Since 2009, it has brought in more than $12 billion from individuals.

Friendly reminder that IRS enforcement is one of the most cost-effective activities that the federal government can engage in, and that Congress has consistently cut funding for the IRS for years and years [0][1][2][3][4]:

Cutting the IRS budget didn’t make sense to [John Koskinen]. It was one of the few areas of government that had a positive return on investment. Koskinen told the Senate, “I don’t know any organization in my 20 years of experience in the private sector that has said, ‘I think I’ll take my revenue operation and starve it for funds.’”

It should be obvious that a politician who votes to cut IRS funding, especially when that funding can go toward enforcement, does not represent the interests of the common people they represent.

If you are a white-collar employee making $100k, $200k, or even higher, you should be especially concerned, since you bear a large portion of the nation's tax burden and expect that your tax money be spent well. 25% marginal tax rate is a bitter pill to swallow when you know that others are not paying their fair share.

At the same time, I've been radicalized by seeing how much effort the IRS put into going after me for $1200 they couldn't even prove I owed from a year I was bussing tables for one summer.

The IRS needs to prioritize its resources by going after the big fish, not obsess over kids waiting tables. A bigger IRS doesn't change the fact that it's apparently toothless against the rich and has nfi how to allocate its resources.

My attempt at optimism: going through a downsize cycle is perhaps good to compel healthy internal reorganization inside systems (biological, business, etc) that can prepare it better for a future expansion cycle.

It used to work that way but the IRS no longer prioritizes the highest earners because they can't afford to. They've been underfunded for years and auditing high earners is very expensive and often involves long legal battles which they don't have the resources to fight.

Audit rates of people making $1m or more are down by 80% since 2011. Now "the top 1% of taxpayers by income were audited at a rate of 1.56%. EITC recipients, who typically have annual income under $20,000, were audited at 1.41%."

There is an aspect of seeming illogic I want to call out here. Maybe it's just my lack of understanding.

Assuming the IRS is underfunded, saying they focus on low income people as a consequence, when it would be more lucrative to target high earners, makes no sense. The claims could all be true, but they don't appear to be connected.

Why would the total amount of funding force the IRS to spend less on individual cases? An alternative hypothesis might be that it actually is more cost effective to target people with less money, for instance, people paid mainly in cash tips, but I don't have any idea if that is plausible, I'm just saying the narrative doesn't make sense to me.

In general, targeting rich people seems obvious because rich people "have the money", but mathematically, it depends on how many there are when you multiply it out.

Anyway, I am very open to the idea that the IRS is being stupid and counterproductive, or politically avoiding prosecuting the rich, but I think it raises the question of "why" that is not answered by saying "underfunding". They still have funding to go after one or more high earners, right, so the total amount is irrelevant if it's taken as a given.

The article linked in the parent comment explains it. Audits of lower income people are largely automated - a letter is generated and sent in the mail. Auditing higher income people takes paid investigators, lawyers and time. They are both considered "audits", but its not the same procedure.

By this logic, they should be focusing on higher income people if audits of lower income people are automated and therefore require drastically less manpower.

The cost of sending the letters is a lot less than bringing a lawyer into court. Low income individuals just pay up. If it costs pennies to send and you make $100, you’re going to keep optimizing that. If you lack the funding to take down a hedge fund manager, you’re not going to bother trying.

The IRS also sends the letters to people that they owe money. This year my accountant didn’t realize I was owed a credit. The IRS mailed me a check and a letter explaining why they adjusted my return and issued the credit.

Systemically, threatening letters, while practically free for the government to send - cause a lot of stress for people. Both those who owe tax and those who have to prove they don't.

It's hard to know where to draw the line but you could reasonably argue that chasing low income people for small amounts is net negative societal utility, even when you get them to pay up.

I completely agree. I was pretty terrified until I opened the letter and saw a check. I assumed it was an audit.

The thing that is often ignored, unknown, or forgotten, is that it doesn’t have to work this way. Some countries send you an end of year report on how much they collected from you and you can audit them as well. It’s less laborious than our system. I am blissfully unaware of the complications of such a system but I’d like to think that it works better. I’d like to think the people of the IRS would prefer that too.

The problem with this approach is that if you actually have income they don't see they've basically told you they don't know about it and aren't likely to catch you if you don't tell them.

No wonder there is an increasing income inequality of the middle-class and below when they can't catch a break while the rich are mostly left unimpeded with tax evasion.

'Cost effectiveness' doesn't help them since they don't get to use the money they collect in their own budget.

They can't choose to spend more, knowing they will make it back.... they don't have the money to invest in going after rich tax payers. They can only spend the budget they are given, and that isn't enough to go after rich people, even if it would bring more money in.

I expected this was a big reason for the seemingly illogical behavior, but am curious how it shakes out. Where does money they recover go?

It would seem to make sense to seed a high income investigative unit, checked by the courts, and then allow them to retain a substantial portion of their recoveries to self-fund.

IRS is funded out of the general fund by Congress, which is also where the money the IRS finds goes.

> It would seem to make sense to seed a high income investigative unit, checked by the courts, and then allow them to retain a substantial portion of their recoveries to self-fund.

Limiting scope sounds nice in theory but there is always scope creep when you throw greed into the equation. And generally speaking the courts are not designed to be a fast resolution to anything.

That's why you build a system of adversarial justice: enforcement vs defense. Same as we feel is good enough to use elsewhere.

And a fast resolution doesn't seem required in this case. High net worth individuals don't seem like they'd be impacted by {potential tax bill and penalties} of their assets being frozen for multiple years while a case plays out. Relative to their total assets, any tax bill is going to be manageable.

The only problems actually preventing the IRS from conducting this enforcement are (1) political cover from direct Congressional interference & (2) lack of resources due to general defunding by Congress.

Given a choice between the dangers of establishing a self-funding high net worth tax prosecution arm and not prosecuting those individuals, I feel the greater risk to democracy is the later.

Maybe IRS just knows that they're being underfunded precisely to stop them from auditing Congress's rich sponsors, so they proactively self-censor their audits to prevent further cuts?

I don’t understand how Republicans can argue cutting funding to the IRS will save the government’s spending. Instead their goal is to make the tax base richer by cutting taxes of the rich. Many of them are all about cutting taxes to the rich and corporations, doubling down on the trickle down. They even blocked payroll tax cuts to the lower and middle class:

It's because the costs for going after well-funded and well-defended tax cheats is higher than going after middle and lower income people who can't defend themselves. This has been known since George Bush II's tenure.

The IRS selects which returns to audit based in part on a statistical formula that identifies returns most likely to be at risk of having an error

So yes, you're correct. Analyzing whether or not someone is eligible for EITC (those making less than ~$50,000) can be automated and if flagged, a letter sent telling them they aren't eligible or asking for more information.

Wealthy people have the resources to defend themselves in court. If you live paycheck to paycheck, you generally cannot afford lawyer fees, taking time off work for court appearances, or the risk of actually losing a case, or the probably million other things I'm not thinking about right now. It is almost always easier to go after the poor than it is to go after the rich and powerful.

I also read an article on this a while ago that said that at least informally, the metrics changed in the IRS - the practice went from evaluating auditors based on the dollar value they recovered to evaluating auditors based on the number of files they opened and closed. So of course now the auditors focus on the small cases because they're quick and easy, and they don't want to have to explain to a performance management system why they closed fewer cases than their coworkers.

Audits of the rich are not economical for the IRS. Audits of the poor are extremely cost efficient, because they can be automated, and because they don't fight back.

Maybe we just need a new agency. One that targets rich people that us plebs can support and politicians can promote. And then just keep the IRS how it is going after plebs for us to hate.

Seems like institutional failure if I have to vote for IRS expansion, the same people going after my tiny coffer, for the IRS to go after anyone else. That's a dumb conflict of forces.

