> Is the “dream” of homeownership really just a massive, intergenerational wealth transfer?

Yes & it has been this way since the inception of government backed loans.

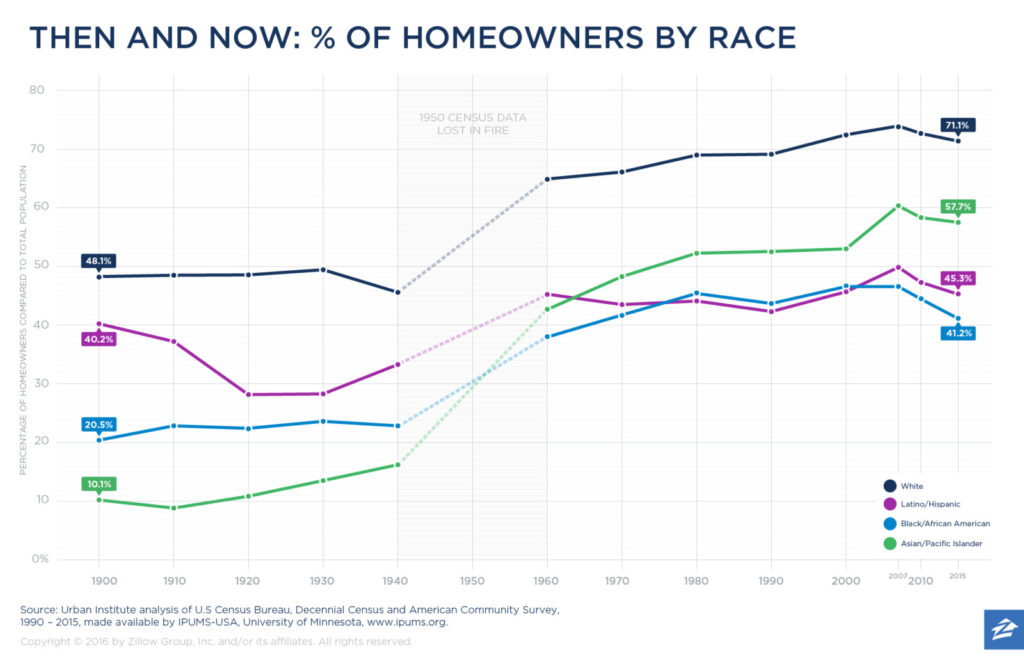

I've recently been digging into the history of housing discrimination in the US and how it relates to the racial wealth gap between blacks and whites. In my opinion there is a clear line from redlining, blockbusting, white flight & loan discrimination to the massive wealth gap among races we see today. It's quite clear to me that one of the best ways to build generational wealth is by the older generation passing off homes to the younger ones.

Theories like this one do not explain how it is that immigrant groups do reasonably well. The history of the USA is filled with people who arrive with no money, poor language skills, sometimes traumatized - and yet wind up doing well within a generation or two.

https://en.wikipedia.org/wiki/List_of_ethnic_groups_in_the_U... is a good starting point to think about. Look at groups such as Vietnamese and Cambodians. They mostly arrived in my lifetime. Everything is against them. Poor language skills, widespread PTSD from what they witnessed, no savings - pretty bad picture.

And yet, look where they are today versus blacks. How did that happen?

> And yet, look where they are today versus blacks. How did that happen?

Generally I don't like to compare the struggles amongst minorities in America. There is a multitude of factors that come into play when analyzing these types of things..

But when you look at the history of discrimination vs. black people in America you need to go back and consider the effects all the way back from slavery, to Reconstruction/Redemption, Jim Crow, discriminatory housing policy, discriminatory lending, discriminatory policing, discriminatory criminal "justice", disenfranchisement on multiple levels, lynching, etc. etc. etc. This is 400+ years of compounding discrimination against black people.

I'm not saying the Vietnamese and Cambodians (and for good measure the Irish & the Italians) did not have it bad.. but I think we need to look at this with a broader lens.

> Generally I don't like to compare the struggles amongst minorities in America. There is a multitude of factors that come into play when analyzing these types of things..

You may not like to compare, but you really should. Because when you compare you get to ask the critical question, "What things did this group do right to overcome their challenges, and can we draw lessons that help replicate that success in another group?"

When you compare blacks and whites, the differences in privilege are so obvious that you really can't see anything else that might matter. But when you compare blacks and Cambodians, privilege goes the other way - blacks have more. For all that went wrong for blacks, they generally didn't flee on boats with only the shirts on their backs after witnessing a quarter of the people that they grew up with being killed. Only to land in a country where they didn't speak the language, or understand the culture, and were generally disliked.

So what did Cambodians have in their favor?

I'm drawing from my thoughts and other comments here. The determination that it takes to be a refugee. True hope that they can create a better life. A culture of helping fellow minority members. A certainty that no matter what the frustration, it really could be worse.

Now can we encourage those attitudes in blacks? I believe so. However you don't do it by focusing on a narrative of, "Your life is hopeless because of things that happened before you were born. Things that are entirely out of your control."

> For all that went wrong for blacks, they generally didn't flee on boats with only the shirts on their backs after witnessing a quarter of the people that they grew up with being killed. Only to land in a country where they didn't speak the language, or understand the culture, and were generally disliked.

This is literally what happened through the Atlantic slave trade.. just replace "flee" w/ "were sold".

> I'm drawing from my thoughts and other comments here. The determination that it takes to be a refugee. True hope that they can create a better life. A culture of helping fellow minority members. A certainty that no matter what the frustration, it really could be worse.

> Now can we encourage those attitudes in blacks? I believe so.

I know that these characteristics have been shown time and time again within the black community. If you want to see a culture of helping fellow minority members look to the NAACP, if you want to see an example of determination please read "Up From Slavery", if you want to understand the hope to create a better life read "The Warmth of Other Suns".

My argument is not "things are out of your control" nor is it that there is something lacking in the black community that other successful minorities have demonstrated.. my argument is "here are the institutional and systemic barriers that are present -- if you want to understand the present situation and how to move forward you must understand them".

> ..."here are the institutional and systemic barriers that are present -- if you want to understand the present situation and how to move forward you must understand them"

I don't want to put words into GP's reply to you, so this is purely my interpretation of what they were saying. The standard go-to retort by advocates of black American equality when presented with examples of minority community success stories is, "So? Blacks in America have had to contend with 400 years of systemic slavery and discrimination!" The position of your argument, and others like it, is we have to "study" the barriers, we must "understand" them before we can make progress against them.

