An interesting aspect of this is that the endless printing of money in the last few years was a sort of stress test of modern monetary theory, which has been seeing lots of discussion in those same years. I never quite understood how this theory would work while avoiding inflation, and what's happening now seems to at least be related - https://www.nytimes.com/2022/02/06/business/economy/modern-m...

Conceptually the answer in the theory is to suck up the excess money with taxes, which of course is not going to fly in the US. But maybe this inflation will make that more viable in the future:

"Ms. Kelton and her colleagues make clear that the pandemic relief packages did not follow one of M.M.T.’s key tenets — they did not try to account for resource constraints ahead of time. In an M.M.T. world, the Congressional Budget Office would have carefully analyzed possible inflation ahead of time, and lawmakers would have tried to offset any strain on available workers and widgets with stabilizing measures and tax increases."

An important point to keep in mind when talking about MMT in a policy setting is that the people who will implement it don't care about theory and will make a series of short-term politically expedient and/or vaguely corrupt decisions. If they implement MMT, there are good odds that it will just look like money printing.

It doesn't really matter what the academic plan is, the policy isn't going to follow it. Much like how interest rates were supposed to rise after being dropped to emergency levels a decade or so ago and instead a 25 bps rise is front page news.

All the politicians/relevant voters are looking for is a green light to hand out money and some buzz to say that it'll make everyone better so ignore the doubters. If they cared about good economic policy the last few decades would look very different. The dominant ideology is that centrally planned interest rates are a good idea, and that is questionable.

Yeah, happened with both monetary policy as you observe, and with Keynesian fiscal policy - deficit spend to cushion and shorten downturns, then contract govt spending and pay down the debt during good times, so that you can afford to deficit spend again in the next downturn.

Makes sense in theory, but the second half doesn't always happen b/c politicians like buying votes with govt spending (either via under-taxation or over-spending, to the extent those aren't the same thing).

Or alternately raise taxes in the good times (rather than interest rates) and pay down that debt... which at least in the US we've got one political party dead set against at all costs.

A generation ago, progressive cycles of deficit spending and taxation had put the top tax bracket in the US at 90%. Still, there was persistent inflation - and worse high unemployment.

The belief was that the Federal Government had grown too large in the economy and needed to be "starved". To what extent government austerity vs. new monetary policy moved the needle for the US economy is unknowable. However many Americans of that generation feel that the starve the beast approach was correct.

If you talk to Americans opposed to new taxes, their opposition is usually based on the idea that the government will waste the money in one way or another. Even those on the left in favor of taxes are often in favor of taxes for redistribution purposes. It's rare that anyone pitches the government as competent outside of military spending, and even then there are many asterisks on 10k light bulbs in submarines.

If you want Americans to agree to taxes you'll need to change the perception of government competence.

> A generation ago, progressive cycles of deficit spending and taxation had put the top tax bracket in the US at 90%. Still, there was persistent inflation - and worse high unemployment.

AFAIK the "90%" rate is highly misleading because at the time there were a lot of deductions that bring the effective rate much closer to today's levels. We can see this in the federal tax receipts as % of GDP, which remained mostly flat despite the top bracket dropping from "90%" to 37%

"A generation ago, progressive cycles of deficit spending and taxation had put the top tax bracket in the US at 90%."

This is incorrect.

The 90% tax rate (and other notably high tax rates from that period) were temporary measures explicitly enacted to discourage war profiteering:

"The crisis of World War II led Congress to pass four excess profits statutes between 1940 and 1943. The 1940 rates ranged from 25 to 50 percent and the 1941 ones from 35 to 60 percent. In 1942, a flat rate of 90 percent was adopted, with a postwar refund of 10 percent; in 1943 the rate was increased to 95 percent, with a 10 percent refund." [1]

These were not tax rates analogous to any of our normal, peacetime rates and they were not enacted as progressive policy measures.

It is misleading and disingenuous to make any comparison between the tax rates we choose in modern peacetime which arise from political decisions about relatively progressive vs. regressive rates, etc., and these administrative rates designed to combat war profiteering and other behaviors related to a wartime economy.

No, but there is a method to the madness. Military units are often given an allowance for the year. One of the responsibilities of a commissioned officer is to often manage the unit's finances. Being in the Navy, my Bosun manage my aviation fuel division's finances. The captain of the ship manages the ships finances. Or at least, they sign it all off. If units do not use their budget, their budget get slashed last year. Essentially money mismanagement comes down in many way to some rules implemented awhile back (80s I believe during the Reagan admin). If a government agency or group does not use the full amount allotted, then they are at risk of loosing some next time they are allotted money. What this has done is create a system that encourages government agencies and military units to use up the budget no matter the cost. You don't wanna be the guy who had money left over last year, so your budget got cut, not it is this year and you had 4 major equipment casualties and because your shortened budget, can't afford for the unit to buy parts. Then, this makes you looked incompetent and hurts your career.

This is why the fuels division I was in, we often bought new desk chairs every year and $500 pocket knives and parts we would never need. Literally had to throw parts away to make room for the new parts.

Nope, but the military gets a pass in most years as at least being competent. Most Americans believe that most government agencies are both incompetent and profligate.

That's too broad a brush. I'm against militarism, but what engagement against conventional forces has the US military lost in the last 20 years?

I can't speak to dealing with insurgencies but it's clear to me that a mix of various administrations policies was to blame more than military effectiveness.

I mean was it the military or Paul Bremmer and co who disbanded the Iraqi military and unleashed a lot of chaos?

I don't want to say yes but damn if we don't have a lot of military might, and as much as an American I want to say stop spending it who will fill the void? We're probably the least bad of all possibilities, and if you disagree, please teach me because I'm legitimately open minded!

The first is that other Western countries could pick up the slack instead of having it fall disproportionately on the US. It only got the way it is because the others were mostly bombed out after WWII and that's no longer the case.

The second is that if the US spent less and did less military interventionism, adversarial countries might not feel the need to spend as much either, and then the balance of power stays the same while everyone spends less money on bombs and warships.

The US is the only one who can initiate this because they're the only ones who can reduce military spending without being threatened even if others don't.

The perception is created by billionaires buying "news" media to spread propaganda to get people to vote against their own interests, leading to "hurts itself in its confusion" attitudes like "keep the government out of my Medicare".

The Kochs, leaders of the "small government" movement are the heirs of a billionaire whoade his fortune building oil refinery for communist USSR government. They only dislike government when it helps the people instead of the oligarchs.

Ironically the thing about the Kochs is a little bit reversed. They have their own agenda, to be sure, but the biggest players in the influence game aren't individual billionaires, they're corporations and government bureaucracies.

The media always dumps on the Kochs because, atypically, part of their agenda is anti-graft. Make the government smaller by reducing corrupt spending programs and regulatory capture. Most of the bureaucracies fight each other for resources but they're not trying to turn off the spigot. The one who does becomes a target for attack. So they're the ones you've heard of.

I assume you're taking a swipe at Team Red, but do remember that the recent TCJA had a provision that removed the ability to deduct state/local (SALT) taxes from your Federal taxes due, above a certain amount. One could consider this very fair: if you argue for higher (Federal) taxes, you should pay what's owed, regardless of what you paid to any local governments, especially since you have much more control over where you live and the taxation policies at the local and state level.

The uproar about this change from Team Blue was palpable; this was clearly a targeted attack on liberal, high-tax areas. The cutoffs for the changes were well above an income level of $150K, which meant it went after the 'rich' that Team Blue always positions as the enemy, but none of that mattered.

Nobody wants more taxation when it actually hits their pocketbook. If there's anything the constituents of the two major political parties can agree on, it's that.

It was a tax cut bill with tax increases targeted at political enemies. There are many other loopholes that could have been closed but Trump was all about attacking political enemies. The anger wasn't at the tax increases it was about the abuse of power.