That's deft political engineering. Congress is to blame. They tweak the budget to protect themselves and their true constituents (megadonors and lobbyists).

We're in a peculiar situation where democrats and republicans are both on the "right" in their fiscal policies. Any blush of "left" policy is shouted down by bipartisan echoes of McCarthyism. The politicians of both parties are, by and large, upper class, and they collectively pit the middle class against the lower class.

We don't need a new IRS, we need a new breed of politician. And enough funding for the IRS that it can audit those politicians and their donors fearlessly.

Off-topic, but it strikes me as interesting how everyone always considers themselves "the masses", calling themselves "us plebes" on a forum where a six-figure salary is the norm.

If you need to work in order to keep a roof over your head, food on your plate and to take your kid to a doctor, then you are working class. It doesn't matter how much money you make, because it is never enough to leave the working class and live off of your assets indefinitely.

While I agree with your reasoning, I think the generally accepted understanding of "working class" is of skilled and unskilled laborers that are distinct from the "professional class" that tend to work in offices and don't work so much with their hands. A plumber running a small business employing other plumbers with a massive cash assets could be a lot farther from being homeless than a senior lawyer with multiple houses and expensive cars but the plumber will always be perceived as "working class" in contrast to the lawyer's "professional class".

Social class defined by economic relations has material consequences that exist between countries and cultures, and the colloquial usage you're referring to[1] is dependent on where you are and who you ask.

To sociologists, economists, and academia, those who rely on a salary or wage to live are considered working class compared to those who don't.

That's not true. With a six figure income, you can live like people making half what you do, save the other half of your income and retire early to live off your assets indefinitely. That's harder to do the lower your income gets.

No. If that were the case, then some banker in NYC, making $1M a year, but no savings, living in a $2M condo with a $10,000 monthly mortgage and 3 kids in private school would be "working class".

This visualization is pretty eye opening in illustrating the difference between a cushy six-figure job and the ultra-wealthy that we're talking about as the complement of "us plebs"

There are only 500-600 billionaires in the US and I'd wager that none or very very few of them cheat on their taxes, given that doing so would have provide essentially no noticable improvement on their spending ability, but have a very high cost if caught.

I don't think your handsome graphic there is offering much insight into the topic at hand. The richer someone is, the less likely they are to cheat on their taxes.

EITC not withstanding you need to have income to hide it.

According to Brookings, the bottom 50% pay 14% of the taxes but are responsible for only 12% of evasion.

The better distinction is the source of income. Farms, landlords and sole proprietorships are the leaders in misreporting income. W-2 salary reporters account for <1% of evasion. Between those two groups are misreported tips (typically lower end) and capital gains (typically higher end)

I think "survive" has a really wide range of definitions. Most Americans live paycheck to paycheck, both the $1m+ per year NYC bankers and the $50k per year midwest mailman.

"Working class" in the sense of political economy, not Western shorthand for "blue collar".

And yes, I believe that if you sell your labor for a living, whether it be for $400k at Apple or otherwise, you have more in common with someone making $24k bussing tables than you do with the person who owns property for a living.

While they definitely are not “blue collar”, income is not wealth. It is a mistake to conflate income and wealth, the implications are very different. One can have a high income today and be destitute tomorrow absent wealth. Wealthy people are a subset of those with high incomes.

Your definition doesn't really align with how "wealthy" is used.

If you're making $400k per year, how long before you start to accumulate substantial wealth? Pretty quickly I'd say. Sure it might not be millions, but if you sock away $200k at age 25 after 3 years, you have more wealth than 99% of people your age.

"Wealthy" is not limited to wealth alone. If you're making $2M a year and have no savings, you're still "wealthy".

And people with large amount of wealth (your definition) can still become destitute. There are plenty of examples.

Yeah, but owning a single family home in one of the most desirable cities in the US makes you rich. That’s something 90% of America couldn’t dream of doing.

Low six figure salaries are barely middle class in many cities the US.

The kinds of rich people being discussed in this thread are still a very small percentage of six-figure+ earners. I would venture to say (no pun intended) that most HN readers are not accredited investors.

I believe the median salary in Loudoun County, VA, which is the richest county in the US or close, is around $70K. The lower boundary of "middle class" must be lower, then.

So I continue to think that the six-figure norm people talk about is within a "reality distortion field".

Or just start over. Dunno why my dollars that I had to go to work for and do what someone else told me to do is guiltier and more traceable than anything else.

Maybe the problem is that they are a s*ty agency that randomly fines people and expect them to pay up. I don't have knowledge how the IRS works but I know at least one tax agency in this world that would fine you random amounts and just wait for your reaction. They are not in the business of fairly auditing your numbers because they'll lose, so they turn to poorer persons that they can bully.

Another thing, many countries expect rich people and rich companies to hire government-certified accountants to verify your fillings (known as a Statutory auditor https://en.wikipedia.org/wiki/Statutory_auditor ). This makes it harder for these companies to do stuff the non-audited guy can easily do.

Its called Capitalism.

Its always been the case in capitalist society that only poor people pay tax, thats why half the world had revolutions to kick it out.

That happens because Congress wants it to happen. They have cut funding for high value enforcement and pushed going after low income filers, which is both amenable to their major donors and helps fuel the narratives about big government and taxes being too high.

This also plays out in other ways: Intuit spreads a ton of money around trying to prevent the kind of automatic tax and online filing which happens in most of the world because thinking of taxes as hard provides them with a steady stream of customers.

Remember though that tax revenue is actually dominated by the little guy.

There are some super rich tax evaders who can hide many millions from the IRS, but they are few in number and it will cost millions to recover that money after going through all the obstacles such rich people can afford to put in place.

On the other hand, imagine 100 million people all under-reporting $1200 - that's $120 Billion Dollars, or about 6 NASAs. If you actually had to go after everyone, that would be extremely expensive, but if you go after just a small percentage of people, the rest will be scared into properly reporting their income. We all know one or two people who have run into serious trouble with the IRS: enough that we are familiar with the consequences but not enough that it seems like a common and socially acceptable strategy. This is by design.

With the very wealthy, this strategy doesn't really work. Just because you manage to get one bank in switzerland to hand over some data doesn't mean my bank in the caimans is going to do the same. Even if the IRS were to catch up to me, I can afford to wait to cross that bridge when I come to it. You can take billions from certain people and they will still have net worths greater than some nation states - those who can afford to lose can afford to play the game.

It's also worth noting that the tax code has plenty of loopholes that wealthy people and corporations can use to legitimately reduce their tax burden. IRS recovery isn't going to be able to do anything about that. If you have billions of dollars, you can afford an accountant who will make sure there's nothing for the IRS to go after.

Really changing the funding of the IRS is irrelevant - were we to simplify the tax code to eliminate loopholes and make it easier for people who can't afford armies of accountants to properly pay their taxes we could both collect more money and spend less on recovery. It may be impossible to get congress to actually do that, but anyone talking about playing around with the IRS's funding is just trying to look like they're addressing a problem they really have no intention of solving.

> In 2017, the bottom 50 percent of taxpayers (those with AGI below $41,740) earned 11.3 percent of total AGI. This group of taxpayers paid $49.8 billion in taxes, or roughly 3 percent of all federal individual income taxes in 2017.

> In contrast, the top 1 percent of all taxpayers (taxpayers with AGI of $515,371 and above) earned 21.0 percent of all AGI in 2017 and paid 38.5 percent of all federal income taxes.

> In 2017, the top 1 percent of taxpayers accounted for more income taxes paid than the bottom 90 percent combined. The top 1 percent of taxpayers paid roughly $616 billion, or 38.5 percent of all income taxes, while the bottom 90 percent paid about $479 billion, or 29.9 percent of all income taxes.