My counter-thesis is that while it is important to be cognizant of barriers, what I call "dinner table change" (the kind of changes that bring dinner to your family's table that night) comes most effectively through power, and power accrues most effectively to those minority communities who organize together culturally, socially, and economically. They work around the barriers, and undermine them over time by obsoleting them, turning them into anachronisms. There is one minority community that has powerfully proven this approach works. But it takes generations of time, and that is an unsatisfactory answer in today's climate.

I have in mind a community that endured not only slavery, but systemic discrimination for not hundreds, but thousands of years. And they made lemonade out of their sour position. The Jewish community. And many minority or disenfranchised communities can learn from the lessons Jews iterated through, found and practiced workable strategies through the millennia.

These aren't just lessons for ethnic minorities, either. The recognition of wealth inequality for example, can bind together people under that common cause into their own minority community. It is difficult to feel satisfaction of progress from signing petitions, voting, or politically participating to advocate for changes in laws, policies, and attitudes. Those activities still must be carried out, but expecting everyone who cares about such change to only channel their efforts in such manners is unrealistic. There is immense satisfaction however at a small and daily level, when for example a local minority small business serving a minority community notches up another satisfied customer.

I know there are many criticisms to this insular, tribalistic advocacy. Our outlook should be more inclusively expansive. We are better than what I am talking about. But there comes a time when the concerns of tactical survival mount to the point that it is better to acknowledge the mainstream system has failed a specific constituency (for now, hopefully), than to sacrifice the well-being of one's family, loved ones, and dear friends upon the altars of ideologies and "The Should".

There is a lot of wisdom to this. And a lot of minorities have had challenges which are now forgotten.

When we focus on things beyond our control, we create a sense of hopelessness. And the result is that we fail to do the things in our control that can create change.

Here is a lesson. If you go back 100 years ago, there was a resurgence of the KKK. The main target of their ire was NOT blacks, it was the Catholics (mostly Irish and Italian) and Jews. Their political power was such that Prohibition was passed with the main goal of giving more legal tools to discriminate against those groups. And their greatest stronghold was not in the South - it was in Oregon.

See https://www.portlandmercury.com/feature/2017/11/15/19472650/... for verification of this. My father's side of the family was Irish from Oregon. I won't forget a long conversation with my uncle about what it was like as a child growing up with concern about which neighbors might be KKK, and the importance of not drawing unwanted attention to himself at school.

Nor was this then a new conflict. The Irish largely came here as refugees from events like the Irish potato famine that happened under the long and brutal English occupation. This occupation began with English invasion in the 1100s. The conflict had been religious as well since Cromwell's put down rebellion with massacres in the mid-1600s. And then they came to the USA, a country founded and run by WASPs - White Anglo Saxon Protestants. Who knew and remembered this history of conflict as well as the Irish did.

For Catholics, the importance of JFK being elected was no different than the importance of Obama being elected to blacks. To date, JFK remains the only US President to be openly non-Protestant. Despite his family's wealth and power, he saw in the Civil Rights movement a familiar struggle.

When you study the long history of discrimination and oppression, do not satisfy yourself with only studying your own people's oppression. Understand that your story is not the only one. Learn about other people's struggles as well, learn what worked for them, and try to emulate them.

The black community has done so at points. For example the Civil Rights movement went much better in part because Martin Luther King learned from Gandhi's example and successes. However the current narrative that I see seems actively counterproductive.

You're focusing on a single variable. The above poster is recommending a multivariate approach. If a similar minority group can start from a worse position (not even knowing the language!) and advance to a better position in a single generation, then your single variable is lacking. The response of "go back 400 years" does not explain away the discrepancy. The common-sense approach is to consider other factors too.

> If a similar minority group can start from a worse position (not even knowing the language!) and advance to a better position in a single generation, then your single variable is lacking.

I can't agree with this sentence. I agree, not knowing the language puts you in a bad spot, but I think you are really underestimating the level of discrimination vs. blacks in America if you think simply "not knowing the language" is enough to put some immigrant group in a worse position than blacks in America.

I'm not sure what other variables you'd like me to use in this analysis but I think if you look back over the history of America you see that others have used one variable to levy their discrimination and it's always been race.

Are you saying present discrimination can explain the wealth gap? my initial response assumed you meant historical discrimination explains the current wealth gap. Thus, if other non-white groups can start at a similar level and attain a higher outcome, then I would posit that other variables must play a role. But maybe you're saying present discrimination (not levied at other groups) can explain it.

> others have used one variable to levy their discrimination and it's always been race

There have been countless forms of discrimination, not all of them associated with race. After all, it's imperfect people dealing with imperfect people.

Other factors I think are also relevant to present-day wealth gaps: family norms/stability (e.g. single-parent prevalence), cultural expectations, education, location. Undoubtedly these are entwined with each other and with the variable of race.

I think historical and present discrimination explains the gap, but I would say that the historical discrimination plays a bigger role because it has had time to "compound".

My general defense against the "what about other minorities" argument is that other minorities are not starting from a similar position to blacks in America and that 400 years of discrimination has compounded and sets blacks back.

The other factors would be very interesting to analyze but once again I think you would need to understand the entire history of America and racial discrimination to make a full comparison, for example:

- Family Norms / Stability: When comparing this across races you would need to take in account a few things, such as the disproportionate amount of black men who are incarcerated and how that affects family dynamics.

- Education: You would need to consider the fact that most public schools are funded via property tax, and then you would need to dig deep into housing discrimination history to see why property values in black neighborhoods are so low and why the schools are poorly funded also.. schools were segregated for a long time and are still pretty segregated now.

- Location: Most African Americans in America live in the south, which has a lower GDP than other parts of America. However, the south was once an economic power house in America... but the engine of that power house (slaves) never benefited from the wealth they generated. So that would also be interesting to analyze.

Whether you do or don't doesn't really matter. Post after post has made the point that you are focusing on a single variable and it is clear that it's not explicit causation for the effects like you claim.

There are at least two variables he's missing that matter a lot:

(1) Selection bias. The pool of immigrants who make it to America in the first place likely skews well above average.

(2) Culture/ecosystem problems in black communities, even if it's politically incorrect to argue it. Black neighborhoods are plagued by gang culture/violence, drugs, patriarchal absenteeism (estimates vary, but roughly 50% seems likely), intergenerational educational deficit (if parents are illiterate/undereducated, their children are likely to be so as well), and various other more generic issues that stem from chronic poverty.