Somehow the Red "cut the taxes and spending" never give back the net inflows they take from Blue states....

Blue states have higher taxes to care for their citizens so they have to take less in Federal handouts.

What's the distinction? I always assumed "blue states" meant a majority of voters in that state voted blue, likewise for red states. Otherwise you might as well say "there's no blue cities, only blue neighbourhoods" and keep getting more granular down to the individual voter.

The distinction is that cities are blue and non-cities aren't, as a rule. "Blue states" are just states where the majority of the population lives in cities.

California is a net recipient of federal money (though not by a lot). The biggest donors are the blue states in the northeast. But plenty of blue states are recipients and the biggest recipients are the swing states, because politicians shamelessly buy their votes.

And the reason the states in the northeast pay the most isn't because of state-level benefits reducing the need for federal programs (which rarely if ever happens). It's because those states are disproportionately the wealthy people who pay the most taxes.

But getting rid of the SALT deduction didn't care about that. Wealthy people in California lost more than equally wealthy people in New Hampshire, even though California is a net recipient and New Hampshire is a net donor, because New Hampshire has lower state and local taxes.

A state being a net contributor generally means they have a lot of high paying jobs and successful companies concentrated in their state. Michigan is actually a good example as you can see when the big 3 auto companies were at their peak the state was a net contributor, but it has been a receiver since their decline.

But that's not how the federal government is supposed to work? The whole point is for them to engage in redistributive policies, which means you inevitably have "never give back the net inflows they take". I'm sure economically unproductive areas (eg. rural areas) "never give back the net inflows they take from" economically productive areas (ie. major cities), but we don't give people living in cities a tax credit.

This also points to a weird but true situation: Many blue states would be financially better off (or at least neutral) to eliminate federal programs and replace them with state programs, because the smaller the federal budget, the smaller the net outflow from blue cities.

But then they weirdly push for the opposite to the financial detriment of their own constituents, including the lower income ones who could have higher state benefits than existing federal benefits if the feds weren't taking so much of their state's money.

Best guess for why this happens is that the blue team is more captured by government sector lobbyists at the federal level, who don't want to lose jobs to state level government workers.

Even the extremists admit (thought they try to hide it) the Bill Clinton paid down the debt by raising taxes and cutting military spending by not starting large new wars. Caro insulted Clinton for proposing a $200B/ye deficit, right before Bush 2 issued a one-year addition of $1T in new military spending for his personal vendetta against Saddam Hussein launched on false pretenses.

The 90's sure were great, I miss voting for Bill! But those days are long over, and most partisans today seem brutally disappointed in Biden because he's only spent $1 trillion instead of $3 or $4.

I'd highly recommend the historical fiction "Red Plenty" which followed the trajectory of Academics in the soviet union trying to compute idealized prices - meanwhile administrators, consultants, and realists had to just make the system work.

At one point a quota increase leads a factory to sabotage it's old equipment, so that they may get a new machine to hit the quota. The administrator in charge of approval determines as much - and arranges for a new machine. Unfortunately a pricing reform introduced by the same plan leads to an inability to build the new piece of equipment as equipment was priced by the ton. Requiring the intervention of "well connected" individuals to solve the problem...

Systems adapt - any reform will introduce exploits, and pathologies. To pretend that MMT based central planning yields a different outcome in the long hall is folly.

I mean it did make everyone better. The COVID pandemic could have really wiped out a lot of people and we printed money and it helped.

It’s the austerity people that have never cared about anything but their ideology. Austerity for austerity’s sake has caused unfathomable human misery in the globalization era.

Right now the labor market is good for workers. That is good. Getting there has always opposed by the ruling class interests though which is why we haven’t pursued it.

MMT at it’s heart is just an increasingly large number of voices screaming out “fucking STOP” and actually try to get to a relatively tight labor market, because on the whole doing so is better for most people.

Yeah sure inflation is an issue but as we are seeing now it’s always been something that can be addressed by putting on the brakes a little.

And for the record I have a degree in economics. I get the other side of the argument. My point of view is that the other side of the argument and elite economists have been fundamentally corrupt in their analysis for decades.

“I mean it did make everyone better. The COVID pandemic could have really wiped out a lot of people and we printed money and it helped.”

Well, let’s see:

1. I got maybe $3k from the government due to all that printing.

2. The price level is easily up 25% for things I need to buy, like food, fuel, computing equipment, and vehicles.

3. And I still got Covid, as did literally everyone else I know. My brother still can’t taste anything and a guy I work with died.

If that’s what you guys with economics degrees call a win, I will update my priors from “you guys are idiots” to “you guys are a cult that uses math to further the work of Satan.”

Do you have so little respect of your fellow man that you think they are incapable of thinking? A big part of the spending was designed to float businesses during lockdowns to “flatten the curve”. The idea being that paying people to stay home would reduce risk of infection. They are pointing out this outcome did not happen.

>Do you have so little respect of your fellow man that you think they are incapable of thinking?

Funny, I was thinking the same thing about the above comment I was replying to.

>They are pointing out this outcome did not happen.

Flattening the curve absolutely does not mean preventing people from getting COVID; it's about lengthening the time horizon in which the population gets infected to reduce strain on the health care system.

Moreover, a personal anecdote about getting COVID doesn't imply an overall policy failure. Just because someone let sick people cough in their face doesn't mean they should wax intellectual about macroeconomics.

I mean, did it? What evidence do you have for this claim?

Vaccines absolutely helped. But now everyone's wages are going down -- it was basically ~$3k stimulus checks that were actually loans with a 400% interest rate.

Real workers wages are falling. Inflation fundamentally increases inequality, i.e. people who own assets watch the value of those assets increase while people who work for income watch their income fall.

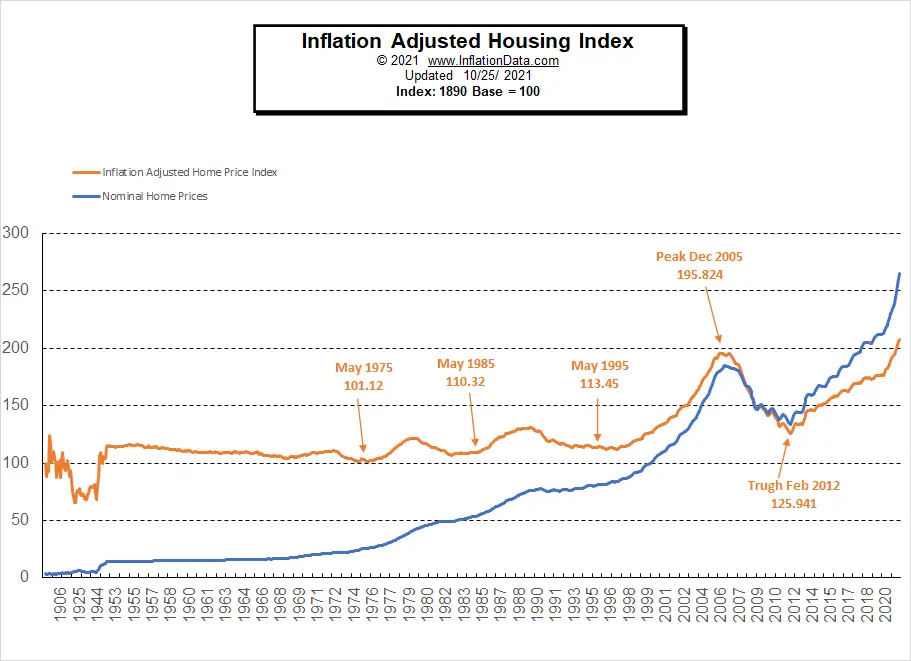

It is good _nominally_. Real wages are basically flat. Meanwhile, for everyone who didn't get a raise or can't currently find a new job for whatever reason, they're losing purchasing power. On top of that, the housing market has been completely destroyed by the Fed printing money and shoving it into mortgage backed securities. In many nicer areas of Southern California you used to be able to get a starter home for $600k (manageable for someone in a working class profession like a nurse or mechanic), now nothing on the market is less than $1.2M.

