool to do something else, it will be much harder to get out of the top 500 companies because nowhere near as many people will be buying.

Its possible index funds become less popular once they stop being the easiest way to get strong market returns without expensive

management fees. In a world of higher interest rates and a more stable equity market I could see specialized funds etc becoming more attractive.

The underlying reasoning is that any system that is too uniform is fragile.

In this case, the common belief that S&P500 is safe is valid up to a point, if too many people rely on this assumption this can turn into a big problem.

It's easy to predict a crash is coming: there's always a crash coming at some point in the future. Harder to get specific about when and what magnitude it will be, with dates, metrics, and numbers. Since you ask people to cash out and sell their positions, are you confident enough to be specific?

What I don't get about Burry is that he is so all out talking about the end of capitalism sometimes even the end of the world without doing anything with the money he made in 2008. He just sits there in his mansion shitting on everyone. dream job I guess.

This makes no sense. stock prices are a function of earnings. for passive indexing to fail would imply a major recession, which would be bad for all stocks

Stock prices aren't simply a function of earnings.

Perhaps with complete transparency and a reasoning, logical market they might be closer to that, but that's not what we have. Even in that case you've got more than earnings to concern yourself with, like risk assessments, d/e ratio, dividend rate, and much more.

Earnings are a fundamental factor. Forward earnings as well. In the last bull run, market caps skyrocketed way beyond sensible forward P/E because rates were 0% and growth equities were worth the risk. Now that rates are going up, the risk profile has changed. In the last year growth stocks that have not shifted to value stocks have been slaughtered. Think meta, snap, etc. At the end of the day there are way more factors than earnings influencing price. The options market even has a big impact on underlying assets. Anyways the risk profile has changed and value will become a stronger factor.

IIUC the point is that index funds abstract the price of some stocks even further from earnings. Because a large percentage of the trade volume in those stocks comes purely from the index fund trades, rather than direct trades that would cause proper price discovery. So when the ETF bubble bursts, those stocks will see and even larger correction down than otherwise.

What part doesn't "make sense"? If he predicts earnings going down and prices going down even more selling 99% of his portfolio - down to one single stock - seems consistent with that view.

{kind=link}

All of this said, these things do take time. This kind of rhetoric will slowly spread until it reaches a fever pitch, likely sometime in the second half of 2023.