70s through 90s wiped the blue collar middle class off the map, there are no other options outside of non-MD healthcare work if you want income that even begins to keep up with inflation. Its gigs and part-time work from there.

Edit: to be clear, I'm agreeing and saying people definitely had time to see the writing on the wall

I saw a lot of people in the trades barely scraping by 5-7 years ago when housing was bottoming out. Housing stock is growing at something like 3x population growth in the US right now. A few more years of that and they may be back in the same situation. Being employed in a heavily cyclical industry definitely has rich years, but it's also got lean ones.

However the housing stock grows, the remaining stock needs maintenance anyway.

So, well, indeed, a good plumber should not see extremely lean years.

(Anecdotally, my son works as a building systems maintenance engineer, without a college diploma. Of course the market for such jobs ebbs and flows, but seems to never dry up: city buildings still need their elevators, HVAC, fire alarm, access control, etc systems working, no matter what.)

Housing starts are at ~1.7MM units/year right now, that's enough for about 4.5MM people at current household sizes. US population growth was 1.6M in 2019 and <1MM in 2020. Even with generous estimates on losses of existing housing, I don't think 3x is appreciably off.

Maybe it has something to do with the fact that more than half of the younger generation are currently living with parents [1]. Not because they necessarily enjoy it, but because they can't afford their own home.

Building more housing should lower the effective price of it, and allow many new home buyers or renters to enter the market.

A lot of the construction boom is probably attributable to the new found geographic freedom COVID gave, coupled with the low interest rates from the Fed's monetary policy. There was a sudden mismatch of locale supply and demand. Housing starts were also quite low over much of the last decade, definitely below the equilibration point for 2019-2013.

It'll be interesting to see how things play out. I think the shift of older millennials out of cities combined with the relatively smaller generation replacing them will likely cause a reversal of a lot of the urban price growth in the past decade in places like New York. Rents are already reflecting that, but sales prices have more hysteresis.

I've read since 2008 LA has added 5 jobs for every new unit of housing. I'm sure other places in CA must be just as bad with how they've been building for the past decade. It feels like we are so far in the hole in many cities, I'm not sure how much overbuilding it would take to right the ship and make housing affordable to the median wage earner again.

When GP said business owners I assume they included independent plumbers. I can call the local plumbing franchise and I will pay $150/hr, but the person who shows up at my door is not making anywhere near that.

My friend works for a home security company. They bill $150/hr for labor and he makes $26/hr.

Compared to other countries, Australia is an outlier for tradesmen income, by far. The closest comparison I can think of is software engineer income in the US vs everywhere else.

Working in a trade in Australia is lucrative AF, if you're looking for a way to be relatively wealthy only a couple of years out of high school, apprentice as a shipwright, elevator technician or HVAC technician.

That may not be a lot of money wherever you live, but a married couple both making close to that are borderline rich where I live. A single person making that is above middle class. Of course a nice house can also be had for $150k.

And yeah, my carpenter got his HVAC, electrician, and plumbing licenses in prison and now runs his own business with family members and makes a lot more than I do, but it wasn't by luck or fortune. Anyone could have done what he did (skipping the prison part), if they didn't mind working hard.

That's not a lot of money, period, considering the hours and the inflation due to overtime. Consider too that that is the median - many are making far below that.

Most people making money in trades make most of it working more than 40 hours a week, or, like you said, runs his own business (which is completely different. That is no longer a "carpenter" plying his trade.)

> Anyone could have done what he did (skipping the prison part), if they didn't mind working hard.

This is just not true and stated as fact. There is no evidence of this. We have no idea how capable this man really is. I know lots of dumb tradesmen and lots of brilliant ones. He should be proud of what he's done because it isn't as easy as you say.

Overall that doesn't make much difference. The bottom decile of business owners makes much less and the top decile makes much more. The majority in the middle makes about the same as they would if they were an employee.