Also you forget that a big reason the labor market is so tight is because a couple million Boomers retired early during the pandemic.

Well I think a big contributor to the current inflation problem was the last round of stimulus passed right as the pandemic was starting to wind down. At that point unemployment numbers had almost gotten back to normal and most revenue numbers for things like restaurants, travel, etc. had recovered to at least 70% of pre-pandemic levels. And then some states like California dumped even more money into the economy through multi-round state funded stimulus checks over a year after the pandemic started. The unemployment programs also should have started winding down the moment vaccines were widely available rather than 6 months after the fact.

I personally know a lot of people that just dumped their stimulus checks on memecoins or wasted it buying spurious goods. I'm sure the used car and electronics market also was greatly affected by stimulus as well.

The Fed also should have limited its stimulus to buying Treasuries rather than MBS. It makes no sense for the government to buy mortgage backed securities (basically a freebie to homeowners/homebuyers who are already wealthy).

I expect it's years of money printing to avoid a dip in the middle of the largest demand drop we've had in a very long time, following by a resurgence in demand as folks get out and try to get moving again (resulting in them spending a bunch of that money all the sudden).

It's pretty predictable IMO.

Either we'd have to drop the economy during the demand slackening during COVID (which would have caused a severe recession, because it WAS a recession in activity, and then there would be a bunch of panicked people in the middle of a pandemic who also lost all their income running around and maybe setting even MORE things on fire), or inflate our way out of it.

Hopefully we don't see some crazy 25% inflation like the 80's, but I wouldn't rule it out.

I'd expect that in a few years it'll flatten out though.

I haven't seen the actual data, but a Stanford economist compared the stimulus payments with actual consumption and it's pretty apparent most stimulus dollars were not spent, but rather used to pay down debt or invest (hello r/WSB!).

Never said TCJA or the Bush era tax cuts were used for good purposes :) but it's probably better for the country in the long run to have excess money flowing into tech VC funds rather than being spent on memecoins and shitty electronics. That way maybe 1% of the funds will have positive returns rather than all of it being set on fire.

I'm just saying in the absence of any alternatives (which I'm sure there are), it's better to have 1% of trillions of dollars going towards advancing humanity and technology than 0%. I am fully aware that 99% of that money is going to be burned on WeWorks and the like.

Oh good. I was worried that there were still people earning income from exploitation, rent seeking, monopoly, cronyism, and leveraging principal-agent conflicts of interest but looks like that’s all over now.

Seems to me if real wages are flat or mildly increasing and it’s WAY easier to get a job that’s a way better world to live in for the kind of people who apply for jobs.

MMT is a bunch of emergent identities that get dubbed gospel which depend on the US dollar being a reserve currency backed by global economic imperialism. MMT died the day the US and EU froze Russia's reserves.

The exact same thing happened with Reaganomics/Supply Side Economics. The economic brains behind these ideas was Milton Friedman, and while he did strongly and aggressively advocate for supply side economics, he also had quite a lot about to say the consumer side of things and advocate for, among other things, a negative income tax [1] that in practical terms is essentially a basic income that solves many of the major problems with things like welfare.

I'm not advocating for a basic income (or supply side economics), but simply emphasizing that what you said is completely true and one of the many risks of MMT. Even if MMT might be theoretically viable, in practice it's going to be interpreted as something not far from a pseudo-intellectual justification for arbitrary levels of debt/monetary inflation.

I also don't see the positive result to be honest. We will get high prices and high interest charges? That is only a beneficial development for a very select group of people.

So if that is the result of such a monetary theory or not, maybe it does not have beneficial goals?

Yeah, MMT basically asserts that the separation between fiscal and monetary policy is artificial, and that the only real constraint on “fiscal” policy (tax and spending) is monetary effects, not the metaphorical limited purse (“fisc”) that must be filled with revenue and borrowing to allow spending.

It is not “Congress can spend willy-nilly” but “Congress needs to stop thinking about fiscal balance and start thinking like the Fed.” (Or, perhaps, “Congress needs to define fiscal policy with movable levers which it gives control of to the Fed or a Fed-like body.”)

Irrespective of its economic merits, any policy which depends on a competent and upright Congress does not inspire confidence. It feels like it's bound to be one of those "True MMT Hasn't Ever Been Tried (TM)" things.

MMT isn't a thing to try or be tried: it's not an ideology or set of policies or even policy goals (there is a very loose correlation between adherence to MMT and certain progressive policy goals, but they aren't the same thing.)

MMT is an understanding of factual nature of the environment in which government operates. Reduced to one sentence it is “the entire concept of fiscal balance is play-acting as if the government was using commodity or externally-controlled fiat currency, rather than it's own fiat and a distraction from the real constraints on government finance, rather than something which reflects, or even loosely guides policy makers towards, the real constraints.”

Factual is class of statements, opposed to normative statements.

> MMT is an old lie

It can't be that old, since it only describes the constraints on sovereign finance of entities functioning in their own pure-fiat currencies, which isn't a subject that has been of interest for very long.

MMT is not based on facts about the world as it is, but on conjecture, ergo it is not factual.

The old lie is that sovereign entities (note the deep and old roots of that term in feudal societies) can debase their currencies with zero consequences.

Usually this works well for a long time, until all of a sudden it doesn't.

dragonwriter seems to have meant "factual" in the sense of "concerned with questions of fact", "is" rather than "ought", and was not intending to claim (at least in that statement) that the answers MMT provides are correct.

gray-area seems to have interpreted "factual" as "accurate" or "truthful", and was objecting that defining a theory as "concerned with things which are actually fr-reals true" is cheating.

To be fair to gray-area, "true" is probably much more common a use of "factual". On the other hand, the broader context was that dragonwriter raised the point in objecting to argument about what MMT purportedly says we "should" do.

MMT is not evidence based, it is in no way factual (it is neither backed by facts, nor is it concerned with facts) - it is a conjecture about what might happen in the best of all possible worlds based on abstract arguments about perfectly spherical economies in a vacuum.

Factual is entirely off base as a descriptor and has been picked here in an attempt to make it seem grounded in reality and without challenge.

I expect at this point you're actually disagreeing in some sense with what dragonwriter believes but I don't know and I won't speak for him.

My point here is not to defend MMT but the quality of the conversation.

If someone comes along and says Modern Moo-netary Theory says we should to build too many catapults, and another someone points out that the theory doesn't address questions of "should", pointing out that the theory talks about spherical cows in space doesn't rescue the original objection.

That a theory makes unrealistic assumptions is absolutely an appropriate objection to raise, but it belongs upthread. Otherwise it won't be seen by people who've already decided what they think of the narrower topic of this subthread, and we'll get more repetition of worse arguments.

There was an obvious implication that it made recommendations (in order for it to have "been tried") which I still believe is what dragonwriter was objecting to.

My objection is to people talking past each other rather than engaging (whether intentionally or unintentionally) and remains as relevant as ever.

> it's not an ideology or set of policies or even policy goals

That might be true in the academic sense.

But in reality, the only people who talk about MMT are people who just want to spend money infinitely and claim that there is no negative consequences to doing so.

Which of course, doesn't make any sense if you know anything about MMT in the academic sense, which absolutely admits that there is negative consequences to spending/money printing.

Mainstream economists don't really think MMT has much to say, TBH, and few professionals care about it.