If the level of absenteeism is very high, it is very likely that the parents are renters and not homeowners, so it circles back a little to the main point.

> If a similar minority group can start from a worse position (not even knowing the language!)

I don't know if we can say emigrating Cambodians were in a worse position than impoverished blacks . Immigrants self select for being willing to leave everything they know for the hope of a better life; they have also competently navigated a difficult process. This selection bias is accentuated in war, when the logistics of escape become trickier. Communities then cohere and reinforce each other on the other side.

Contrast that with American blacks. Captured by coastal kings who sold them to Europeans who transported them here against their wills. Any who stood up or out got eliminated. Loose to non-existent intergenerational information and wealth transfer. Et cetera

All the American blacks you refer to are dead, and can't be compared to far more recent Cambodian American immigration. Even if said blacks had wealth, its gone and irrelevant to modern blacks.

This makes even less sense than the original question.

The original poster posits a theory that generations of housing discrimination contributed to the enormous racial wealth gap. Another poster comes along and says "what about these immigrants who didn't face generations of housing discrimination?" And the conclusion of this is that the "single-variable approach" doesn't work.

It's too bad because the original point stands and in fact it's well documented in the literature. In fact an excellent book, The Color of Law [1], was recently published that shows very clearly in excruciating detail how racist policies systematically worked to deprive blacks of property and wealth.

But no, let's talk about the very different experience of the Cambodians and other minorities so we can continue to blame the blacks.

That's an uncharitable read of my comment. (Or more likely my comment was clear as mud.) As you said, the above theory was that the current wealth gap can be explained by generations of discrimination. But if another non-white group can enter at a similar "difficulty" level and attain higher results, maybe the explanation is more complicated. I think then the focus would need to be on current (possibly discriminatory) policies and factors, rather than historical ones. Education, family unit, cultural factors, etc.

What mechanism could exist for transferring poverty from slavery of ancestors to poverty of current people? The examples of immigrants seem to show it's not being born poor or having a traumatic life experience and being disadvantaged. Could it be the knowledge of the history that's holding blacks back? If everyone somehow forgot Jim Crow and slavery, would the next generation of blacks do as well as immigrants, do you think?

Also, I really think you should have some evidence at all that slavery or persecution causes intergenerational poverty after the effects have gone. I hear that theory a lot and I've never seen any science to support it. Only to support immediate poverty of the individuals who were persecuted, not their great great grandkids.

Another counterexample is Australia - founded by convicts 200 years ago and in a much shorter time, they ended up doing very well compared to blacks since slavery.

> Could it be the knowledge of the history that's holding blacks back? If everyone somehow forgot Jim Crow and slavery, would the next generation of blacks do as well as immigrants, do you think?

Forgetting Jim Crow and slavery is not enough -- this thread helps to illustrate that. The effects of Jim Crow and slavery would need to be eliminated.

> Also, I really think you should have some evidence at all that slavery or persecution causes intergenerational poverty after the effects have gone. I hear that theory a lot and I've never seen any science to support it. Only to support immediate poverty of the individuals who were persecuted, not their great great grandkids.

How could it not? I mean just think about the institution of slavery for a minute.. there was a time where the Mississippi Valley had more millionares than any other place in America.. how do you think that happened? Through slave ownership? Black families were literally torn apart generation after generation, they were denied the opportunity to realize the wealth their labor produced, generation after generation. A slave owner passes on his million dollar plantation to his children.. what does the slave pass to his child?

> Another counterexample is Australia - founded by convicts 200 years ago and in a much shorter time, they ended up doing very well compared to blacks since slavery.

Rather similar to how Native Americans are doing, I believe, not great. Their percentage of the population is similar too, around 2%?

We don't have anything comparable to black slavery. Convicts when they had served their time could integrate back into society. My great-great-x4 grandfather was a British convict who got 7 years and sent to Australia for stealing a handkerchief...

"How could it not?" isn't scientific, it's prejudice - you're assuming the conclusion. But there are so many example of it not happening. Here's another - Jews have been persecuted for centuries, kicked out of country after country, had whole families killed in the holocaust, and yet they repeatedly bounce back. Jews in Europe today are not a disadvantaged class despite their severe persecution from all sides before and during WWII.

If the effect is certain, how long does it take to wear off?

I also don't think you can ignore that the discriminatory lending, policing, and other policies also affect other minorities. The US enacted into law banning Chinese immigrants, white San Francisco was ready to mob and burn down to Chinatown at some point.

Totally agreed. I'm not trying to downplay the history of other groups in America as so much as highlighting the unique challenges that have affected black America.

The US enacted a law banning Chinese.. The state I live in (Oregon) explicit banned blacks in the constitution [0]. San Francisco was ready to mob and burn down Chinatown... "Black Wall Street" in Tusla, OK was burned down by a mob.. [1]

I did not want to get into a tit for tat comparison between oppression but I would implore anyone who is interested to really do their research on race in America.

I think you're very confused if you think other minorities faced anything like what blacks faced. Combined this with the well-known fact that most recent non-Mexican immigrants to America (after 1960) were often quite wealthy before they came to America and you're looking at a very different experience.

For the record I have family members living on reservations. Go back a little over a century ago, and natives were hunted for sport, like game animals. It was only 40 years ago that the USA officially discontinued policies of forcibly removing children from their homes and putting them into schools where they were mistreated. I personally know people who were beaten as children for speaking in their native language. Abuse and prejudice remain facts of daily life.

There's a pattern that you see emerging in "late-stage" immigrants that are no longer found amongst other minorities in the United States. I believe that this pattern, where minorities share risk to bring about equal success and growth, stems completely from the racial divide that other minority groups in the US have had to fight against. An excellent example of this is immigrants who come to the US, ally with others of the same minority, share housing (even sometimes to the point of breaking the law), start businesses (while breaking several laws along the way), and then bring more immigrants in to help grow the business and then distribute that wealth to those involved. It's very similar to what happened in early European immigration to the US except that these "late stage" immigrants now know exactly what to avoid. They're able to take in all the advantages of being an immigrant while ignoring/offloading the risks associated with breaking the law. There's a reason that a stereotype exists regarding Vietnamese nail salons and, however inaccurate the stereotype may be, it started from this pattern of Vietnamese immigrants moving to the US, starting up nail salons, and bringing in hundreds more Vietnamese immigrants to grow these businesses while sheltering illegal practices that could be hidden by the growth of the business.