> First, these numbers refer only to federal income taxes. Both the federal and the income part are important.

> The income tax is not the only tax collected by the federal government — far from it. Just half of the taxes collected by the federal government come from the income tax. About a third come from payroll taxes — which fall much more heavily on working people, since they’re largely levied only on the first $130,000 or so of earned income.

..

> Second, the wealthy naturally pay a disproportionate share of federal income taxes because they make a disproportionate share of the country’s income. In other words, these numbers to some degree demonstrate exactly the opposite of what those who use them claim: They’re not an indication that the superrich are beleaguered, but are in part a sign of America’s staggering wealth inequality.

..

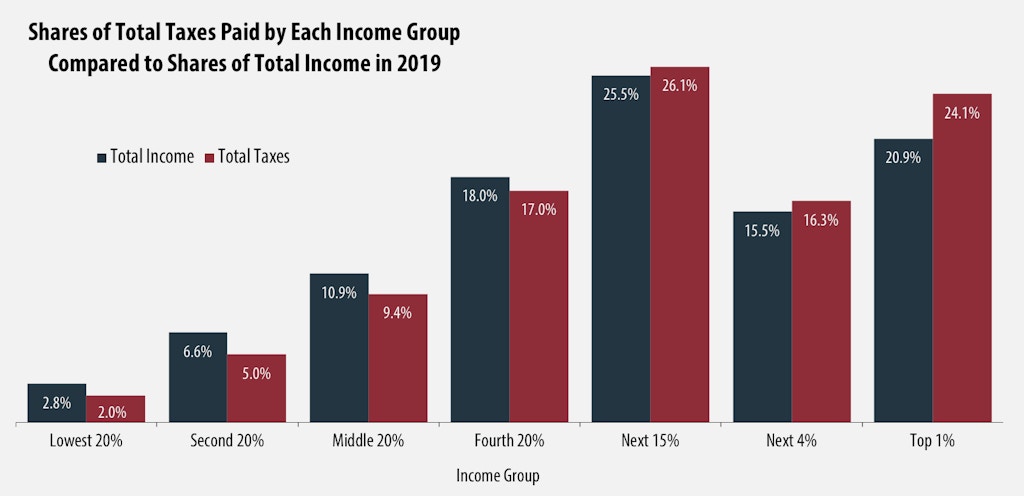

> the top 1 percent — with an average income of about $2 million — made 20.9 percent of America’s income, but paid 24.1 percent of America’s taxes. Few people will perceive this as a monstrous injustice.

> Meanwhile, the middle 20 percent of Americans— with incomes between $41,000 and $66,000 per year — make 10.9 percent of America’s income and pay 9.4 percent of America’s taxes. The bottom 20 percent, making less than $23,000, make just 2.8 percent of America’s income and pay 2 percent of America’s taxes.

The 98% of people paying 61.5% (a significant majority) of income taxes are all the little guy. Even a decent percentage of the 99th percentile would also be the little guy. The "super rich" capable of hiding millions from the IRS are an extremely tiny portion of the population.

One other thing there is an assumption that membership in these statistical categories are 'stable' Not really though. Lot of 'the 1%' are in it for short periods of time.

Other big issue is the super rich typically have full control over when, where, and how, a taxable event happens. For the wealthy most wealth building doesn't involve taxable events. One of my beliefs is the mortgage interest deduction is a sop to the middle class. Because otherwise the wealthy would out compete middle class families for single family homes.

While it is certainly possible to give misleading statistics, these seem pretty reasonable to me? Could you say more about how you think it's misleading?

Pedantry is just another distraction, obfuscation.

GP's point is the IRS is unfairly focusing on the weakest while ignoring the worst offenders. No reasonable person disputes IRS's own repeated statements to that effect.

We can only guess the motives of any one still in denial.

Just from skim reading, theintercept's article is based on a study from ITEP and Vox's data comes from taxjusticenow.org. I'd have to dig deeper to see if they're referencing the same data of if these are just complimentary studies.

> Remember though that tax revenue is actually dominated by the little guy.

That's not correct. 4.5% of returns account for almost 60% of taxes. 17% of returns account for almost 80% of taxes. And that was before the Trump tax cuts.

This citation is solely focused on income taxes, which make up only have of the revenue. Payroll taxes are 36% of the revenue, and are only incurred on the first ~$120k of income. I think this number would be more enlightening if it included all taxes (state property and income tax too), not just federal income taxes.

> The IRS needs to prioritize its resources by going after the big fish, not obsess over kids waiting tables

If the IRS doesn't go after any kids waiting tables, no kids waiting tables will bother paying tax. And that's, in aggregate, a lot of money.

This is a similar fallacy to the idea that cops should not investigate minor crimes - say, burglaries - until it's solved all murder. If they actually do that, burglaries will effectively be legalized, and anarchy ensues.

The bigger mental trap here is I guess a failure to consider second order effects.

Finding mistakes and cheating from lower earning tax payers merely takes some computer time. Finding problems with richer tax payers who have more complex tax returns actually takes a lot of manual effort, so budget cuts in enforcement affect the latter much more than the former.

Kinda. If you document your tips in a manner acceptable, you're taxed on those. If you don't document, then there's effectively a "standard assumption", in cash-heavy or tip-heavy/driven jobs.

The flip side of this is that many servers don't document because, well, they make above the standard assumption.

I'm coming late to this, but I think there is a parallel in policing generally, where cops would rather take on low risk, easy win "mall cop" activities like petty drug and traffic enforcement than deal with major crimes that have a real harm in society. Without a much more specific mandate from lawmakers, it is too easy to go after minor infractions by defenceless people instead of doing some hard work.

The problem is it can be so hard to prove misdeeds on the part of the rich. Most of the stuff the average Joe does causes reports from the other side of the deal, the IRS simply needs to match them up. Easy peasy, I get a notice from the IRS that I didn't report $1234 because I slipped up and typed $1233.

Look at the various reported tax games with Donald Trump, though--many involve situations where the other side of the transaction is cooperating. If both sides are dirty the IRSs job becomes much harder. Also, the more complex financial transactions can't be distilled down to standardized reporting so well, it's much harder to match both sides.

> Congress has consistently cut funding for the IRS for years and years

I just want to clarify that de-funding the IRS doesn't have universal support in congress and is actually a partisan policy. I'm guessing you know that and are just toning it down to be less politically offensive on HN.

However, this is an important distinction and not for the sake of finger pointing. It's important because it means that we have the power to change our government. We have the power to demand better of our politicians and to refuse to vote for them if they support policies that make it easier for tax cheats to walk while increasing the tax burden on everyday people.

I understand why you might want to tone it down and just blame congress and all politicians for this type of policy (because, yes politicians are gross and should be kept at an arm's length), but that breeds the idea that we are just stuck with a broken government that can't be changed. You really can have an effect on government if you are willing to look at who historically votes for policies like this and make the choice that is best for you. If you didn't have power in the process, then our politicians wouldn't be spending so much money on campaigns to get you to their side.

From the articles you linked:

> The IRS has never been a popular cause on Capitol Hill. But Democrats and Republicans long shared a grudging consensus that the agency’s basic work of tax collection deserved protection.

That changed when the Republican Party came into power in 1994 and Newt Gingrich became the speaker of the House. The new majority’s main priority was tax cuts, and vilifying the IRS helped its case.

> The notion wasn’t a fringe position within the party. Former Sen. Richard Lugar of Indiana, a respected mainstream Republican, ran for president in 1996 on a platform of abolishing the IRS. A Republican congressman in 1998 introduced a bill to repeal the Internal Revenue Code by 2002. “Abolish the IRS” remains a potent talking point. Ted Cruz, the Republican senator from Texas, campaigned on the slogan when he ran for president in 2016.