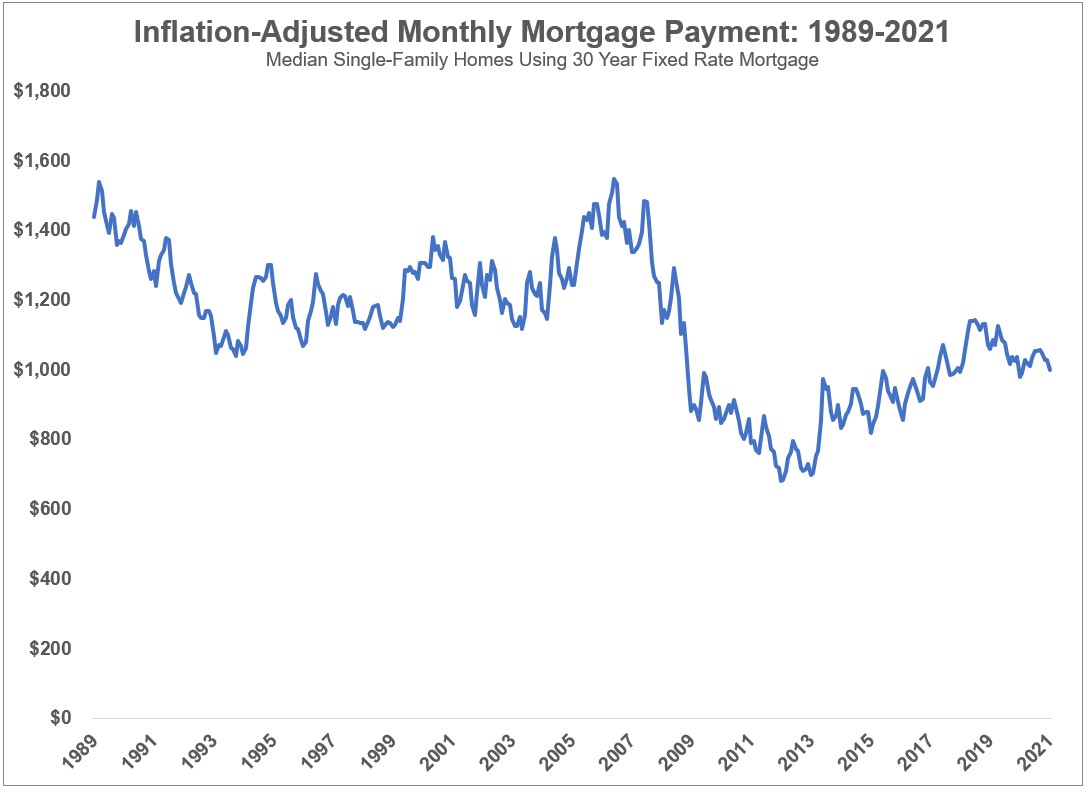

Part of that change is artificial. Mortgage interest rates have plummeted, which have caused prices to go up. The real median mortgage payment is about the same over the last 50 years.

This, unfortunately, also implies an explosion of interest rate risk. Given a fixed monthly payment, I'd much rather be paying it at high rates that have a good chance of dropping, than at low rates that have a good chance at rising.

Edit: Thank you, Americans, for your perspective! I understand now that you have fixed rate mortgages there. That's, for better or worse, not the case in Canada!

Ah, my perspective is coming from Canada where every mortgage is variable rate. ("Fixed rate" mortgages are only locked in for five years).

One would think that would cause US real estate to appreciate much faster than Canada when rates are low, but the opposite is the case. Strange days indeed.

* In Canada you technically can get a 25 year fixed mortgage, but the interest rate is 8.75%. That's a massive premium and I've never heard of anyone doing that.

If you want your monthly payments to be low initially, and you intend to pay off the mortgage debt fully within 5 or 7 years, then a 5/1 or 7/1 ARM can be a good option.

I don't understand this allergy towards debt. Oh no, people had the option to take out a loan to access capital they wanted to invest in themselves. If only we could be like the Europeans instead and waste public money to fund whatever stupid whimsy someone fancied rather than make them responsible for the productivity of their choice.

>70s through 90s wiped the blue collar middle class off the map, there are no other options outside of non-MD healthcare work if you want income that even begins to keep up with inflation.

Is it? According to the CRS[1], real wage (ie. inflation adjusted) growth is up 6.5% even for the bottom percentile.

Ah, my information was bad. The study you originally cited specifically mentions CPI-U as the measure they were using.

I assure you I wasn't lying, and thank you for the correction. (perhaps consider not jumping straight to the lying accusation in the future).

There's still a conversation about housing taking up an increasing share of the pie that doesn't exactly shine through in that top line number, but no point in belaboring it.

> Ah, my information was bad. The study you originally cited specifically mentions CPI-U as the measure they were using.

well the BLS publishes a bunch of CPI numbers, but "the" CPI is just CPI-U. The others are even more specific (eg. CPI-W for clerical workers or CPI for the elderly)

>There's still a conversation about housing taking up an increasing share of the pie that doesn't exactly shine through in that top line number, but no point in belaboring it.