Minorities that are already in the United States don't have the ability nor the structure to make this a reality.

You’re comparing a massive group of people with a comparatively tiny group of people that have self selected for only the most willing and capable of abandoning everything and building a new life from nothing after qualifying to enter the United States. Of course those people are going to be more successful. That alone discredits the point you’re making.

> Everything is against them. Poor language skills, widespread PTSD from what they witnessed, no savings - pretty bad picture.

A lot against them, but a lot of important factors working for them too. For one thing, their family and community structure remained intact, allowing them to build community capital.

Also, because they are Asian, they benefit from the beneficial stereotypes of Asian Americans in educational and business environments AKA "the model minority" myth, and don't experience the presumption of criminality that blacks are often subjected to to this day.

As others have stated, they were also a self selecting group who were fleeing a single acute experience of trauma due to the war vs the intergenerational and normalized trauma of slavery and segregation that blacks face. And to add to that, they arrived with a strong work ethic, but at a time when many immigrant groups landing in the US were doing well. They weren't redlined. Their children weren't excluded from white neighborhoods and schools.

I, as an Asian American, grew up in in a 90% white city with excellent schools, but with a conspicuous lack of black people around. No segregation for me, but it was there if you were black.

None of this is to say Vietnamese and Cambodians had it easy at all. In fact, they are still poorer on average than other immigrant groups who arrived around the same time with better circumstances, like Indians, Taiwanese, etc. That's who you should be comparing them to to understand the effects of disadvantages.

Can you explain this? Why would compound debt exist for blacks but not for anyone else? Why would poor American whites be labeled under "compound interest"?

Again, it is a metaphor, don't take to too literally.

Blacks were slaves, whites and immigrants were not.

Can you picture slavery as digging out of a hole (debt)? Until breaking even, you are subject to compound debt.

Yes, immigrants do well within a generation or two. Blacks have only had civil rights for a generation. White males not only have always rights but made them.

Yes, I'm generalizing based on skin color. That is literally what race is.

I think the idea is, poor whites don't need to pass through institutional racism like poor/rich black do. Of course poor whites have it worse than rich whites but they have more/easier opportunities to break through.

Who arrived with no money, poor language skills... and were not pushed into redlined neighborhoods, were not denied credit, and were not rewarded with dropping property values around them as soon as they bought a house and the white folks left.

Immigrants (especially non-White) faced their own challenges, but not those ones.

I hate how statistics are used to bludgeon people. Anytime an article comes out about economic inequality is posted I see the same familiar pattern. Issue is presented, black people are compared to everyone, shit on, dick measuring about how everyone else is killing it in SV (and of course everything (status-quo) is okay), rinse and repeat.

In the mean time: ecology is in decline, trust in science is on the decline, democracy is in decline, wealth inequality is increasing and accelerating. The emperor has no clothes. Wake up!

Anyone know what that looks like if showing person-years instead of years? Curious the effect that integrating over population would have. Could imagine integrating over some inflation or return measures too.

>And yet, look where they are today versus blacks. How did that happen?

All blacks? Methinks you've tipped your hand.

I'll indulge you though and wonder, bemusedly, if immigrants have different social structures and expectations of a country than a formerly enslaved ethnic minority whose social cohesion and family structures have been systematically dismantled and obliterated. Whose social traditions and cultural ties have been intentionally wiped out for centuries?

Could an immigrant's cultural identity and ties to other immigrants with shared goals and expectations allow for a beneficial cooperative framework wherein alternative banking and lending structures are available to the newly arrived?

Could a society that still murders members of its citizenry disproportionately due to their ethnic and historical legacy (and a legacy no fault their own) really offer a framework beyond simple survival to such a minority?

Could the difference between being a foreigner in your new home and a "foreigner" in your own actual home country encourage different outcomes?

It’s because the Cambodians here are a self selected of people who were willing and able (whether money, family support, or hustling skills) to start their lives anew. The blacks are descendants of people forcefully abducted, who were selected mostly for physical traits.

The constant among Vietnamese, Cambodian, Japanese, Korean and other cultures is a really strong family unit. Family owned businesses, parents working hard to educate kids, parents holding high expectations for children etc.

Both political parties in this country seem to undermine black families, Conservatives through thinly concealed racist policies and the war on drugs, Liberals through social programs that foster dependence on government rather than elevation to independence.

I've said it before, but the millennial generation will not be kind to boomers when the history books are written. Our parents have basically fucked us over in a million different ways, but especially with housing. I see a ton of boomers who have basically shredded the economy by creating multiple bubbles in the stock market and housing, destabilized the middle east and thrust us into many unwinnable wars, blown through all the home equity they had with home equity credit lines, never saved for retirement, and now expect to be taken care of by social security and medicaid during retirement.

This is apparently what happens when you have a strong cultural revolution during the 60s, but everyone grows up and gets greedy. Although I'm not too optimistic the millennial generation won't do the same exact thing when they turn 40...

The middle east was destabilized before most Boomers were born or when they were young children. Blaming grandma for people fighting in the Middle East is ridiculous.

> expect to be taken care of by social security and medicaid during retirement.

Social Security was created in 1935 before a single Boomer was born. Medicaid was created in 1965. Boomers would at most be 20 years old or at minimum 1.

> thrust us into many unwinnable wars

Young people actually supported the Iraq War at a higher rate than did older Americans.

Yea, this article is really not surprising to anyone who isn't a boomer. I look around and see smart, hardworking people with some of the "best" jobs in the nation (doctors, lawyers, programmers, etc.) who can't afford to buy a home. Between student debt, the cost of living, nearly 50% taxation (and rising in CA), wage stagnation, and real estate greed... it's nearly impossible even for those young people who are doing well. If you ask me, the boomer generation certainly left it (far) worse than they found it.

Thanks, boomers, for de-regulating banks, leading to financial instability that continues to this day.

Thanks, boomers, for the 2007 Great Recession.

Thanks, boomers, for buying up homes in 2008 at a discount, and selling it back to the next generation at an exorbitant price. Your "investment" is literally why we have a housing crisis.

Thanks, boomers, for the massive mismanagement of federal, and local governments.

Thanks for the wars, boomers.

Thanks, boomers, for some historical wage stagnation.

It's no surprise that people are struggling to afford a home, and waiting to start a family.