As someone who took a lot of political science and economics classes once upon a time, and has an ongoing amateur interest in these things, MMT is the first time I've looked at one of these macro-level explanations/descriptions and not felt like I needed to ask a bunch of stupid questions that are (inevitably) going to be dismissed with a heaping dose of condescension. Finally, something that makes total sense when I look at how real world systems (and especially governments) behave.

It's less that it's simple (it doesn't really seem simpler to me than any other fundamental approaches to macro, no?) than that at least real-world behavior of governments, and changes in the world as a result of that behavior, doesn't all seem to point strongly in the direction of something about it being wrong or badly incomplete. It's simple like universal gravitation is simpler than epicycles.

Ok and the fact remains, that the vast majority of experts in the field dismiss MMT as something that doesn't provide much of value to the field.

Thats the important part here. Whatever your opinion is on any of this, basically all the actual people who know what they are talking about, disagree and think that MMT is basically valueless.

The world isn't that complicated. Its brutal and uncaring. We make up complicated systems beacuse we'd rather not face the pointless brutality of it all. Contrast the complexity of religious faith in life after death to the biological reality on the ground for the best example of this.

Similar background. MMT, for me as well, is the first comprehensive explanation of money that just fits everything and makes complete sense without any glaring holes.

All other theories feel like yeah... but how does it explain this phenomenon or that

Not-quite Fiscal Theory: the fed mints a $1 trillion dollar platinum coin and lends it to congress to allocate the year's budget. The coin may not have any value beyond spot, but everyone can see that congress has a rare piece of metal!

An issue with using fiscal policy this way is that many of the things that are worth spending money on aren't easily movable levers, they are long term projects.

If inflation is accelerating and we need to cut spending to fix things it may be difficult or inefficient to cut the budget of a 10 year infrastructure project. If we need to spend more one year, do we just flood the healthcare system or military with money temporarily?

Changing tax policy frequently creates uncertainty for people investing in long term projects, which increases risk and cost associated with funding them.

I like that there is an academic debate going on about MMT, but there are practical challenges in implementing it. While far from perfect, the current monetary policy approach is easier to implement and change, while outsourcing capital allocation decisions to the banking system.

Here are the first two paragraphs on the MMT Wikipedia article:

> Modern Monetary Theory or Modern Money Theory (MMT) is a heterodox[1] macroeconomic theory that describes currency as a public monopoly and unemployment as evidence that a currency monopolist is overly restricting the supply of the financial assets needed to pay taxes and satisfy savings desires.[2][3] MMT is opposed to the mainstream understanding of macroeconomic theory, and has been criticized by many mainstream economists.[4][5][6]

> MMT says that governments create new money by using fiscal policy and that the primary risk once the economy reaches full employment is inflation, which can be addressed by gathering taxes to reduce the spending capacity of the private sector.[7] MMT is debated with active dialogues about its theoretical integrity,[8] the implications of the policy recommendations of its proponents, and the extent to which it is actually divergent from orthodox macroeconomics.[9]

Regarding this being a "test" of MMT, I don't see why. The first part of the first sentence of that second paragraph, MMT says that governments create new money by using fiscal policy and that the primary risk once the economy reaches full employment is inflation, which seems to be precisely what has happened, no?

Unemployment < 4% is basically full employment. People that are changing jobs are temporarily unemployed. Another metric you can use to reach the same conclusion is that # of job openings > unemployed work force

How is "unemployment" defined in the US? Take those numbers with a grain of salt.

In France, you were counted as "unemployed" if you were registered with the national employment agency and actively looking for employment according to their criteria.

If you didn't find anything (for example because the opportunities on offer were too far away, or various other reasonably human reasons) after a certain time, the agency dropped you, and you were no longer part of the "unemployed" statistic. Unemployment went down!

I've also seen the government there change their criteria for unemployment (for example dropping you after 9 months instead of 12), to make it seem like unemployment went down.

(I'm a big believer in statistics-driven policies, but statistics, like anything involving humans, can be corrupted)

That's very astute of you. The GP was talking about a rate called U-3, but the U-6 rate is far more descriptive. U-3 is what is generally used as the quoted rate, because it severely minimizes actual unemployment, allowing the Federal Government to use false statistics. [1]

It's extremely meaningful. It measures those who are unemployed. U-6 counts underemployment and people not actively searching due to an "economic reason".

The US uses a large-scale survey for unemployment rather than tying it to the unemployment process. The official definition most people quote is based on responses to the survey of "have not worked recently, have looked for work recently" but there are also broader measures of unemployment that count people who want to work even if they haven't looked, as well as people working part time who want to work full time.

Using even the broadest measure of unemployment[1], numbers are back down where they were before Covid. The labor force participation rate is still down though[2] which means that about 2% of US adults aren't looking to go back to work at all- many of them are likely now retired, students, or stay-at-home parents.

That's U-3. U-6 is at 7.2%. In general the claim that many people are not returning to work after COVID lockdowns is true. The reasons are up for debate, but that's not the point. The U-3 rate is an artificial rate to claim as the truth. That's moving the goal posts in order to get the win.

Plus there are a record number of unfilled job openings.

U-6's 7.2% is compared to 7.0% in February 2020 and 8.1% in February 2007. So even that is similar to pre-Covid levels and better the the peak before the last recession.

The 5% = full employment threshold has always been calculated based on U3. That's what they measured to come up with that estimate. If you want to talk about how U6 is better, then you need to compare it to previous U6 measurements, not previous U3 measurements.

If, as you were implying, U3 was hiding extra unemployment right now but U6 was more accurate, then it wouldn't be so closely tracking U3.

For something to be a non sequitur, it must be a non sequitur to everyone, not just to one. This is not a non sequitur for two reasons.

1) The sentence you quoted was not intended to be a

consequence of the earlier statement. Unemployment rate

and number of job openings are connected, but not as you

believe. Correlation is not causation. You are drawing

inferences without cause.

2) Full employment depends upon the number of job openings as

well as the unemployment rate, which you ignored from

my comment.

> Yes, which would basically imply that it's incredibly easy for anyone who wants a job to get one.

No. That is your inference but is clearly not implied.

Inflation has many inputs and looking at inflation strictly through a monetary lens will provide a distorted picture as to why there is inflation.

Additionally, MMT states that it needs to use taxes to manage inflation, which the US federal gov't is clearly not doing, which undermines the testability of the theory.

> How do you define full employment? The unemployment rate in the USA is currently 3.8%.

3.8% is near historic lows.

More importantly: "full employment" doesn't mean unemployment is literally 0% - in fact, an unemployment rate of 0% would be actively bad, because it indicates that people are unable to leave their jobs (even temporarily) to seek better opportunities or life changes - usually because inflation is too high.

There's no strict definition, but an unemployment rate <4% almost certainly corresponds to full employment, as frictional unemployment can be expected to be ~4%.

BLS defines full employment as an economy in which the unemployment rate equals the nonaccelerating inflation rate of unemployment (NAIRU), no cyclical unemployment exists, and GDP is at its potential. [1]

MMT has seemed to me to be an academic fig leaf over the indirect taxation which occurs when more money is printed. MMT is fundamentally wrong, and everyone smart knows it is, but you as an individual can't make any sort of "respected" career as an economist unless you say the right things or are stupid enough to believe them.

Wouldn’t it also suggest that the prescribed inflation antidote - raising taxes - would be impractical due to political opposition. Seems like a double win: stand strong against raising taxes (which is the heterodox position) while showing MMT “doesn’t work”.

A few years ago, Janet Yellen (testifying in congress I believe) called for more research into "hot" economies because presumably there was a lack of such research. We're now in a period of growth and basically full employment after a pandemic where the fed and fiscal policy decided to keep things "hot." There have also been supply and energy shocks that are contributing to inflation.

The remaining part of the MMT puzzle as I see it is: raise corporate taxes, and see if it helps bring inflation under control. If raising rates slowly doesn't quite do it, this should be the next go to for policy makers.

