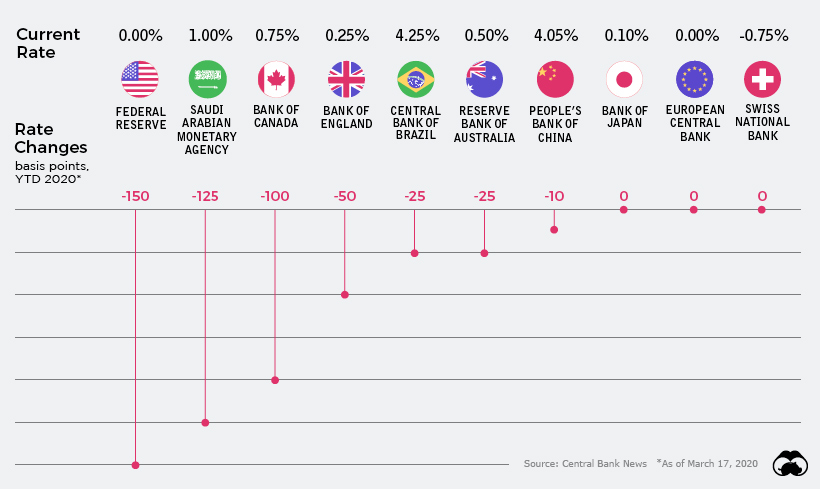

I don't see the need to plan for inflation until a future point arrives that demonstrates there might be inflation. Looking at evidence from developed countries and their central banks, they are unable to generate an appreciable amount of inflation from monetary policy (significant quantitive easing operations). Maybe generous fiscal policy causes it (UBI, "helicopter money", and the like), it just seems a bit disingenuous to argue what we'll do about a hurdle that seems unlikely to present itself (many developed country central banks are near zero, at zero [ZIPR], or below zero interest rates [NIRP] [1] [2] and you're still not generating inflation [3] so ¯\_(ツ)_/¯).

Spain is experimenting with something not quite UBI [4] (but close enough for this comment I will refer to it as such), and their inflation rate is currently negative [5]. Something to follow.

EDIT: jcranmer said it better in a sibling comment ("To me, it seems a case of economists clinging to models that predict the opposite of reality, and it contributes to my general impression that economists prefer mathematical models even if their correlation to reality is poor.") [6].

> Looking at evidence from developed countries and their central banks, they are unable to generate an appreciable amount of inflation from monetary policy (significant quantitive easing operations)

Since QE operations were not designed to produce inflation (and were arguably designed specifically to not produce consumer price inflation), this isn't exactly surprising. They did, however, affect prices of the assets the government bought up as predicted.

Suffice to say, there's a massive difference between monetary expansions in a time of deep recession - economic policy orthodoxy since Keynes - and the assumption that inflation isn't a thing in developed countries.

It's much the same as a startup can pay for stuff by emitting more equity: pay for the right stuff and the value of the company might actually rise and there are many examples of valuations leaping afterwards, but you can't just assume these examples and the infinite divisibility of the cap table means no startup needs to worry about dilution or impact on future valuations.

> Spain is experimenting with something not quite UBI [4] (but close enough for this comment I will refer to it as such), and their inflation rate is currently negative [5]. Something to follow.

Spain reforming its benefits system to create a new payout to 5% off its population to be funded by debt and taxes isn't remotely similar to Spain reforming its benefits system to pay its entire population newly printed money, so the fact the former has little immediately evident inflationary impact in the middle of Covid tells us very little about the latter.

{kind=link}