> Yea, this article is really not surprising to anyone who isn't a boomer. I look around and see smart, hardworking people with some of the "best" jobs in the nation (doctors, lawyers, programmers, etc.) who can't afford to buy a home. Between student debt, the cost of living, nearly 50% taxation (and rising in CA), wage stagnation, and real estate greed... it's nearly impossible even for those young people who are doing well. If you ask me, the boomer generation certainly left it (far) worse than they found it.

Is this a national problem you're seeing, or one specific to CA/NYC/etc.? I suspect it much be a local problem, since I can't see doctors, lawyers, and programmers having a hard time affording a home outside a few very specific locations.

I think the issue of wage stagnation, student debt, and all the issues that come with the wars and poor government management are felt across the nation by young people.

That said, I think the housing "crisis" is really specific to certain areas. In CA what we're seeing is that it's very hard to afford a home in certain areas.

I think there is some truth to this for sure. But speaking from a here and now perspective it’s hard to not take this stance. My wife and I make a good bit more than the average income for our area and at 27 we aren’t going to be even close to affording the house I was born into. That house was bought by my parents at 23 with my father working part time.

The creation of the automobile opened up a ton of land for new, cheap housing. That lasted for a few decades, but the land is now developed and the population is much larger and evermore urban, so the gold rush is over.

There may be a chance to develop our way to cheaper housing, but you'll be getting less land and less space for more money.

Agreed, there are timeliness and environmental variables to living costs and land for sure. The fear here seems to be that being a doctor or lawyer to use the cliche won’t secure you housing and that landowner becomes a profession that trumps all in terms of income and social class. I don’t mean this to be disingenuous I realize thats always been true to a certain extent but the extent is important.

My wife and I hold "great" jobs right now. Some of the best in the nation. Yet we can't afford anything close to what our parents could when they were 10 years younger than we are now.

And it just pisses me off to no end when we see shit like this from the boomers:

"A particularly potent political grouping would be for older people, particularly retirees, to team up with young people on economic issues. So it’s not surprising that some political mavens are trying to make sure that doesn’t happen. One of the strategies of the plutocrats comes from financier Jay Gould : “I can hire one half of the working class to kill the other half,” except this time, they aren’t even having to hire one half to turn it against the other.

Just as I’ve noticed an sharp uptick in women’s identity articles, I’ve also seen a ramping up of generational warfare and anti-baby-boomer messaging (I have as much antipathy towards broad comments about baby boomers as I do women). This phenomenon admittedly has deeper roots, since billionaire Pete Peterson has been campaigning against Social Security and Medicare since the mid 1980s, and presenting old people as something society can’t afford is part of his strategy. But he’s been joined by fresh troops, such as Fix the Debt and billionaire Stan Druckenmiller’s overt campaign to turn young people against older ones, The Can Kicks Back."

Wouldn't white flight followed by re-urbanization favor people of color in terms of home value?

I know in my city the neighborhood that historically had high black homeownership levels now has a million-dollar entry fee. Meanwhile the suburbs are undesirable and cheap.

No, because what do you think those white people fleeing to the suburbs in the 80s and 90s did? They didn't sell homes to minority homeowners because the banks wouldn't give minorities loans. They either sold to other white landlords, or became landlords themselves.

So, the million dollar apartments are owned by wealthy white landlords who have realized 100% of the appreciation, while systematically pushing poorer minorities, who are almost 100% renters, out to even worse ghettos.

This is a tricky question for me to answer because I've been doing more research on the "back end" aka why minorities weren't getting housing as opposed to what's happening now w/ re-urbanization.

Part of it is that many homes sold during the white flight and blockbusting era did not go to minorities, there were explicit causes in the sale to prevent this. Another part of this is the fact that minorities who did buy bought "on contract" which means that they did not owe a mortgage to a bank but to an individual (who most likely was a blockbuster) they did not build equity (wealth) and were subject to very harsh loans. I don't know what percentage of homes sold to minorities during this era were "on contract" so it's hard to quantify the effect.

Based on an anecdote it's definitely true that some amount of minorities benefited from re-urbanization.. I was in NE Portland a few weeks ago and had a very interesting conversation w/ a local Uber driver who lamented the fact that his family had sold his grandmothers place in the 90s, this home has probably appreciated at least 3-4x since then.

> In my opinion there is a clear line from redlining, blockbusting, white flight & loan discrimination to the massive wealth gap among races we see today

Yes! And due to inheritance, wealth propagates within racial lines. White families build wealth subsidized by the government and have white kids, who have a huge advantage over non-whites due to the historical wealth accumulated.

It is a self-reinforcing and self-propagating process, and now, old whites use zoning laws to extract value from younger generations, particularly non-whites and poor whites, whose families don't own real estate.

Out of curiosity... forgetting rates for a moment and just checking on numbers of people, aren't there more white people in abject poverty than black people entirely in the USA?

Seems if the argument is that white wealth propagates - that there should be few poor white people anywhere. There has been no racism towards them, and lots of time to build up the "subsidized wealth".

I'm not crazy about all this generalization based on skin color.

> Out of curiosity... forgetting rates for a moment and just checking on numbers of people, aren't there more white people in abject poverty than black people entirely in the USA?

Yes, but that is irrelevant. Poverty rate is 9% for whites, 22% for blacks.

> Seems if the argument is that white wealth propagates - that there should be few poor white people anywhere. There has been no racism towards them, and lots of time to build up the "subsidized wealth".

There are fewer poor white people. The problem is that racism isn't the only factor in play here. Bad education, healthcare, etc. contribute to inequality.

There are issues in play both intra and inter races. As outright racially-driven policies were revoked, whites turned to using wealth as a way to block blacks, resulting in the side effect of punishing poor whites as well.

> I'm not crazy about all this generalization based on skin color.

This isn't generalization. Read the redlining maps. Look at household wealth broken by race, the difference is even sharper than income:

The reality is that the house is sold to cover the cost of a nursing home, or that a reverse mortgage is used to convert that value into living expenses, or that the older generation dies with home equity loans that were taken out to cover expenses.

> In my opinion there is a clear line from redlining, blockbusting, white flight & loan discrimination to the massive wealth gap among races we see today.

Yes. See: "The Color of Law" - https://amzn.to/2JlHvRT extensively well documented. It's depressing reading though.

> As we’ve pointed out at City Observatory, there’s an inherent contradiction between the goals of promoting housing affordability and using homeownership as a wealth building strategy. Affordability requires that housing be stable in price; a good investment needs to appreciate. If housing is a great investment, its because its becoming less affordable. If housing stays affordable, it is, by definition, not an investment that generates gains.