> Republicans, riding the Tea Party wave, took control of the House of Representatives and started hacking at the IRS’ enforcement budget

> Down it went, some years the cuts were steep, some not, as Republican lawmakers laughed off dire warnings about the consequences of letting tax cheats run free.

Having a bored and well-funded cop on every street corner, looking for crimes, is not the best thing for a free society. "Make sure everyone pays their fair share" seems reasonable, but all too often degenerates into "spend years harassing a single mother over the EITC tax credit, then chalk it up as a win when she folds."

I've seen those return-on-investment studies saying "for every $1 allocated to the IRS, they collect $10 in unpaid taxes," but how much of that comes from harassing people who end up paying because they can't afford to spend years litigating in tax court, versus people who were actually hiding income?

The point is to specifically fund enforcement against actual tax evaders. They go after small cases because they have no resources to go after anything bigger.

There is no way to correctly assess how much tax should be owed in even moderately complicated situations. Income tax law is way too vague and relies so much on the intentions behind activities. It's also always playing catch-up to new tech.

Enforcement involves substantial interpretations that reasonable people in and out of the IRS can disagree on.

This is not an argument for more or less enforcement, but I've found people usually neglect this aspect.

Very good point. Our massively over-complicated tax code only advantages wealthy people who intend to cheat or skimp on taxes, and tax prep companies like Intuit -- the latter of whom actively and successfully lobby Congress against tax reform.

This should be a bipartisan issue, but neither party seems interested in tackling it. A cynic might argue that this is because both parties are interested in maintaining the status quo, their leadership being full of people who benefit from it (or friends of such people). It also helps ensure that running the country is expensive and inefficient, making progressive policy harder to implement.

This is an anecdote that I have not tried to verify, so take that for what it's worth. A colleague in the early 2000s immigrated from New Zealand to the US. His wife went to get a job at a grocery store, and he told me that he was amazed that the hiring manager could not tell them how much of her pay would go to taxes. The implication being that this sort of thing is easy to figure out in NZ, but impossible in the US because of complexities in the US income tax system.

> His wife went to get a job at a grocery store, and he told me that he was amazed that the hiring manager could not tell them how much of her pay would go to taxes. The implication being that this sort of thing is easy to figure out in NZ, but impossible in the US because of complexities in the US income tax system.

That's because the hiring manager doesn't need to understand tax rates to do his job. He plugs the numbers into the black-box HR system, and the system spits out dollars, that he pays employees with.

The reason for why you have no idea how much the government will take in taxes, is because income taxes are progressive, and are charged based on total income earned per year.

So, someone working at a $200,000/year job for a year, will have a tax rate of ~26.5% (I'm ignoring Social Security).

But if they were unemployed for 9 months, and started working that job on October 1st, they will have a tax rate of ~16.5%.

What this means is that when you start a job, you have to guess what your likely annual tax rate is going to be, and set up withholding for that amount.

If you underpay by a large enough sum, the IRS will send you a bill, with an extra penalty next April. If you overpay, the IRS will send you a tax return.

Here in Russia we use another system: employees don't have to pay taxes from their wages themselves. It is company's responsibility to calculate and pay it. This system has an advantage, that most people don't have to bother with filling out complicated forms every year, but it has also disadvantages because people don't see how much money they give to the state.

As vkou said, the hiring manager has no idea what taxes the wife will pay...but the payroll manager does, and could probably tell her exactly what she would pay based on her start date, estimated wages based on expected shifts, and exemptions.

Expecting the hiring manager to know the tax stuff would be like expecting the dev team to know how much income tax the business is going to pay.

Step 1: did you receive money? That is income.

Step 2: if you incurred expenses in making that money, and that money is not a wage/salary paid by a business, deduct those expenses from the income in Step 1. Otherwise, deduct nothing.

Step 3: look at the tax table for the amount at the end of Step 2 to see what the tax you owe is.

It only gets complicated if you want it to be complicated, such as if you're trying to maximize potential deductions or minimize taxable income by exploiting loopholes or special provisions.

> It only gets complicated if you want it to be complicated

That's not true. I wanted to claim some cash income this past tax year and it was a pain in my ass. It's very relevant how you made the money: for instance, if you made it gambling vs a woodworking hobby vs a small ebay reselling business, all are handled differently.

>Friendly reminder that IRS enforcement is one of the most cost-effective activities that the federal government can engage in, and that Congress has consistently cut funding for the IRS for years and years

It hardly matters whether it makes money. Two things come to mind:

* Civil asset forfeiture is one of the most profitable acts for police departments. California outlawed this for money below some large sum.

* Traffic tickets are one of the most profitable acts for some city departments. I would far prefer that they reduce that.

I don't care that the Federal Government makes money. It is not a good thing that it makes money. It is just a thing.

When North Carolina came after me for taxes they thought I owed, only for them to reduce the judgment from the many thousands to a few hundred dollars when I sent them a "yo, I think you're mistaken" letter, I didn't feel pleasure. The fact that they insisted any further appeal could only occur in person, knowing full well that a flight to that state cost more than paying the bill, I did not feel like the government was made better through the experience. If they had decided that they should collect the whole amount I would not feel like they would be doing a better job.

That would tend to encourage raising tariffs. Which is, generally, bad for business (and gets very complicated in the context of trade treaties and the WTO).

Payroll taxes are a tariff on labor, income taxes include non-labor (but “long-term” capital only at a favored rate) income, so aren't exactly a tariff on labor, though they also aren't neutral between sources of income.

1) The federal government is not a business, it's a federal government. It shouldn't be looking at taxes as a "cost-effective activity with a positive return on investment".

2) The entire concept of increasing the IRS's budget so they can collect more money is circular reasoning that leads us down a race-to-the-bottom scenario, but the "bottom" in this case is maximizing tax revenue to the point where everyone is squeezed dry....because the government apparently knows how to spend their money better. I.E. Increase the IRS budget so we can collect more taxes, so we can increase the IRS budget so we can collect more taxes, so we can...

3) For your final selfish argument, it's debatable to say it's better for you that others spend their money on taxes rather than less on taxes and spending it however they please. Any standard macroeconomics course will show you that people spend most of the money they have access to. In other words, they're injecting that money directly back into the economy, which typically adds ~10x in value to the economy as a whole, as it trickles through the supply chain. e.g. they buy a new couch: delivery guys get paid to deliver it, delivery company profits off the delivery, furniture store salesperson makes a commission, furniture store makes a profit, couch manufacturer makes a profit, company who produces couch cushions gets another order to replace the sold couch, couch cushion company orders more fabric and couch cushion stuffing.....

The IRS collects more money by collecting the money people actually owe but did not pay. Taxes could be reduced by as much as 10% if the IRS was able to collect the underpaid taxes. I don't know why you're against that.

For your final selfish argument, it's debatable to say it's better for you that others spend their money on taxes rather than less on taxes and spending it however they please.

The IRS doesn't determine tax rates or tax laws, it just enforces them. And to note, all of the infrastructure that pays for the road the delivery company used the deliver the couch, and the forests which provided the lumber for the couch's frame, and the ease of contract which made all of these transactions...were all made possible by the taxes collected and paid by all of these people.

Tax is a vital part of the economy. It's the price (fee) you pay for the government services that underpin everything else.

> Do you honestly think that if the IRS successfully collected more taxes that politicians would reduce taxes?

These numbers on budget shortfalls, deficits, and CBO estimates that are thrown around every time a tax credit or additional tax is considered are very much affected by revenue collection. In SF where there's quite a bit of direct democracy, they were also thrown around to the public when considering several tax or tax-adjacent referenda such as the recent tax on high-revenue businesses or a few on the upcoming ballot, all of which come with their own budget estimates. I'm doubtful that all of this would have no effect the next time balancing the budgets is considered.