The rise in housing prices has mostly been canceled out (or caused by?) low interest rates. After you adjust for interest rate and inflation, the monthly payment for a house (ie. the price you actually pay) has actually gone down from the 90s.

> The rise in housing prices has mostly been canceled out (or caused by?) low interest rates. After you adjust for interest rate and inflation, the monthly payment for a house (ie. the price you actually pay) has actually gone down from the 90s.

Only if you ignore the tax side of things, housing interest payments are deductible where principal payments aren’t. That ends up having a huge impact when inflation and interest rates drop. It’s not uncommon for mortgages to be less affordable over time. A bump in interest rates without could really mess things up.

> That ends up having a huge impact when inflation and interest rates drop.

How so? The chart in question is for 30 year fixed rate mortgages. You're going to be making the same payment every month regardless of what direction interest rates move.

The mortgage income tax deduction means paying interest comes at a discount, paying principal doesn’t so the effective nominal payment increases over time. However, when inflation is high after 10 years the mortgage becomes trivial to pay. That dramatically increases housing affordability over a lifetime. Making a stretch purchase becomes reasonable, but if inflation is very low making the same nominal payment becomes less affordable every month.

Worse insurance and property taxes are indexed to value and don’t care about inflation. Further people can’t make the same down payment when property values increase. Identical down payments at different interest rates don’t lower monthly payments equally, and at ultra low interest rates their not even a good investment.

Housing is not included in the CPI. The housing figure is Owner's Equivalent Rent. They survey owners and ask them what they think that they could rent their home for.

They do include actual rent costs, but the weighting for rent costs has 1/3 of the weighting of Owner's Equivalent Rent. The CPI-U provides an tiny weighting of rent compared to the real rent costs for anyone who is actually renting.

I'm not sure what report your read, but that report very clearly states the following:

> Real wages fell for workers with lower levels of educational attainment and rose for highly educated workers. Wages for workers with a high school

diploma or less education declined in real terms at the top, middle, and bottom of the wage distribution, whereas wages rose for workers with at least a college degree.

And that is before you start looking at issues with the CPI-U and how it's price weighting compares to real expenses faced by blue collar workers.

Dont you know that equality is a critical aspects of social satisifaction. See everywhere, equality is mentioned as the magic word that described the sacred value of liberal society...

But

It's never applied to personal wealth...

Your thinking is precisely the ludicrous disconnection between the elites' idea of society and the reality... (I am not saying you are elite, just that elitism thinking is so blindly superficial...)

BTW, equality in personal wealth is emphasized nearly 2000 years ago by Confucious 不患寡而患不均.

How is this relevant? The parent poster made a testable statement ("there are no other options outside of non-MD healthcare work if you want income that even begins to keep up with inflation"), and I disproved it by pointing out that even the bottom 10% of Americans are keeping up with inflation and then some.

Software engineering isn’t blue collar work. “A blue-collar worker is a working class person who performs manual labor. Blue-collar work may involve skilled or unskilled labor.” https://en.wikipedia.org/wiki/Blue-collar_worker

Plumber or nurse sure, but staring at a screen or moving Post-it notes isn’t physical labor.

While wrenching on a car is indeed manual labor I feel like it can take similar levels of mental effort, background knowledge, and training as junior dev work. So the parallel isn’t entirely off base. I believe the OP’s argument is that there are new classes of work that didn’t exist back then. Perhaps they’re not as cleanly sorted into white and blue collar lines as before but they occupy similar places in the socio-economic status positioning.

Being a mechanic is extremely repetitive. Occasionally people are faced with something odd, but it’s mostly a checklist job because identical makes and models generally run into the same issues.

Or as a childhood friend out it. It’s boring, but I can zone out and work with my hands.

Where is cost of living in this analysis? In the Midwest you can still have a nice quality of life with any decent job. Yeah sure, you can’t have such things in SF, NY or LA like maybe you could in the 70s.

There is no such thing as a free lunch and so reduced real estate costs bring with it an environment of potential poor local governance, poor job market, neighbors that do not share values that are conducive with rising home prices.

A most recent example is poor compliance with things that benefit the masses (ie. Vaccine, mask etc.)

I suspect the next thing will be poor compliance with switching over to energy efficient power generation as the world moves to clean energy + things implemented to discourage clean transportation (ie. extra taxes on EVs/banning solar installs without major caveats). All these boneheaded things drive down the cost of the real estate to its true market value.

{kind=link}

Edit: to be clear, I'm agreeing and saying people definitely had time to see the writing on the wall