I have thought about this before and really think we should stop treating home ownership as an investment. However, I can't think of a way to do that which is fair to those who bought homes already..

Why does policy need to be "fair" to investors? New government policies move asset values (including real estate values!) in both directions all the time. Investors -- including homeowners -- are not entitled to an investment that always appreciates.

This belief that we cannot do a thing unless that thing benefits wealthy homeowners is harmful.

In this case I believe it would have to be "fair" due to the political power of home owners in most areas of the United States. The fastest way to lose every vote from Suburbia is to lower the value of their greatest investment.

And this is how we get real estate bubbles. It’s already back to the “it’ll always go up” stage even after 2007, in most areas with decent jobs that might afford some security or ability to pay mortgages.

As a general rule of thumb, screwing people by changing the rules on them harms investor confidence. The promise of future stability is an underrated part of our economy. See the FDIC. This is why many legal changes go to great pains to grandfather the old rules.

That's not to say the rules could never be changed. But just imagine being, for example, a small time landlord in the UK. Recently the rules changed, and you can no longer deduct mortgage interest as an operating expense from the rents you collect. Old mortgages are not grandfathered. This means a lot of existing rentals are suddenly & out of nowhere going to be losing their owners money. Thanks, government. Maybe it needed to happen, but it's a bit chilling to have that kind of rule change happen on you.

I guess this is just an ethical question? I don't think it would be fair to those who recently bought a home if we just wiped out a substantial proportion of their assets.

> This belief that we cannot do a thing unless that thing benefits wealthy homeowners is harmful.

You perhaps misinterpreted my comment. I don't think they will benefit at all from a solution, but I would think a good solution should not be too devastating to any given person.

I'm less concerned about wealthy home owners than I am for those who just got a mortgage.

I agree why don't we just make a extremely burdensome property tax for non-primary residence properties that are not worked/workable land such a farm land? Maybe 5x property tax on your second property, 10x on your third, etc. Maybe it only kicks in and ramps up after a set number of months to allow developers to buy properties and develop them for sale but make it hard to hold them for too long in order to get a 'legit' owner in the house who will actually make it their home.

Relaxing zoning rules is an "easy" one. It doesn't deprive anyone of a home.

Alternatively, if you want to get a bit more radical we could turn all property ownership into 99 year leases from the state, as is the case in Singapore, potentially reducing the length of time on leases over time to spread out the pain. Though it would be a long process.

I would also support legislation that reduces transaction costs on buying/selling homes, which actually suppresses the price of homes because it takes a longer term commitment for buying to make sense.

Yes, this is unfortunately one of the great mistakes (or intentional deeds, depending on how you look at it) of US economic policy of the last few decades.

> I have thought about this before and really think we should stop treating home ownership as an investment. However, I can't think of a way to do that which is fair to those who bought homes already..

Correction: fair to those who bought homes recently, rather than 20 years ago and are sitting on top of unrealized capital gains.

Levy solid capital gains taxes retrospectively, use that money to compensate recent buyers. Those that made a killing are still ahead (although less so), those that made losses are compensated.

I guess my first question is, when we say home ownership is a good investment, do we mean it will make you rich? Or that it will keep up with inflation and be cheaper than renting in the long term?

The latter is hardly incompatible with affordability, and can still be considered a sound investment.

Yes this article makes some good points but the rhetoric is all wrong. Here, this guy says it much better than I can:

>Home is where the cartel is. I use the word “home” not “housing” advisedly. Homeowners understand their actions not as monopolizing the housing market but as protecting their homes and neighborhoods from the market. The libertarian “deregulatory” rhetoric by which market urbanists sometimes make their case is counterproductive. Telling people to think of their homes as a commodity upon which market forces should be brought to bear in order to ensure production of housing services at competitive prices is obtuse. People purchase property, rather than renting, largely to gain security and control, to escape the vicissitudes of the market. The worst place to emphasize “deregulation” is in dense urban environments, where almost every sort of action has spillovers.

Policies like up/rezoning which decrease current home prices in order to lower rents are directly redistributionary and I think you have to make your case in those terms and I just don't find redistribution on the basis of age that convincing.

When you have an asset with minimal elasticity in supply (such as housing in areas where building more is difficult) that is nevertheless needed for survival, owners of that asset will be able to capture most of the productive capacity of the people who need that asset. In areas with high productivity and high incomes - like around rich coastal cities - that's manifested by skyrocketing housing prices. In areas with lower productivity and lower incomes, prices still go up, but not as much, and the effect is felt as an inability to get ahead or even make ends meet even when you work hard. The wealth generated by younger laborers is transferred to older asset-owners who own the necessities of life, simply because they continue to own them.

Similarly, classical economics predicts a substitution effect for these goods: as they become increasingly less affordable, buyers will try to bypass the market entirely.

That's behind nearly all the social changes and huge tech businesses of the last two decades. Can't find a place to live? Rent in a tiny apartment instead of buying a house.

Live out of a van. Move to cheaper locales while working remotely. Can't get a job because that's yet another scarce resource monopolized by an older generation? Drive people around in your car with Uber. Sublet your rental on AirBnB. Blog for advertising revenue. Sell your crafts on Etsy. Start a new service business and advertise on Facebook or Google. Take funding from YCombinator and try to start the next great marketplace.

The last couple years have brought even more radical examples, eg. Bitcoin is basically an attempt to setup a shadow financial & monetary system and opt out of the dollar-denominated economy entirely.

Yeah, this is not predicted by classical economics.

Westerners really need to look at other countries. You do not see these sorts of extreme housing shortages in Asia. You don't see it in Tokyo, Bangkok, Shanghai, or Seoul. I have trouble even explaining what's happening in places like San Francisco or London or Paris to my Asian partners. That's because Asian cities aren't afraid to grow. Tokyo, Bangkok -- these cities have grown enormously and continue to do so [1].

Ultimately, the West has collectively decided to tombstone their cities. There is enormous demand to live in the West's metro centers and yet, at virtually all levels, powerful forces work to ensure that these cities do not expand to satisfy this demand. This decision not to grow is very much a political decision.

The end result here probably won't be good. A great deal of economic growth is being left on table. Cities are the primary engines of economic growth and when they aren't allowed to grow the result is less growth and opportunity. Political instability ticks up; a great deal of many people stuck languishing in less dynamic areas because they can't afford to move to the dynamic cities end up feeling like they're stuck and now want to tear the whole system down. Democracy itself breaks down as the urban-rural divide becomes more and more severe.