> and that the primary risk once the economy reaches full employment is inflation, which can be addressed by gathering taxes to reduce the spending capacity of the private sector.

I don't understand this. Increasing taxes reduces the spending power of the individuals who pay the taxes. But that taxed money doesn't evaporate. The government spends it or redistributes it. It ultimately makes its way back into the private sector.

The key concept is that taxation is unrelated to the government's ability to spend (with fiat currency). They can tax $1T and spend $1T. Or they can tax $0 and spend $1T. Government is not constrained from spending whatever amount it likes—except in the spending's effects on money supply, inflation, et c.

From that POV, destroying money (or, if you prefer, reducing the rate of increase in the money supply) is exactly what taxation does.

All value is explanatory, that is, even if it has "intrinsic value" like carbohydrates in ATP in a cell, it is still knowledge instantiated for a resilient purpose (eg to power a cell to replicate its knowledge).

As explanations change, value changes, so anything can be a currency at the level of the individual--in this way, at least for conscious minds, a public monopoly on money is, while possible, morally wrong. It's a form of Marxism.

There's already been a solution the problem of state monopoly on symbolic abstractions for value (money), that started with Bitcoin and has been growing a new global economy since 2009.

What do you mean by, 'Try paying your taxes in BTC ...' ?

In USA, sales taxes are paid to government by the vendor. As just a typical person in USA who does not work for federal government nor reside in D.C., sales taxes and property taxes are all that I (implicitly) pay. The vendor and I determine amount and type of my payment.

Your comment had a threatening tone implying something bad may happen. What is the lurking threat?

Many people don't qualify to pay 'income' tax, but most people just think they have to do it. And employers withhold it from wage slave paychecks, which does make it challenging to opt out.

Definitely possible to not have what is known as wage income. Many do it. The super rich structure their affairs to avoid being in that system of voluntary contributions.

>>Conceptually the answer in the theory is to suck up the excess money with taxes

Govt spending is already 45% of GDP, so there's not much room to increase it more.

As for MMT, I think what the MMT crowd doesn't realize is that there's a lot of latent inflation coming. Asset prices and CPI do not go up in tandem. First Asset prices are inflated, then later for the next decade or so, as people slowly make withdrawals from those inflated asset prices, it begins to affect the CPI. And that's where we are right now, at the beginning of the CPI impact.

I am by no means a fan of mmt, but I think looking at government spending as a share of GDP misses the point mmt proponents attempt and often fail to make; which is that financial constraints are should not be the limiting factor of the economy.

A better indicator would be the price of labor and commodities since they better reflect the constraints of the real economy. Unfortunately for the mmt people, the prices are going nuts because we are actually dealing with real resource constraints now.

As I understand it taxes in MMT are just destruction of money, it's the essential counterpart of money creation used to balance supply. It's irrelevant to GDP and spending in that model, since in MMT the government doesn't need taxes to spend, it just print what it needs, that's the core idea.

Interestingly, the mechanics of this seem backward. A major problem with the Fed's operations is that operations on financial markets take 12-18 months to spread to the real economy, so they have to target interest rates now based on what they think the economy is going to look like in 12-18 months. Conversely, money going into or out of the average person's checking account now affects what they do in the real economy now, without a lag time. When we've recovered from significant economic crises (2008 and 2020), it's often been through direct fiscal stimulus.

It seems that the logical thing to do would be to put money into the economy through directly giving it to citizens, and then take money out of the economy through interest rates, by making it more expensive to borrow and reducing business investment. Typically you want to put money into the economy in a hurry, in response to a crisis, but you want to take it out gradually, so that businesses can plan ahead. MMT's framing of this still seems backwards, even if they've realized that fiscal and monetary policy are two sides of the same coin. You'd also get a lot less political resistance to the fiscal policy side if it involved giving people money rather taking money away from them.

I seem to recall that France used to do this -- create money for government spending, taxed money ceases to exist, no need for government debt. But I can't find anything about it, and I don't know if I'm just not using the right search terms.

Has this been put into practice in large countries before?

This points to why the EU will likely disintegrate - member countries can't print to monetize country debt. Either EU members split out to regain currency autonomy, or EU officially federalizes member country debt.

Obviously the latter will happen - it is in fact already happening, between eurobonds and recovery fund. We just don't make a big song and dance about it - quiet work is how the EU is managing to do the unthinkable of federating this anarchic and unruly continent.

The economic imbalances between EU states are nothing, compared to the ones between US states. Do you see the US "disintegrating" anytime soon?

I could see Illinois imploding due to retiree obligations and pieces of Illinois being absorbed by neighbor States. More likely for federal government to take over State pensions because federal government can emit unbacked money.

I can think of a few trillion in urgently needed money we could spend taxes on: renewable energy, batteries, retrofitting homes for chargers, resilience building (and paying people to move out of high risk areas), invest in carbon capture/moonshots.

> I never quite understood how this theory would work while avoiding inflation

I see this sentiment any time MMT is brought up. I think it shows a misunderstanding of what MMT is saying.

While I’ve got my own issues with MMT, it’s always been made clear by MMTers that inflation is an important signal to respect and that you can’t infinitely ‘print’ money due to the constraint of real resources.

You're correct, but I think the problem is that a lot of people who advocate for MMT, don't actually understand it, because many of the pro-MMT people I've talked to really do think you can print money forever.

It's not unique to MMT, the same thing happens with plenty of other subjects too.

I think people conflate what MMTers were saying post-2008, which was we had WAAAAAAAAAAAY more capacity to print money, especially from 2008-2014 or so, with we can spend literally infinite money. And so you get all of these people saying "MMT was wrong" with the pandemic inflation, when it's the exact opposite. We started running into real resource constraints (due to lockdowns, supply chain issues, etc) and inflation shot up exactly as expected. Now, even as an MMT fan, I'm perfectly willing to admit that predicting where the real constraint is is extremely hard. And that politically in the US raising taxes on a dime is basically impossible. But MMT wasn't wrong, for the parts that have been tested as much as they can be.

Where in the world would raising taxes on a dime be perfectly acceptable? Imagine you have a rent or mortgage payment, but inflation hits 10% so your taxes go up 10% month over month to counter it. Your costs were fixed, the inflation affected other things besides your long term agreements, and yet, you would default on your payments because you got 10% less that month after taxes. Who would not want to burn the whole system down after experiencing that?

> Where in the world would raising taxes on a dime be perfectly acceptable?

"Any place where..." Noted that you couldn't conjure a single example.

> If inflation is that high, the real cost of making your mortgage payment is shrinking in real dollars.

This assumes that inflation is evenly distributed in all sectors. It isn't. Your CPI inflation rate is a proxy, a rough index, an average, and a dubious one at that prone to all sorts of bad signals.

Tax rates are evenly distributed (even if a higher tax bracket results in a higher rate, it's still evenly applied across the population).

Inflation isn't. Wages don't move in lockstep with inflation, particularly across all sectors and across all jobs. It moves in fits and bouts, and a raise may only come once a quarter or once a year for many (since businesses need their expenses to be predictable).

This idea that taxes could be unpredictable based on some rough, government sponsored index of inflation is quite silly on deep inspection. It completely upends the predictability of doing business.

And the cost of that unpredictability would be a contraction in the economy from less spending to hedge against the uncertainty of income.

> everyone is working with wildly different and often contradictory definitions

I’ve found the main MMTers to be mostly consistent amongst themselves in their theories. Now, I think some ideas are wrong, but they do seem mostly on the same page. I agree MMT does an excellent job convincing laymen of some pretty wacky ideas and that’s one of my bigger complaints with it.