Taken to the logical extreme, we'll have privatized road services, privatized police and firefighters, and privatized postal services. This is an even worse race to the bottom where some areas just don't get served at all because it's no longer lucrative. Or people who live in areas that were previously served but no longer maintained have nothing to do because the company that was handling the roads is cutting costs. Their only option is to move but that's not easy. Some things just have to be handled by the government and I'd argue the US does a horrible job at this. USPS funding is going down and healthcare and insurance sucks.

The IRS isn't collecting more taxes. Even a kid would know they aren't even allowed to do that. They're just collecting taxes that are already owed. If the government wanted to increase taxes then they could already do that right now but they aren't because no one would vote for them. Increasing IRS funding would help the government collect taxes from the people who owe them which would lower the overall tax burden of the average tax payer (assuming they actually pay taxes).

If it costs the IRS $100 to collect $1000 then that means that's $900 less that everyone else needs to pay.

>The IRS isn't collecting more taxes. Even a kid would know they aren't even allowed to do that.

With a sufficiently complex tax code, bureaucrats can selectively enforce or interpret it as they choose. It wouldn't be unreasonable to expect abuse if there is an incentive for agents to collect more.

I'm by no means against taxes, I completely agree they're rightfully used to fund roads/police/fire/etc. My primary argument is that the richest government in the history of the world has more important things to prioritize than making the IRS more ruthless against the middle class. And I'm saying that if they end up collecting more tax money, it doesn't necessarily mean it's a net positive for society as a whole. Most of those tax benefits are reaped by big business, so in other words those benefits are reaped by the owners of those big businesses.

The low vs high tax debate is kind of a moot argument anyways since the US govt can pretty much print money as needed...which ends up being an indirect tax on the general public via inflation.

> And I'm saying that if they end up collecting more tax money, it doesn't necessarily mean it's a net positive for society as a whole. Most of those tax benefits are reaped by big business, so in other words those benefits are reaped by the owners of those big businesses.

This seems to indicate that it is a net positive for everyone else. If they don't collect tax money from those owners, all of the benefits of that money goes to those owners and none of it goes to anyone else.

> The low vs high tax debate is kind of a moot argument anyways since the US govt can pretty much print money as needed...which ends up being an indirect tax on the general public via inflation.

So... it's not a moot point? One group, through taxation policies, is asked to pay a larger share of what would have been an indirect tax on the general public.

Your tax rate is actually around 57% because you forgot to include your medical insurance of around 11% at that salary for a family of 5. Roughly $2,000/month. If you are comparing tax rates with first world countries you need to include your health insurance costs or the results will be skewed.

Luckily with a salary in the top 2% nationally you can afford insurance. The same can not be said of people who are not rich.

I agree that health care is very expensive, but you may be overestimating a bit... I looked up some plans on California's exchange for a hypothetical family of 5, and all except for the "platinum" tier were between $1200/mo and $1600/mo -- so 6% to 9% in this particular example.

With a lower income, the percentage would increase -- but only up to a point since a family of 5 starts qualifying for ACA subsidies if their income is less than $120K.

The subsidies make a big difference -- 84% of people who purchase insurance through the exchanges receive a subsidy and the average monthly cost of a plan after taking subsidies into account is $145 (vs $595 without) [1].

Your math is bad, and you're using a nonstandard set of numbers.

Generally in CA, and most of the US, you would receive health insurance through your employer, and the bulk of your medical insurance premiums are non-taxable subsidies by the employer.

Like I said, your math is bad. You're using numbers from individual plans, not employer-sponsored plans. As individual plans are entirely separate pools from the employer-sponsored plan pools, the numbers aren't even remotely similar.

It's harder on the poor. The percentage figures will vary based on your income level. Luckily the OP chose an income level in the top 2% of all Americans which made it a somewhat reasonable level.

This was also an individual plan bought on a healthcare exchange. Large employers have a stronger negotiating position and can get somewhat better rates, but in the end you're still basically paying a tax and it is disingenuous to compare tax rates with countries that provide socialized healthcare with their taxes and not include the cost of healthcare coverage in the States.

It is not fair to compare taxes between countries with and without healthcare, but it is almost impossible to compare otherwise. For example USA has huge prices and excellent services compared to almost any other country, in my country (Romania, Europe) the socialized healthcare is so bad many people have a private insurance, I have 2 private insurances through my employer and I still pay out of the pocket about half of everything I get (100% of dental care is out of the pocket, most consultations are covered by the private plan, most treatments are out of the pocket).

You're also forgetting social security, as well as your employer's contribution to medicare and social security (Which is the same as your own). They get deducted from your paycheque (In both Canada, and the US) before you even see it.

Which, for an income of $231,600/year ($11,600 of which get taken off your paycheque before you even see it), adds up to a total of $71,143.

Meanwhile in Ontario, your total tax burden, for an income of $223,750 ($3,754 of which gets taken off your paycheque before you even see it), adds up to... $88,663.

Of course, in California, your employer is also spending ~$20,000/year on your health insurance plan (And is asking you to pitch in ~$6,000).

In Ontario, at that income level the province will bill you... $900/year for a health premium. The rest of your health care costs[1] come out of the regular taxes you pay.

...And if we add all that to the math, you'll discover that the Canadian takes home a bigger portion of their paycheque then their American equivalent.

[1] Okay, I'm also missing vision and dental, which are part of the $20,000/year employer part of your health plan, but are not covered by the province of Ontario. The Canadian would have to pitch in a bit of cash for that.

Hm, I actually did the full pay calculation included payrolls a month ago for myself last year. Granted, I was in washington last year, but between federal income taxes, social security, and medicare mine was about 27% on 221k income as a single person with no kids and I'm including the employer payroll taxes as part of that income. Converting USD to CAD gets you 294,528 which has an average tax rate of 41.69% according to this website [0] and it doesn't include your payroll tax.

As for healthcare, vision, and dental for a single person with no kids my employer paid $8,800 for the year, I paid 150, I get to put $3,500 pretax income into a HSA for healthcare spending, and my max out of pocket spending is $2,600 so that's not really a concern for me.

Washington derives all of its tax revenue from things that don't appear on your paystub. Property taxes and sales taxes. Because it's not saddled with Prop 13, it can actually collect property taxes at its posted rates.

This does, however, mean that it has one of the most regressive tax regimes in the country.

If we are going into such detail then we also need to take into account differing currencies, cost of living, salary distribution, purchasing power parity, sales taxes, property taxes, tax credits, etc.

Just as an example, my salary in the US would be 30-40% higher and denominated in a currency that is worth 34% dollar for dollar.

Sales tax in Ontario is 13%, sales tax in Cali is 7%. Property tax in Toronto is 0.61%, property tax in San Francisco is 1.18% [1]. The net burden of these non-payroll taxes is pretty similar.

[1] Assuming you're one of those suckers that isn't laughing all the way to the bank, thanks to the mindboggling piece of legislature called 'Proposition 13'.

Marginal tax rate is a weird way to look at it when you list a specific salary. You should use the actual effective tax rate that person would pay, which is 34.8%, fico, state and federal.

Wages in Germany are much lower. Owning a home in a city like Berlin doesn't seem a lot easier than in SF. People are fine doing long term rentals with rent control.

Not everything is about Silicon Valley. You can move away to afford better housing. That's what I did.

In this case the relevant metric is property tax as a percentage of income rather than as a percentage of property value. On average, California is somewhere around 15th in the nation, but there's a sharp divide between new owners and grandfathered owners.

also, as ever, we have to note, since so many people do not understand it, you do NOT pay 35% federal tax on your income, you only pay 35% of your income above a certain level.

Marginal tax rate (which is specified) is at least how much you'd owe on every dollar of income after. Average tax rate is how much tax you actually paid against income.