But hey, in the short term, those who bought early get rich.

Monopoly is well-treated in classical economics, and this is an instance of zoning regulations enforcing an artificial monopoly. And the results are exactly as predicted in a microeconomics textbook: owners of the monopoly asset capture nearly all economic surplus from trade in it.

economics posits that individuals are rational actors, not that societies always make good collective decisions, and further economics describes many conditions under which collective decision-making can end up disastrous for all involved despite or because of each individual acting in their best interest along the way.

This isn’t predicted by classical economics. This is the result of the housing supply being artificially constrained by zoning laws. If developers could build a 40-story high rise next to a single family home, housing would be dirt cheap. On top of this, rent control further disincentives developers from constructing new properties.

AirBnB and Uber aren’t “bypassing the market”, they’re bypassing local laws and ordinances. The reason why AirBnB is cheaper than hotels and Uber is cheaper than taxis is because they don’t incur the cost of regulatory compliance. Real estate would also be cheaper if developers didn’t have to comply with zoning regulations.

Still predicted by classical economics. Zoning laws change the elasticity of supply. Housing in a completely free market should have relatively high elasticity; if the price is too high, build more! Zoning laws artificially constrain the supply and so create a monopoly/oligopoly situation, which is what allows owners to charge economic rents beyond the marginal cost of producing more housing.

Similarly, the local sublet/taxi regulations that AirBnB/Uber bypass artificially constrain supply, allowing owners of properties or taxi medallions to charge economic rents. Bypass them and you get a competitive market, where owners of houses & cars can charge only the marginal cost of use (and instead, AirBnB and Uber get to charge monopoly rents).

I once made the observation that much of the older generation’s net worth is tied intimately with their homes. That if we exclude home equity, the resulting net worth is very little — demonstrating a pattern of poor savings habit and investing. Unfortunately, for the younger generations, they will have to be much more diligent savers and investors as they are now fighting asset price inflation — a problem previous generations didn’t have as much.

To be fair, the people who have massive housing equity generally bought their houses when interest rates were sky high. In the 1970's, when you could buy a decent house in Palo Alto for $50,000, the interests rates were 15-20%. As rates have gone down, the prices have gone up. Mortgage payments as a fraction of income have gone up much less dramatically than the sales prices.

An extended low-interest rate environment is a (the?) major factor in increasing income inequality. Assets become much more expensive, benefiting owners (in this case, of houses and real estate) and hurting those who strive to own. Further, savers are generally barely breaking even with inflation, which leads to less saving.

Low interest rates "stimulate the economy" which means those who already have (applicable to both people and companies), can borrow more and multiply their assets much more rapidly than those who don't have, can catch up.

Sure, but high interest rates make money more expensive, meaning less people can afford less house. A factor that impacts people who need to borrow the most (the non rich).

So what's better, high asset prices or high borrowing costs? Something tells me they both even out painfully.

Not true, as home prices key around monthly payment, so high rates put downward pressure on prices to keep the monthly payment relatively constant.

When long-term risk-free rates are exceptionally low, capital seeks excess return, much of which gets invested in real estate, increasing demand and prices. When the risk-free rate is 7, 8, 9% on a 10Y bond, then messy, illiquid, physical real estate is far less desirable as an investment.

The original article was about income inequality -- when average Joe can easily borrow $300k for a house, the average company can easily borrow $300 million or $3 billion to get larger, buy competitors, execute LBO's, etc... all of which consolidate power and capital among the wealthiest and ultimately reduce labor opportunities for everybody else.

Not true, as home prices key around monthly payment, so high rates put downward pressure on prices to keep the monthly payment relatively constant.

When long-term risk-free rates are exceptionally low, capital seeks excess return, much of which gets invested in real estate, increasing demand and prices. When the risk-free rate is 7, 8, 9% on a 10Y bond, then messy, illiquid, physical real estate is far less desirable as an investment.

That's just one factor. Another is this. When interests rates go up, the reason why price pressure is down in the first place is that fewer buyers can afford fewer houses; in other words, sales go down. This is already happening today (https://www.bloomberg.com/news/articles/2018-04-25/are-risin... <-- today's article). When sales go down, sure, there's downward price pressure. But by that time, contrary to what you seem to be suggesting, the little guy doesn't necessarily benefit (because borrowing costs can be out of reach). And worse: if they go down far enough, it could bring some people underwater, which as we saw from the last cycle disproportionately impacted the lower middle class. And even worse: any home equity line of credit that has a balance is going to be more expensive to pay back.

The original article was about income inequality -- when average Joe can easily borrow $300k for a house, the average company can easily borrow $300 million or $3 billion to get larger, buy competitors, execute LBO's, etc... all of which consolidate power and capital among the wealthiest and ultimately reduce labor opportunities for everybody else.

Yes, the original article was about income inequality. And I've addressed these above, using different factors than the ones you've honed in on (capital concentration). I have news for you, capital concentration still leads to inequality during times of cheaper housing. You're making a mistake by thinking higher interest rates will make a big dent here: Blackstone and American Homes 4 Rent have sources of cash that you and I don't have (IPOs, bonds, to name some, I am sure there are many more).

In a capitalist system (that is not collapsing), income inequality will always trend upwards, high interest rates won't stop it. However, low interest rates accelerate the increase in inequality.

Income inequality has expanded at an unprecedented pace in the past 10 years, during which, global interest rates have been the lowest they've ever been.

I must be missing something in this article. It seems to say that older generations have more net worth than younger generations. Its graph depicting net worth by age scales almost linearly. Isn't this how it's supposed to work?

If I encounter someone who has spent a year digging a hole, another person who has spent two years digging a hole, and another person who has spent ten years digging a hole, I suspect that each respective hole's depth would be roughly proportional to the length of time spent digging it. The same concept applies to years making income. Clearly this isn't ubiquitous, since it's only possible to gain wealth if you make enough money to save wealth, but one could argue using this data that it's actually the norm.

People should start spending their retirement at some point. The article points out that in the 80s, the 45-65 group had the most money, more than the 65+ group. But apparently older people are now hanging onto their still-appreciating homes, and only when they die will they pass on their homes to their (also now aging) children.

I think it's more those with more money can influence lawmakers to make rules more hospitable for making more money. That would explain something like this happening for a long time, that would not be explained by a high percentage of home owners being voters (when it's one big company that owns a lot of homes):

https://www.theatlantic.com/business/archive/2018/04/rent-to...