Also, I find the focus on mathematical models problematic in mainstream economics. It obfuscates a lot of erroneous assumptions. Models are great for testing, but words are useful for communicating ideas too and can sometimes be a better format, especially for wider audiences. To be clear, I’m not saying models are bad or that MMT shouldn’t use them, in fact I saw one MMTer post this paper recently:

http://www.levyinstitute.org/pubs/wp_992.pdf

I keep these things in the back of my mind when talking about economic theories:

- an economist is someone who can tell you today why he was wrong yesterday.

- the central bank of Sweden made up an award in the honor of Nobel. Twice the recipient made a point to remind people economic theory is not an exact science.

> an economist is someone who can tell you today why he was wrong yesterday.

Which puts them near the bottom as a hard science, but near the top of the social sciences. (I'm agreeing with you, but the valence of your observation depends on what reference class you have in mind for economics)

How is it a test? MMT doesn't say you can increase monetary supply forever without consequence. It says that you can increase monetary supply until you see consequences, at which point you need to start reducing it, mostly through taxation. Raising interest rates does reduce monetary supply, but I don't think nearly to the degree that MMT would call for.

Now, if congress immediately votes in a bunch of new taxes, it'll be a wonderful test. :D

MMT simply has currency scaling with the exponential utility of commerce. Value is created on both sides of each business transaction, not just for the recipient of the money. The money supply increases to reflect all of the new value created by commerce.

Even if we imagine MMT working perfectly — whatever that means — it represents a stealthy redistributing of wealth. The idea behind it is for the government to acquire and then redistribute goods and services from those in the private sector who would otherwise command that wealth, and do something else with it: in other words, give these goods and services to others.

And no one is going to notice this? The people who are used to enjoying some quantity of goods and services are not going to notice that they now enjoy less, because someone else is enjoying them?

Or, is this somehow supposed to "stimulate" the economy, so that more goods and services are actually produced, because of the extra money?

This is alchemy. Production comes before consumption.

Any theory of economics that only works if you can depend on an elected body to take quick and reasonable steps—like raising taxes—is one doomed to failure, and ought not be tried.

The problem is all that new wealth created, about 90% goes to the top 1% who can easily store it away in nontaxable assets (at least until said assets are sold) since generally the “buy tax” isn't all that high compared to growth in value of securities and real estate (at least good investments thereof). Just siphoning more money out of the poor and middle class will not fly in the USA you will be voted out and your policy rescinded within a couple of years.

You can expect inflation as you grow the money supply. Inflation is good. Runaway, uncontrolled inflation is not. We have not had, nor do we have now, runaway inflation. You have to grow the money supply as the population and productivity increases. Most of the talk and reporting on inflation is just silly.

"Conceptually the answer in the theory is to suck up the excess money with taxes"

Huh, why is that the answer? Why wouldn't the conceptual answer be "do the opposite", i.e. sop up the excess liquidity by removing money from the money supply, by doing things like raising interest rates, increasing bank reserve ratios, and selling some of the trillions of dollars of securities already on the Fed's balance sheet? The last thing anyone should want is the government to take a lot more in taxes so it can be squandered on foolish projects. Also, once government programs start up and build/lease buildings and hire a bunch of people, they are almost impossible to get rid of (the process of terminating a Federal employee is a Kafkaesque nightmare).

I would love more "foolish" infrastructure projects in my area. In my state/city, We are dealing with increasing flooding, overcrowded roads, and could always use more green space.

I get your sentiment, but the government could be using that money in positive ways that don't involve spinning up whole new organizations

You raise a good point that we could really reverse inflation by actually closing tax loopholes and reabsorbing the excess we printed and gave out to the 1%. . . but like you said, never going to happen unfortunately.

Most prices haven't inflated on supply constraints, they've risen on opportunism of profit margin increases by companies who were allowed to merge and grow with insufficient anti-monopoly regulation.

If we haven't devalued our USD currency against the EUR because we printed while they also printed, is there a currency that we did devalue ourselves against (or a country that didn't devalue their own currency through printing?)

Does printing always actually equate to devaluation?

This didn't happen in a vacuum, though. It was simultaneous (and, obviously, co-causal) with a very rapid economic contraction and a subsequent supply shock across a ton of industries. Any analysis of this situation that starts end ends with "the government printed money" is, IMHO, basically pushing an agenda.

What actually happened is that the device under control (the economy) had an excursion (picture a car blowing a tire and veering) and the government corrected rapidly (prevented it from entering another travel lane, say), but it was something of an overcorrection (the car ran off the shoulder).

Should we have "printed less money"? Probably yes, in hindsight. Was the alternative worse? Of course it was; we were looking at a huge jump in poverty. Was anyone unaware of the inflation risk? No, not really. Was anyone dead-on correct about the right amount of stimulus? Not that I can see.

I would encourage readers to also review this [1] document which compares and contrasts MMT and other economic theories. The author concluded that "MMT contains some kernels of truth, but its most novel policy prescriptions do not follow cogently from its premises. "

I haven’t studied MMT enough to be able to comment on it beyond a surface level, and the economists behind are smart, accomplished people. What I do know is that in the real world of policy, MMT will just be used as an excuse to spend limitless amounts of money by politicians that also don’t understand it.

the only long term sustainable economy is one that has a sound money where natural supply/demand laws govern it, not a central and politically motivated agenda where money can just poof be made from nowhere, people are falible and complex systems are impossible to control. Ultimately mmt is like relying on weathermen to be 100% on point. Mmt is just a boom bust cycle where debt is kicked down the road and the bubbles grow larger with a false sense of security.

MMT has all the same problems as Communism: nice in theory, but terrible in practice.

MMT proponents will argue that no one has ever properly implemented it.

However, an economic theory that is not effective in practice, given the realistic constraints of human nature and politics, is useless.

In theory the only way MMT works is to arbitrarily raise taxes to counter inflation. The Fed does not have the power to raise taxes, Congress does. But such a floating, variable tax rate is ripe for abuse of power and I don't know anyone who would not revolt under such a system.

It's like the anthropic principle in physics IMO in that it can be taken either descriptively or prescriptively, and while the former is almost trivial in what it describes, the latter invariably ends up leading to significant consequences far beyond the initial description.

The alternative is a static or deflationary currency. This leads to hoarding of assets which were originally intended to serve and increase commerce. Think Bitcoin. Without MMT, we would be falling from a skyscraper as you depict.

Bitcoin isn't static or deflationary. There is a schedule of inflation built in via the mining reward which is currently at 1.5% until the next "halvening" where it will become 0.75%. The mining reward will continue to half every 4 years until roughly near the year 2140.

You realize 2140 isn't that far away and that the cap is what is inflating current values (and coin hoarding) right? Just ask investors and they will tell you.

' deflationary currency ... leads to hoarding of assets '.

Someone owns every asset. By making it impractical to save using the fiat money, savings goes to non-fiat items like land, stocks, energy, and BTC. This harms the poor who are rarely able to escape into those non-money items.

It seems interest rates lower during recessions. Right now we are already low and are raising which seems to be a different pattern. Is lowering interest rates a method to overcome a recession?

Lowering interest rates makes capital cheaper, which does spur investment and thus economic development, so, it can certainly have that effect given the right circumstances. But keep it too low, too long, and you see money start flying around too quickly, getting a little too loose because everyone wants to get theirs, and then they start inventing things like mortgage-backed securities and everyone starts over-leveraging, because, why not, money is cheap! Then you get 2008.

It's important to separate out fraud from low interest rates. Low rates absolutely drive investment, and riskier investment at that. But the issue with 2008 was fraud in the lending market, not necessarily the low rates.

Risky investments aren't necessarily bad investments. Low interest rates give businesses more runway to operate investments that might take a while to show returns. A million dollar loan at 10% for an investment means that it needs to return into ~$80k a month to break even. At 2%, that same investment only needs a ~$16k monthly return. That's a huge difference in runway needed to start generating cash flow.

