"More than 200,000 civil servants became eligible to retire at 55 — and in many cases collect more than half their highest salary for life. California Highway Patrol officers could retire at 50 and receive as much as 90% of their peak pay for as long as they lived."

It is simply not possible economically to support these type of benefits. Look no further than the Greece or Italian austerity crisis to see how these type of government payments will play out.

It's the same in every country: Some historical group's advantage can't be removed because they are enough people to get leverage against any opponent. There's a need for a new advance in democracy, because it has almost-bankrupted a few countries now (including Greece). Perhaps the separation of powers in our democracies (executive, judicial and law-makers) isn't enough. Maybe we should add a 4th weight, which translates hard limits from nature into limits that politics can't cross: "You can't allow a global warming", "You can't increase debt beyond 4%", "You can't let people work dramatically less for 5 decades (like in Greece), unless you justify it with an incredible progress in NGP/GDP/technology" or "You can't have discrepancies between public and private sectors". Somehow I'm happy Europe provides a bit of pushback against my country (France) because God knows how much debt our politics would otherwise subscribe.

How about we weight people's vote by an estimate of how long they've got left to live? After all, the longer into the future you'll live, the more seriously you have to take it.

I see several thoughts about that interesting proposal(offhand and only related to USA):

1) Those that have participated in government/military have less say than when they served. This could be a positive, but I feel some objection to a POW (my grandfather for instance) having less say than someone who didn't serve.

2) Do _really_ we want the least experienced citizens having the most say? The US already has age limits for certain offices so that sort of reduces my concerns about this, but...

3) Phase in plan? Currently voting is dominated by older voters. I don't see those people rushing to their polling places to vote to have the value of their vote lessened. Could be interesting to see the reasoning that happens for people to vote for or against it from a game theory perspective.

> 2) Do _really_ we want the least experienced citizens having the most say?

That's the first thing that I thought of, but then I realized that I have a pretty dim view of the 'experience' of most older people that I know. They are woefully unable to use computers, and on account of their 'trust' in things like fake news they seem incredibly unprepared to deal with our current reality and are just as susceptible - if not moreso - to populism. And while this is a bold claim I'm not quite prepared to defend, they seem quite a bit more selfish and materialistic than the twenty-somethings I spend much of my time with.

Maybe in times of rapid change like ours, 'experience' doesn't mean as much as it once did.

Plus, it goes both ways. If we should defer to those with more experience, it's only fair that they should take better care of their offspring.

There was a fascinating discussion about Greece on HN about a month ago. Based on what some Greek posters were saying, it seemed like the Government has effectively nationalized the housing market by raising property taxes to 5-6% (through purposefully inflated appraisals). If you're a Government in desperate need of revenue then it makes sense, as land and houses are the only assets you can't move out of the country. That may be the endgame for many of these heavily indebted cities, states and countries.

Honestly, this has been one of the reasons I've chosen to avoid buying a home even though I could easily afford it now.

Seems like, besides lack of mobility in a era of never stable employers, owning a home essentially weds you to your locality's debts - unfunded bonds, pensions, etc. You can already see how cities with the biggest problems - Chicago, Detroit - are already cracking. They went for the easy things first: traffic cameras, cigarette taxes, huge tourist taxes on rental cars and hotels.

But eventually they'll come after the biggest cash cow which is property taxes.

> But eventually they'll come after the biggest cash cow which is property taxes.

I sure hope so. Actually, scratch that, I'm not sure. It might affect people that I don't want it to affect. It's probably complicated (so by all means enlighten me).

I'm all for someone buying a house and being able to keep it and live in it. But what bothers me to no end is that every single house I've lived in, renting a room for pretty steep prices what with wanting to live in a city, involved a landlord who made a good deal of money on me and my fellow renters, and for no reason other than buying or renting the house a long time ago when it was still cheap.

My previous landlord made a profit on the rent-controlled apartment he snagged a decade or so ago. While the rent is a significant portion of our income, he makes a profit and gets to kick us out (in a friendly way) once he wants it back. The fact that this guy was a major squatter back in the day only makes this more frustrating.

My current landlord does fuck-all and has some kind of disability that has kept him from working for a while. I'm pretty sure that the rent I pay at the very least pays his mortgage, and perhaps even leaves him with some profit, all because he's older and he got there first. Meanwhile I, in my early thirties, am paying a significant sum just to be able to live in 'the city'.

I'm happy he's got a place, don't get me wrong, and I can afford it. But it feels more than a a little unfair to see my younger siblings and friends struggle to pay rent when he's got a whole apartment all for himself for no particular reason other than 'times changed'.