Regulations like mandatory minimum lot sizes and density restrictions make it a lot harder for younger people to buy their own piece of the ownership pie, which creates scarcity, which in turn causes property values to skyrocket even further. I can’t help but see this as a form of regulatory capture.

The price of a house goes up.

It’s called appreciation, but it mimics inflation much more. Except in certain volatile areas, housing has not been an inordinately good investment, but it is an inflation hedge. Housing is illiquid, does indeed depreciate, and often must be relinquished to be “spent.” Lack of savings or income so low it precludes savings are more important than housing as a source of inequality.

This! The inflation hedge also makes the wealth gap exponential for those without the capital to get in the real estate game for lack of a better term. The capital needed to get into a home with traditional financing seems to go up by the month and is essentially moving the finishing line for those millenials saving for homes.

- divorce/single head-of-household rate. Over 75 probably has a much higher marriage rate than younger. If you divide that wealth into two households, how does it look?

- shift to private ownership of retirement accounts. In 1989, pension plans, etc., were much more common. These wouldn't count as personal wealth as they are income-maintenance, rather than an asset.

It all comes down to supply: why is this such a hard concept for people to understand. It's not old people's fault, unless they're the voters who keep preventing housing from being built. When you limit supply, prices MUST go up: there's no other way it can go.

The other big problem is fundamentally: regulations that drive up costs for developers: everything from impact fees, to zoning, etc. We need to start working with developers to drive down costs and increase competition: that, plus vast amounts of building will drive down costs.

Current homeowners are incentivized to always vote for their property values to go up - so they always vote to prevent new housing to be built, in the name of neighborhood character.

Where I live in Southern California the problem is that supply is kept down by people renting out their first home and buying a 2nd. The houses appreciate at 4% per year and the rent increases at nearly 8% so it's win win for owners. On the flip side renters continue to spend their money renting and paying the mortgage of their landlords. The 2010 census reported Irvine was nearly 50% rentals [1].. In one of the largest planned communities in the US that is a problem.

Putting the contradiction of an "affordable investment" aside and looking at the high prices: couldn't local governments change zoning laws to encourage building more homes to lower prices? More supply lowers prices right?

They certainly could, but they'd be fighting the, generally very politically active, current homeowners every step of the way. Increasing supply will reduce their property values.

Proponents of building more housing need to step up their political activism to match the NIMBY crowd.

Housing is both mandatory and the largest expense for nearly everyone. It's a tremendous damper on "spending less." If the secret to wealth was easy when those books were written decades ago, it is much less easy now.

What you musn't lose sight of is the effect of the prolonged low interest rate environment on asset prices. Money is cheaper to borrow so zero-sum competition for things like good schools drives prices up. The beneficiaries of this are older people who owned property before the low interest rate environment. The people who'll pay for it are those who are buying now, and will continue to pay well into the future. Thus the inter-generational transfer of unearned wealth.

That's not really true (something that land value tax advocates will gladly point out) because supply of housing is fixed in the short term. Landlords charge what the market will bear for housing; rent isn't anchored to their actual costs. They bear the burden of increasing costs.

There is a risk that property tax could suppress supply of housing in the long term, since it makes rentals as investment vehicles less profitable, and therefore indirectly contribute to increasing rents.

In my high COL area, renting is definitely cheaper than owning, at least with regard to small condos that I look for. Foreign and older buyers have pushed up the price of condos as rental properties, but now there is a glut, and they must rent at the price the market will bare, which has absolutely nothing to do with their actual costs, but instead what the average 30 year old can afford here.

And in my city, there simply aren't enough millenials able to buy these high priced condos ($300K + $800 in HOA / taxes per month). Thus the rent gets pushed down to $1500, which is way less than it'd cost to buy, and is definitely a money-loser for many of the owners after paying interest, management fees, taxes, HOAs, etc.

I’m not comparing it to the cost of renting, I’m simply saying that when I sell my home for $200,000 having bought it in the 1970s, at best it will be nearly break even.

But you also have to calculate the opportunity cost of having a bunch of money sunk in an asset that (apparently) didn't perform spectacularly. By renting he could have invested that $200k in an S&P 500 index fund. Assuming he bought his house today in 1978, the S&P 500 increased over 27x ($97 on 4/23/1978, and $2670 today), plus he would have got about 2% dividends. I'm guessing his house didn't cost $7400 in 1978 (not to mention the 1 - 2% "dividend" he paid the government in property taxes), so I'd say renting isn't obviously worse. Depends on the rent.

Renting doesn't magically mean you have additional money to invest. The only opportunity cost to factor is the value of the down payment. But you also need to consider their cash flow as rents rose and their mortgage payment remained mostly the same or dropped as they refinanced plus now that they own their home outright.

So why are housing prices rising? Maybe it’s the young people willing to pay ever increasing prices. Maybe they are responsible for shooting themselves in the foot?

low interest rates + rising wages. it seems like people will buy as much home as they can afford. so yes, in a sense, people are collectively shooting themselves in the foot by leveraging their homes as much as possible, but then again you need a place to live.

For centuries prior the elderly were subjugated to the mercy of the young (like many Asian economies and as one could imagine in primate hierarchy groups), due to physical labor being the largest source of wealth. In contemporary society, the contrary is true given that physical labor has been a diminishing source of wealth. Today's economy is one where experience and knowledge triumphs, as physical labor is rapidly replaced through automation. Society is still far from it, but as close to a meritocracy as it has ever been.

For many centuries, land ownership was (and in fact still is) the largest source of wealth. Historically, it conferred not only wealth but also power. This was the key characteristic of the feudal system.

Land is a store of wealth, that's not the source of wealth. If we look at the Forbes top 20 richest people compilation, we would be hard pressed to point out anyone who made the majority of their wealth through land.

Except over time the young will find it less and less likely that they'll be able to afford a home, up until it's impossible or the system breaks entirely...

Or what the article and research by AEI and Thomas Sowell has implied: you'll be able to afford a house when you're older since nowadays you become more valuable the more knowledge you gain.

{kind=link}

{kind=link}

Yes & it has been this way since the inception of government backed loans.

I've recently been digging into the history of housing discrimination in the US and how it relates to the racial wealth gap between blacks and whites. In my opinion there is a clear line from redlining, blockbusting, white flight & loan discrimination to the massive wealth gap among races we see today. It's quite clear to me that one of the best ways to build generational wealth is by the older generation passing off homes to the younger ones.