It makes for a good news story that regular Americans understand and frankly want to hear (the banks were bad). But if you really dig into the reports, e.g. Financial Crisis Inquiry Report, almost the only fraud comes from misreporting of income which is essentially consumers lying. There could be other documentation issues, but underwriting almost entirely depends on credit score + income, so they're fairly trivial.

"Money is cheap" yes, also "you can buy a house if you can fog a mirror". (Buy as in acquire a piece of paper that says you'll pay $$$$ per month to whoever holds the note.)

Yes, fortunately we've learned from that mistake and I don't think are repeating that this time around. People really are qualified to buy these days, and there just isn't enough supply of housing to go around.

> Lowering interest rates makes capital cheaper, which does spur investment and thus economic development

There are diminishing marginal returns to this, and when rates were already close to zero it is hard to imagine going to zero spurred much more than meme stocks and YOLO gambles.

Correct. It is surely a non-linear function, but the statement "lowering interest rates makes capital cheaper" is generally true, and used as an economic lever in monetary policy.

>> Is lowering interest rates a method to overcome a recession?

It is claimed to be. The idea is that with lower interest rate, companies and people will be more likely to borrow money to spend and that will boost the economy.

I for one do not really believe this to be true. I suspect it's the act of lowering rates that gives a temporary boost until things rebalance. In other words, economic activity has some dependence on the derivative of interest rates. This is why things were so good from 198x through 2003 or so, rates were dropping the entire time (filtered of course).

> economic activity has some dependence on the derivative of interest rates

If interest rates go down, it's easy to roll over old promises and make new ones besides. If interest rates go up, promises must be kept or the business will fold.

At the end of every business cycle, interest rates are low and there are lots of unprofitable "zombie companies" that operate by simply rolling over their promises. In order for the economy to grow, interest rates must be hiked to do a controlled burn and remove this underbrush. Zombie companies have to actually die. This is painful at the best of times.

Political will formation will be doubly hard this time around because A. there is more national debt (so we probably need to soft-default on it and inflate it down, first) and B. last time around Carter did the burn and Reagan got the growth and the credit, so the question is who wants to be Carter this time around.

>> last time around Carter did the burn and Reagan got the growth and the credit, so the question is who wants to be Carter this time around.

You are only the second person to tell me this story. I'm not doubting it, the first guy said it to me over 15 years ago right before the bust as he was buying 6 percent treasuries.

Probably the right time to do it would have been around 2000, the last time the government ran a surplus (last years of Clinton, first year of Bush jr.) but instead we heard: There's a surplus, we don't know why, but we don't think it will go away, so here have some money, and lets spend like crazy and have a war.

This isn't a rate-hike recession, it's stimulus withdrawal.

Rates are at 0.25%. Last time it took 20.00% to stop inflation. We haven't even started. We haven't soft-defaulted on the national debt, so we can't even think about starting. The Ukraine conflict will be dusty history by the time actual rate hikes and an actual rate hike recession come around.

I also personally think that high inflation is treated as bad axiomatically. This needs some justification if the only proposed solution is to intentionally cause a recession.

The system will seize up and collapse with anything close 20% interest rates. Look at what happened in September 2019. The rates shot back to 0 because there was a liquidity problem in the repo market. The system is rife with zombie companies servicing their debt with nearly free debt. This will not go like the 70s. When rates stop increasing and go back to zero within the next two years remember this comment

If rates stop increasing and inflation continues with barely a pause, then what happens? We have massive social instability? Retirees are screwed? Lenders will have to increase rates just to earn a real return.

The 1979-1982 interest rate spike was preceded by 15 years of faffing around, playing at raising interest rates, and then chickening out, with a backdrop of rising persistent inflation. I think it's likely to play out exactly as you describe, but that's exactly how it played out in the 70s.

I'm much less certain that it will end the same way, but there are big problems with all the alternatives too (yuan, euro, crypto, gold) so who knows.

Except it wasn't. Inflation was already high and going up by the time the first oil crisis hit. CPI was 5.5% in 1969, 5.8% in 1970, went down to 3.3% by 1972, and was 6.2% in 1973:

The biggest jump was 1.81% in August, 2 months before the oil shock. (Note that this is roughly double the monthly numbers we see now.) There was consistent monthly inflation 0.68%+ from January -> June.

The real reason for the 1970s inflation was Nixon monetizing the debt incurred by our Vietnam hangover, but in true Nixonian fashion, he found an external event to blame it on.

I think what you're describing is exactly what's claimed. /Lowering/ interest rates leads to growth, not low interest rates. I don't think many economists would dispute that.

The general model is that interest rates, lowering taxes, and increasing government spending are tools for shoring up the economy during a recession. During a growth period, interest rates should be raised, government spending lowered, and taxes raised, so we have room to adjust them for the next recession. This can, in theory, smooth out the boom-bust cycle which otherwise naturally results.

The problem is that we rarely raise interest rates, reduce spending, or raise taxes, since it's politically unpopular. Many of these tools are harmful; for example, outside a few domains like infrastructure and medicine, long-term high government spending tends to /harm/ the economy.

> The problem is that we rarely raise interest rates

Not really true; there was a long period of near-zero rates not moving during and after the Great Recession, but that was a unique event; from 2015-2018 there was a fairly consistent notching up of rates typical of an expansion with inflationary signals, then an ease back from 2019 until COVID hit at rates were cut sharply.

Looking at history there's a long run up in 2003-2006 after the 2001 recession, a run up 1992-2001 through the dotcom boom after the short period of easing from 1989-1992, a runup from 1986-1989, etc.

Throughout these time periods there was a dramatic increase in the money supply (from my view of FRED stats it doesn’t look like there’s ever been a contraction of the monetary supply), so we’re rate increases just offset by enough monetary growth to offset?

> Throughout these time periods there was a dramatic increase in the money supply

well, yeah, a hot economy means that borrowing even at high interest is attractive, which is why you are trying to constrain lending (money creation) with higher interest in the first place to prevent inflation.

>> I think what you're describing is exactly what's claimed. /Lowering/ interest rates leads to growth, not low interest rates. I don't think many economists would dispute that.

No, they treat is as if the steady state economy will be larger at a given lower rate. For example GDP = X+Y+Z + K/rate. What I'm saying is that GDP = X+Y+Z + K/rate' which is not sustainable at all and means existing policy is not at all the right way to handle it. Actually there may be some degree of truth and both terms should be present in the equation, but nobody talks or acts like the derivative term exists.

Yes, lowering interest rates during tough times has the effect of making borrowing capital cheaper, thus incentivizing people to take on risk via opening a business, investing, etc...

In contrast, raising interest rates is a way to fight a hot economic market. While in theory having massive growth might be ideal, it would be the equivalent of a sprinter using all of his/her energy in the first 100m while running a marathon...it needs to be a balancing act.

Lowering interest rates has been one of the major tools in fighting recessions, and one of the main concerns has been that lowering interest rates isn't possible(or effective) when they are already at such a low level.

The thinking is that lowering rates will increases spending (why save if you aren't getting much of return, you will find other ways to invest your money rather than have it sit in a bank account). So, if the economy seems to be in a recession central banks will often lower rates to encourage spending. But if you are already at near 0% for a record length of time, and have printed massive amounts of money, well friend we are in uncharted territory. What's better than do nothing? Doing something, we have this interstate rate lever, we can't pull it down, lets push it up!

It's being pushed up because we are not in a recession. We aren't even close to being in a recession. We need it to be raised in times like this so we actually have room to move it should things go south.

"It seems interest rates lower during recessions. Right now we are already low and are raising which seems to be a different pattern. Is lowering interest rates a method to overcome a recession?"