Most people (particularly in the US) do not understand this. In addition, the actual placement of the tax makes a great deal of difference. Owing 35% on income above $35k is very different than owing 35% on income above $220k. Very people know where the tax brackets are.

Indeed. If you have 4 kids in BC, your effective marginal tax rate could be as high as 33% (Federal) + 20.5% (BC) + 1.95% (BC health tax) + 3.0% (pharmacare deductible) + 9.5% (Canada child benefit clawback) = 67.95%.

except it's impossible to simultaneously pay those rates on a marginal basis. according to https://www2.gov.bc.ca/gov/content/taxes/income-taxes/person..., the 20.5% rate only applies to income over $220,000 (which, even by US standards is in the top 3%), while according to https://www.canada.ca/en/revenue-agency/services/child-famil..., the CCB clawback only applies between $31,712 and $68,707. therefore, while you can simultaneously pay all these taxes, I don't think it's accurate to call it a marginal rate.

sorry, I was on mobile and didn't check closely enough. it's worth noting that the maximum clawback is 100%, so in order to have any benefit to claw back at $220k, you would need to have at least four children under 18 years of age. if we assume that of the BC families receiving at least $1 in CCB, the probabilities of having four or more children and earning over $200k are uncorrelated (I would hazard a guess that the actual correlation is almost certainly negative), then the number of families paying 20.5% provincial income tax and 9.5% clawback is probably around 52.

in order to also be paying the 3% pharmacare deductible, you'd also need to be spending at least $7k per year on medical expenses, as well as making less than $316k before taxes. on the whole, I would say that paying that much medical expenses would make someone disinclined to have (more) children.

in conclusion, while I was wrong to say that it's impossible to pay all those taxes simultaneously and marginally, it seems highly unlikely and I doubt that anybody in BC actually pays that marginal rate.

Please come in Romania, then cry for every Euro you pay in taxes, you will get almost nothing out of it. Please go to UK and wait 3 to 6 months for a doctor appointment. Go in the Netherlands and see how is to be sent home when you have pneumonia because they are busy treating some overdosed drug addicts (real case, happened to a relative). Go to Russia (and I cannot tell more). They are all in Europe.

The difference is that healthcare is paid on top of the 25% (or higher), in addition to many other public services that are provided for in many European countries.

Can I deduct transaction fees? Maybe only business transaction fees?

There are a lot of unanswered questions.

I plan to on my 2020 tax filings next year.

I’ve never had an issue reporting crypto assets on my taxes since 2014. I wouldnt have been included in the “only 800 people that reported” according to the IRS’ flawed study which was just a search string for bitcoin or btc, as I was mining litecoin back then and receiving capital gains in litecoin back then. I looked and I literally had typed in LTC in a capital gain document.

These guys are so far behind reality.

The new question should be “are you yield farming and did you claim any liquidity mining airdrop?” but sure lets just wait till 2027 for them to catch up

I got a letter from the IRS a few months ago and the text said something along the lines of “we know you have accounts on cryptocurrency trading services. Please be aware that crypto trading is taxable and you can face severe penalties and even jail if you don’t report them”. I do have accounts but I have not traded with them... My guess the account they’re referring to is the one in coinbase, which I have not used since they announced the service.

That's exactly how it should work though. If you buy 1 BTC today for 10k USD, and then its market value increases to 400k USD and you buy a house using it, can you really argue that you haven't just made a capital gain of 390k USD?

Only if you sell it. One way is when someone chooses to get a loan agaist the asset instead of selling it. Of course, a lender would be crazy to loan against the future value of BTC.

Lenders have been doing great lending against btc and other digital assets. They all set up systems to immediately liquidate the borrower and also sell the asset (or hedge against it).

Its the borrower that amplifies their risk.

But if a borrower collateralizes well enough it is much more tax efficient for them.

These are solved problems for 2 years.

And yes, that is an additional example about why assuming there is a capital gain or loss merely from seeing the flow of crypto through a Coinbase account is misguided.

Could be just a tax deductible interest payment to service a business debt in a sole proprietorship. Its simply not up to Coinbase to determine or the IRS to assume either.

Coinbase is getting better about it if you use their own products for staking and earning. (1099-Misc, 1099-K). But they are still doing it wrong for people that use crypto properly and keep personal off-exchange custody of assets.

That’s how it also should work, if you are using a volatile asset. Not everyone using crypto is using volatile cryptos, and not everyone using volatile cryptos is holding them long enough for capital gain/loss to be the primary concern, meaning there is likely a more relevant tax report such as a income tax or a deduction against income tax.

So the assumption is flawed. The priorities in reporting are flawed.

It’s also a gain or loss if there was a gain or loss.

If you got paid and liquidated immediately, the price change was not worth mentioning and the income tax is.

If you bought crypto to immediately pay for a server, the price change is not worth mentioning because it likely didn’t change more than a fraction of a percent and the expense is worth mentioning.

Current law factors that in, because current law doesn't factor in what asset was used for payment.

With rise of stablecoins like DAI and USDC where equally large volumes are being used, focusing exclusively on capital gain/loss is even more misguided.

It doesn't matter though. It's like when I get RSUs and sell all immediately. I still have to file the sales as a capital gain, even if the amount is basically 0.

But to your point, RSUs - unless you did an 83b election - have a bigger income tax component, especially in your sell immediately example. Which reinforces my point that the prioritization is wrong and that focusing exclusively on capital gain/loss is misguided. This time I’ll italicize exclusively, for emphasis, lest that somehow gets lost in the message.

If you pay an invoice with bitcoins that have experienced capital gains, you have to pay capital gains tax.

>Tax deductible transaction? With crypto huh, never asked!

What is a tax deductible transaction? If you donate bitcoins to a charity by sending the bitcoins to the charity's bitcoin address that is indeed fully tax deductible and you don't need to pay capital gains tax (and you get an income tax deduction of the entire value). But is coinbase really trying to get you to pay capital gains tax when you simply send bitcoins from one address to another? That doesn't make sense.

>Receiving crypto for services rendered?

How does receiving crypto have anything do do with capital gains? Capital gains come into play only when you get rid of the crypto.

>The asset doesnt matter, only the nature of the transaction matters

Yes, and any time you exchange cryptocurrencies for something else (dollars, goods, services) that is a capital gains relevant transaction.

Isn't that because crypto is not considered currency by the US? You only get to not do this if you are paying debts in USD, even though the value of USD could fluctuate in the same way theoretically, that is ignored.

Correct, the IRS is capable of perceiving how an asset can be used, but they are not capable of unilaterally declaring the classification of an asset. Currently, when it comes to determining whether an asset is a "currency", it has to be issued or used by a recognized nation state, or Congress has to label the asset as such.

Congress could easily delegate additional discretion to the IRS, they just haven't yet as they have been unprepared for this outcome.

When you look at the universe of assets, they either exist in walled gardens (brokerage accounts that there is no expectation to withdraw from, or that you simply can't withdraw from), are not easily divisible or have separate denominations if they were, or are impractical to transport (a barrel of oil, other spot commodities), or are not fungible (art, collectibles, barter assets).

All crypto assets transcend and overlap with the fungibility of every other asset class all at once, while being able to function as non-fungible assets if desired.

Congress could easily delegate additional discretion to the IRS, they just haven't yet as they have been unprepared for this outcome.

Congress has considered this matter already, and they have chosen not to treat cryptocurrency as a domestic currency by refusing to consider bills that would classify cryptocurrency as a domestic currency.

Non-domestic currency (i.e., foreign currency) is treated as an asset under US tax law, and as a currency not issued by the US government, cryptocurrency is a non-domestic currency and is thus subject to the same tax treatment.

They havent chosen they havent gotten out of committee, like thousands of other bills per session. I would agree with you if the full house actually voted and failed.