It used to be that you could lower interest rates and run up deficits during bad times with the intent of going back to normal when things are better. We now have kept low interest rates and record deficits during good times. When things blow up (as they always do after a while) there is almost nothing left that can be done to counter a recession. In the past going to war helped....

Yes, the common theory is that lowering interest rates encourages investment and growth, at the cost of higher inflation. This increased inflation is also generally thought to depress 'real' salaries, which further increases growth.

The last couple of recessions have placed a ton of deflationary pressure on the USD, and the fed has reacted to maintain a small positive inflation by both lowering interest rates and QE.

Now that inflation is rising and the economy is also at nearly full employment, its pretty straightforward for them to raise interest rates to rein in inflation.

Lowering interest rate to stimulate economy, increasing interest rate to lower inflation. Problem is we've got no room left to lower and asset prices have never been higher.

Yes, because it increases the money supply. We are supposed to tighten when things are good by raising rates. At this point they need to raise rates to pull money out of the system. Because with covid, not only did we cut rates, we put in a HUGE amount of money and that was really irresponsible. And now we are seeing the repercussions with inflation lowering the value of the dollar.

We should recall that not only did the US cut rates and spend a lot of money through the covid recession, when things were bad, it ignored that first bit of advice before Covid when things were good (it's hard to remember now how hot the economy was in 2016-2019, but it was really hot), by cutting taxes and continuing to print money and keep the rates low to cover it. As the tax cut detractors correctly predicted, those tax cuts (and the growth that didn't happen enough to cover them) reduced the US's leverage to respond when an actual crisis came up.

a) higher taxes enable the government to apply deflationary pressure on the economy (by removing currency from circulation)

b) Reducing taxes without cutting spending (because it will "pay for itself in growth") leads to a larger deficit, which requires increased debt to cover, which triggers the money-printers.

Your first point is only valid if the government doesn’t spend that money or uses it to pay down debt, a dubious assumption with the US federal government.

Your second point is wrong: you can continue to run deficits without printing money. You just have to find lenders in the marketplace willing to buy your bonds.

Yes, the Federal Reserve is buying vast quantities of US treasuries right now, effectively monetizing the debt, but the sequence of events you describe isn’t typically how things work.

Wasn’t that during Yellen’s term who was replaced by Powell in 2018? The same year the tax cuts went into effect. The following year the rate cuts started and then Covid hit.

I am not sure if it is really useful to evaluate what happened vs the other outcomes that we were not able to experience. We don't really even have that many precedents for the situation. It was, and still is, an extremely complex problem to address. Injecting large amounts into the system ultimately doesn't create long term wealth, but in that short term gap during the first 1 of the pandemic many people were undoubtedly pulled out of a hole.

We are not yet in stagflation, unless I really missed something. The economy is actually fairly strong by most indicators. The question is whether inflation can be tamed by the time we hit a recession(which we will, whether it is in 6 months, 2 years, 5 years, etc...)

These 6-12 month predictions for the next recession are always real popular 6-12 months before the next major election. I recall almost identical rhetoric in H1 2018, coincidentally the last time the fed raised interest rates.

Nobody has a clue when the next recession will be.

It's important to note that the Federal reserve normally controls the overnight rate, and let the market determines the interest rate for other durations (eg. 30Y). That changed with the introduction of Quantitative Easing where it reduces the interest rate over the entire yield curve.

In other words, even through the overnight rate is 0%, you could still push down the interest rate down for bonds of a longer maturity, and that'll further stimulate the economy.

We did waste the 3 yrs before Covid hit by not increasing interest rates and not reducing Fed's money printing. I don't know if it's the fed or if the government pushing to win elections, but feels like we didn't take care of the house in good times and we have led ourselves into this cycle.

Because Powell cares more about markets than the real economy or wealth inequality. Also they tend to care much more about the short term than the long term.

People will tell you that it's not in the Feds mandate to care about those things, and they don't actually care about markets, but it's clearly not true when cast in the light of their actions. Or to any rational observer that follows them closely.

Even in Powell's presser today he spent a lot of time talking about being sensitive to markets. Why didn't they raise rates in the entire year while inflation was increasing and the labor market already showed signs of overheating? That one's easy too. Because Powell's nomination was coming up and he wanted to maintain easy policy to boost his chances to get reappointed.

Why did they continue QE policy of buying assets to drive down interest rates while inflation was over 7%? Because he knew if he ended it abruptly it would cause a market selloff.

He cares about the real economy to the extent that their policy doesn't significantly impair asset pricing.

sad but true. The only thing that Jpow cares about is the markets. In his defence the economy is made of people and crashing the market/causing recession is going to cause more grief to the public that is already overwhelmed with covid.

Slowing down GDP growth or the stock market would have been political suicide. It would probably have been a good thing in the long-term but long-term planning is not feasible anymore in the current climate. Sadly it's a winning strategy to inflate bubbles.

IIRC the fed tried a few times to tighten and the market reacted badly(i.e. taper tantrum). Rather than focus on economic health, Powell chose to support asset prices owned by the upper half of Americans(and, by a huge majority, the 1%).

That sort of makes sense given Powell was a Trump appointee and Trump favored a weak dollar in order to boost American manufacturing.

Yeah no doubt about this. But its also important to remember we've been doing this non stop since 2008 minus a few months in 2018. So this is a multi president, both parties are involved in continuing this train.

People have been conditioned to believe it's either one or the other party's fault. And they decide whether things are going well or not so well based on whether their favorite president is in power. Nobody looks at the actual data.

It's not as dramatic as that looks. They changed the definition of M1.

From the same link:

Before May 2020, M1 consists of (1) currency outside the U.S. Treasury, Federal Reserve Banks, and the vaults of depository institutions; (2) demand deposits at commercial banks (excluding those amounts held by depository institutions, the U.S. government, and foreign banks and official institutions) less cash items in the process of collection and Federal Reserve float; and (3) other checkable deposits (OCDs), consisting of negotiable order of withdrawal, or NOW, and automatic transfer service, or ATS, accounts at depository institutions, share draft accounts at credit unions, and demand deposits at thrift institutions.

Beginning May 2020, M1 consists of (1) currency outside the U.S. Treasury, Federal Reserve Banks, and the vaults of depository institutions; (2) demand deposits at commercial banks (excluding those amounts held by depository institutions, the U.S. government, and foreign banks and official institutions) less cash items in the process of collection and Federal Reserve float; and (3) other liquid deposits, consisting of OCDs and savings deposits (including money market deposit accounts). Seasonally adjusted M1 is constructed by summing currency, demand deposits, and OCDs (before May 2020) or other liquid deposits (beginning May 2020), each seasonally adjusted separately.

m1 graph is incredibly misleading because they changed the definition, and even before it was still quite limited. Here's the real money supply https://fred.stlouisfed.org/series/WM2NS

*Printing money, but in response to covid stagnation in 2020.

Printing and interest rates are separate. There was still a missed opportunity to increase interest rates while the economy was running hot prior to 2020.

It has been increasing since 2008, without Covid the same graph would look very different. Its just that the fed just increased the scale so much that the previous level seems puny now, even though the y axis is 1000s of Billions of dollars.

Not only that they increased the rate, but also they'll reduce the buying of securities:

"In addition, the Committee expects to begin reducing its holdings of Treasury securities and agency debt and agency mortgage-backed securities at a coming meeting."

IIRC they have already stopped purchasing them as of a week ago I think, they were supposed to announce their plans on quantitative tightening (selling the things they bought) which is what that quote is referring to.

> they have already stopped purchasing them as of a week ago

To clarify, they are still purchasing securities, but at a rate that does not increase the size of their balance sheet. As debt matures, they reinvest the principle in new securities to maintain the size of the balance sheet. When the Fed discusses QT right now, they’re talking about reducing these purchases, so the net impact is a smaller balance sheet.