Good move. I’ve gone from excel most of last decade, to services like cointracker in 2017-2018, back to excel because those services dont keep up with the various trading venues and types of transactions in crypto and across chains, to excel + zapper.fi and yield farming accounting services in 2020

Isn’t this how the IRS treats it so that’s how Coinbase has to treat it? If one buys a bagel with Bitcoin, then one needs to treat it as a sale of Bitcoin to US Dollars

Yes, hence the entire crypto fad is a mass delusion built on lies. It’s regulated like a security, hence you’re not going to be able to use it like currency. Ever.

Cryptocurrency is considered a capital asset, so there are 2 taxes that apply to a cryptocurrency transaction:

(1) normal income taxes, to the person receiving the crypto, and (2) capital gain taxes (or losses) to the person sending the crypto, because capital taxes apply to capital assets when they are disposed.

The nature of the transaction is irrelevant to (2).

Also could be true you were part of a data leak from one of the exchanges. The IRS actively pursues collecting this data, and I've had some very interesting conversations with one of the contractors they use to help scan the Internet for such things.

If you were included in the mtgox leak, you probably got such a letter too.

I don't see how this is any sort of trap. It just removes the possibility the tax payer can feign ignorance about having to pay taxes on cryptocurrency transactions.

Cryptoholders should consider themselves lucky it's not considered a "collectible". For example:

"For federal income tax purposes, gold is considered a collectible - just like art, stamps, or those baseball cards you've been hoarding. What that means is that instead of a maximum long-term capital gains rate of 15% for most taxpayers (20% for high-income taxpayers), you'll pay a maximum long-term capital gains rate of 28%."

If you receive enough valuable content in exchange for that menial task, you report it on your income tax return and pay taxes on it.

Generally, the value of the content you receive (to you) is so immaterial that you would have to spend your entire year on it to receive enough of it to be subject to tax.

It doesn't say "crypto" currency, it says "any virtual currency". So what do they mean by any virtual currency? ACH direct deposit? Starbucks gift cards? RuneScape gold? Virtual currency is just currency that isn't physical. Bitcoin was not the first virtual currency (nor the first decentralized currency).

They should just remind everyone that cryptocurrency counts as income. No need for a question that has an ambiguous answer. This is going to confuse a lot of people.

ACH direct deposit is absolutely not a currency in any sense of the concept. It's a vehicle for USD—direct deposit has no value, it's a transaction. Gift cards can maybe be considered a form of currency, but they're hardly able to be treated as one since you can redeem them in exactly one way, and the issuer needs to count them as a liability in the currency they were issued in (mining a bitcoin doesn't create debt on Satoshi's corporate ledger).

You can argue the semantics all day, but nobody is buying up and trading millions of dollars in Starbucks gift cards. Arguing that these rules are for any purpose other than cryptocurrency is wild. The IRS doesn't create rules for things that aren't a material concern, and cryptocurrency is the only recent "virtual currency" that is a material concern.

The question is: "At any time during 2020, did you sell, receive, send, exchange or otherwise acquire any financial interest in any virtual currency?"

and right #7 says: "Taxpayers have the right to expect that any IRS inquiry, examination, or enforcement action will comply with the law and be no more intrusive than necessary"

Whats the confusion? The IRS has a legitimate power to ask taxpayers about their income, in compliance with the law. Asking the question doesn't appear to be "more intrusive than necessary".

Purchase and ownership of cryptocurrency is not taxable. The question is overly broad since it covers activity and situations that do not factor into tax liability.

I would guess that the Taxpayer Bill of Rights is one of those silly "does not create a private right of enforcement" non-laws. As in yes, it's a law, but nobody who cares about it has the right to enforce it in court.

> For their part, many crypto users are angry with the IRS’s guidance, which treats bitcoin, ether and their kin as property rather than currency. So if a crypto holder uses it to buy something or exchanges one cryptocurrency for another, there’s usually a capital gain or loss to report on the tax return.

I was confused by this statement, as my understanding is that treating it as a currency would result in worse tax consequences.

I'm not aware of any worse tax consequences, but I guess it is possible considering the potential for those sweet long term capital gains rates.

The problem I have with treating cryptocurrencies as property instead of currency is that it creates a massive accounting burden, effectively killing its potential use as a transactional currency. Can you imagine what it would be like if you had to report all of your bank statements, credit card transactions, and cash transactions to the IRS and have it all reconciled?

You have to record all forex investing gains and incomes. So if you have an account with euros and are exchanging them to dollars throughout the year to buy things, you must report gains and losses as well.

I think the issue is that for tax purposes anytime something changes to dollars and gains or losses occur.

Whether crypto is currency or an asset won’t affect this much. I think you need a new tax rule altogether that let people “settle up” at the end the tax period or something.

> You have to record all forex investing gains and incomes.

I'm not sure about the US but this is definitely not the case in the rest of the developed world.

You are saying that every American citizen when they travel overseas, exchanging money and purchasing items on their card have to report that to the IRS?

Get the feeling this only applies to professional traders not people on holiday.

I'm not sure about the US but this is definitely not the case in the rest of the developed world.

It actually is in the EU, and most of Asia.

You are saying that every American citizen when they travel overseas, exchanging money and purchasing items on their card have to report that to the IRS?

That is not forex investing.

For most American citizens, the only taxable forex transaction would be when they convert the foreign currency back to USD, because that is the point at which the change in exchange rates may have created conversion-related gain or loss. (I.e., very simplified example: you paid $100 USD for $100 AUD on arriving in Sydney Australia, and paid $100 AUD for $110 USD leaving Australia, resulting in forex gain because the AUD became worth more by the time you left.) However, if you are not a person who regularly trades currencies, generally you don't have to report forex gain unless it exceeds $200 for the year (in the US; the threshold differs for each country).

Can you imagine what it would be like if you had to report all of your bank statements, credit card transactions, and cash transactions to the IRS and have it all reconciled?

Seems like that would be easier. They tell me how much they think I owe, and I either send it in or file an appeal.

Can you elaborate? Currency treatment wouldn’t make sense for most digital assets but what way would the tax treatment be worse than unclassified property?

If I buy Euros with USD and then buy a meal or hotel stay with those Euros, I don’t pay any US tax (and importantly, I have no IRS paperwork obligation) regardless of whether the Euro-USD exchange rate changed on the meantime.

The same is not true if you replace Euro with Bitcoin above.

I would argue in the case where I used the currency to buy something in that currency that I did not have a “gain on a currency transaction” of any amount.

I would guess the IRS would disagree, since you're even supposed to pay taxes on bartering where no currency exchanges hands, just goods or services.

So if you exchange $20 USD for foreign currency and then buy something a month later where it would have cost $25USD to get the same amount of currency, that's a capital gain.

That doesn’t answer the question, that was an unnecessary example about the status quo, how would it be worse if the IRS treated them like currency because you just wrote an example showing how it would be better. Let’s just wait for the person I originally responded to then

Showing a use case where a digital asset is used as currency seems perfectly responsive to your comment that currency treatment doesn’t make sense for digital assets.

I said for most digital assets. That wasn’t an accident. Utility tokens, security tokens, NFTs, wouldn’t make sense to be treated as currency, since I’m around people that require me to specify.

And then you have an example that didn’t show how proper accepted legal designation as a currency, in the future, would lead to worse tax treatment, which is the supposition we were talking about. Let me know if you come up with something.

Given that crypto is regulated as merely being property, it seems quite arbitrary to ask questions specifically related to it. Where is the Beanie Baby question or the question about my old Magic cards sitting in a box?

Quote: "In late August, the agency released guidance affirming that taxpayers who receive crypto for completing “microtasks” must declare it as income. This applies to users of firms like StormX, which makes tiny payments in crypto to people who do small tasks such as playing games, answering surveys, or evaluating products."

Ahhh, but this is heaven. If I'd be an US citizen doing crypto transactions I'd made sure after each of them to write them down already prepared. Then when tax declaration season comes hit IRS with a bag of 20 kilos of paper in declarations. No more than 1000 people to do this and trust me, IRS will change their tune so fast your head will spin.

People in crypto have this bizarre fantasy of the IRS as a place where they still keep everything in paper files.

The IRS processes more tax returns every year than the entire EU combined. It switched to digital files a long time ago. If you file your return by paper, it gets scanned into a digital copy and the original gets carted off to a warehouse somewhere in the mid-West. If you get audited, the auditor is looking at a digital copy of your file. If they are looking at a paper copy, it is because they printed that copy out for personal convenience.

If you send the IRS 20 kilos of papers, the people who they hire seasonally will process your 20 kilos of papers and an automated system will scan and convert each and every page. Though generally, if your tax return would exceed a certain length, you are now required to file electronically and any supporting attachments are to be kept on file so they can be requested by the IRS as necessary.

(On a somewhat bizarre note, the tax court requires paper copies of all filings and documents, though in some circuits the tax court now allows discovery to be satisfied through the provisioning of digital copies.)

If you have tried one of the robo investors, the amount of transactions that they generate, even under routine usage (regular contributions, tax loss harvesting etc.), it is beyond any human's ability to comprehend. Fortunately for IRS, computers can very easily track, trace and make sense of large volumes of transactional data without breaking a sweat.

The way US taxes generally work is that you don't provide the transaction-level details to the IRS when you file your taxes, just the aggregate. You only provide the transaction-level details if and when you are asked to during an audit.

Read the article. In regards to crypto they expect exactly that. Here is another quote from article, above:

"“Buying a sandwich with cryptocurrency shouldn’t be a taxable event,” says Sean Cover, a New York City cryptocurrency holder who works in finance for a nonprofit group. He says that in 2017 he had more than 500 transactions on several platforms, and it took him 10 hours to prepare his crypto tax forms even though he paid for special software. "

A crypto transaction is a transaction of a capital asset, so yes, it is exactly that and Sean should choose to use regular USD next time if he doesn't want to track all of his capital asset transactions. You live by the sword, you die by the sword, and all that.

But generally if your return would exceed a certain length you now have to file electronically.

Taxation is obsolete as a revenue mechanism for a monetary sovereign. The only value of taxation is to discourage an activity. To discourage the generation of income is profoundly counterproductive.

I am more than happy to be able to access to healthcare, school, good infrastructure thanks to my taxes – but I'm European, so maybe it's more about how the US system uses your taxes instead of the taxes itself.

Also, since crypto gains are considered capital gains, then any capital losses you have been accumulating can now be used vs your capital gains.

The problem here is.. how the heck can the IRS verify your claim that some gains were capital gains? What if you sell drugs for a living and invest poorly in the stock market. You just send your drug sales gains in as crypto gains, and so you have effectively washed your illegal gains, giving you the benefit of being able to not pay tax on that bc of your capital losses.

That's exactly how it works - you pay taxes on net gains (gains minus losses) in a tax year, and if there's a net loss you can deduct and/or carry it over. Why is that problematic? It's exactly how gains/losses work when trading shares of stock.

Hodl (/ˈhɒdəl/ HOD-əl; often written HODL) is slang in the cryptocurrency community for holding the cryptocurrency rather than selling it. A person who does this is known as a Hodler. It originated in a December 2013 post on the Bitcoin Forum message board by an apparently inebriated user who posted with a typo in the subject, "I AM HODLING."

In 2017, Quartz listed it as one of the essential slang terms in Bitcoin culture, and described it as a stance, "to stay invested in bitcoin and not to capitulate in the face of plunging prices." TheStreet.com referred to it as the "favorite mantra" of Bitcoin holders. Though originally used in relation to holding Bitcoin, it is now also used to describe holding other cryptocurrencies and tokens.

They already did something similar last year so this comes as no surprise. There are tax calculation services like https://koinly.io you can use to speed this up (for free)

In 2017 I played with a bunch of cryptocurrencies and made a small amount of money, which I decided to report.

Oh my god was that a pain. No help from the exchanges whatsoever. Had to compile a huge spreadsheet myself to make a big custom 1040/8949.

I hope it's easier now. I'm also glad they're trying to enforce this now. I know many people who made money speculating on crypto and not one of them reported it. The crypto community has a really nasty anti tax undercurrent (see: crypto communities moving to Puerto Rico)

Same, and it made me decide I wouldn't deal with cryptocurrencies until this stuff has proper infrastructure around it. It was such a pain in the behind to write scripts to reconcile all the weirdly formatted transactions and movements across exchanges.

I'm not even sure it worked out properly in the end, but after spending 5 days doing it, I decided what I got was probably close enough to the truth, and I called it day. If the IRS is ever unhappy about it, I wish them good luck figuring out the actual number. I'll happily pay the penalty if they make the calculation for me and save me the trouble!

You need to pay tax on any capital gain you incurred when you converted the bitcoin to dollars to pay for that web hosting package.

For example:

On 1/1/2020 you bought $50 worth of bitcoin.

On 6/1/2020, you converted your bitcoin to dollars to pay for hosting. By that point, let's say, the price of bitcoin had doubled, so you sold half of your bitcoin to pay your $50 hosting fee, thus getting $50 for bitcoin that you bought for $25. Your taxable capital gain would be $25 ($50 - $25). (I'm assuming that even if the hosting provider accepts bitcoin as payment, the price of their services is denominated in dollars.)

The bitcoin that's left in the account (now valued at $50) is not subject to any taxes until the year when you sell or exchange it.

In general, on your 2020 tax return, you'll be reporting income (including capital gains) that you received in the 2020 calendar year.

> So why does it not list “hold” as needing reporting?

Because merely owning an asset does not create any federal tax obligations.

> If I merely own coins do I need to say yes?

The question on the form is: "At any time during 2020, did you sell, receive, send, exchange or otherwise acquire any financial interest in any virtual currency?"

So if you merely owned cryptocurrency that was acquired before 2020, the truthful answer would be "no".

As the article explains, the new thing is that on the 2020 form everyone needs to answer that question:

"The crypto question first appeared on the 2019 tax form, but on a part of the return that not all filers had to answer. Now it’s moving to the 1040’s most prominent spot, just below the taxpayer’s name and address."

Interestingly, I used taxact and taxact programmers thought that all filers had to answer that question. In case of a Yes, they added a Schedule 1 form with that question on top.

{kind=link}

Friendly reminder that IRS enforcement is one of the most cost-effective activities that the federal government can engage in, and that Congress has consistently cut funding for the IRS for years and years [0][1][2][3][4]:

Cutting the IRS budget didn’t make sense to [John Koskinen]. It was one of the few areas of government that had a positive return on investment. Koskinen told the Senate, “I don’t know any organization in my 20 years of experience in the private sector that has said, ‘I think I’ll take my revenue operation and starve it for funds.’”

It should be obvious that a politician who votes to cut IRS funding, especially when that funding can go toward enforcement, does not represent the interests of the common people they represent.

If you are a white-collar employee making $100k, $200k, or even higher, you should be especially concerned, since you bear a large portion of the nation's tax burden and expect that your tax money be spent well. 25% marginal tax rate is a bitter pill to swallow when you know that others are not paying their fair share.

[0]: https://www.cbpp.org/federal-tax/depletion-of-irs-enforcemen...

[1]: https://www.propublica.org/article/has-the-irs-hit-bottom

[2]: https://www.cnbc.com/2018/05/11/budget-cuts-shrink-the-irs-a...

[3]: https://www.theatlantic.com/politics/archive/2018/12/rich-pe...

[4]: https://www.propublica.org/article/how-the-irs-was-gutted