I could go on and involve my 'Boomer' grandparents who are throwing all their money at improving their home in bum-fuck nowhere that none of their offspring will ever care about, while they've got kids and grandkids who could really use a bit of money, but I'll leave it at this.

It reminds me of 'We Suck Young Blood' by Radiohead, and while I suppose that's what we get in a society that emphasizes the individual over the collective, it still sucks, and quite frankly I feel no remorse over never visiting my grandparents once they're in a home and waiting to die. Let them die alone and unsatisfied with their fancy house.

(okay, I'm exaggerating. I'll visit them and I do care for them. But man does this stuff bother me!)

It seems like that would be unsustainable since that would kill off construction of new housing. It would be more sustainable to do it only for the land, but not the buildings themselves.

It is simply not possible economically to support these type of benefits.

It is possible to support these types of benefits. It's just not possible to do it while also using the public workers' pension fund as a backup piggy bank when the rest of the government budget needs help.

When you dig into these types of stories you almost always find that millions or often billions of dollars have been raided out of the pension fund by the legislature or the executive in order to make their budget numbers look good. Same is true for other publicly-funded initiatives which are always touted as "too expensive" or chronically "underperforming".

Of course, the same is true in the private sector as well, it's just that there at least the leadership has to go through the formality of declaring a bankruptcy in order to raid the pensions and repurpose money to their own preferred projects.

Sometimes this does actually happen, "His predecessor, Gov. Pete Wilson, took $1.6 billion from CalPERS accounts in 1991 to help close a state budget gap." But the overall trend is exactly the opposite.

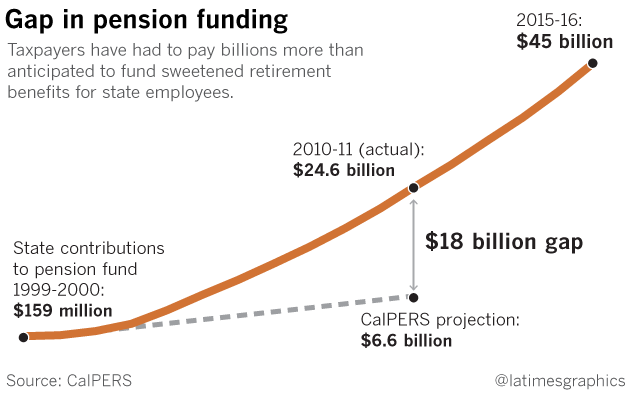

TFA is called 'The pension gap' for a reason. According to TFA, billions are flowing from general funds into the pension fund to cover the short-fall. $24.6 billion in the last decade, and another projected $20 billion in the decade to come. [1]

When the pension benefits amount to $2.6 million annuity at the day of retirement after 30 years on the job, yes, it is objectively too much of a benefit and unaffordable. If we were talking about an annuity worth just 5% of salary for each year worked, it would be a different story. But $2.6m divided by 30 is $86,666. That is just insane.

That depends on how much is paid in and if it's mismanaged.

It's also recommended to have your 401k set to pay your final monthly pay for your remaining months. We think that's sustainable, don't we?

The real problem in America is gross mismanagement of pension funds. It's going to get worse. I live in a county where it was suddenly discovered administrators had been lying both about funding the pension and it's performance for years and now employees are screwed.

As opposed to having state funded pensions which are invested in the market and when the global economy collapses everyone else who just lost their savings has to pay even more to the people on fixed income plans?

When the global economy tanks everyone is in for a hard time.

Well, part of that deal is delayed pay, because the public sector pays a great deal less. Without this, you're going to get menial and do-littles in public service. ... Which the more I think about it, perhaps is the reason why they want to, so the Republicans can look at their bad performance and cut funds further. (Don't get me wrong, Democrats seems to like throwing money down holes for populous programs, which have their own set of regressive issues. I'm much for UBI, and scientific testing of laws and programs to determine if the benefit is actually helping. If not, eliminate and move it to help more, better.)

If you cut funds by what you can, and then blame them for bad performance, you can "punish them" with less money, getting even worse. Wash, rinse, repeat, until that program is effectively dead. We're seeing it in the schools right now, with "No Child Left Behind" and the similar takes across the country with it. Inner city schools have bad performance, primarily because of bad home life, poverty, lack of food and resources... But because they do bad for tests, they get less funds.

I always think, what would our system look like if we adequately funded our programs? Would the BMV be such a cesspool? Not hardly. Would dealing with government office be peachy? Well, no. But they would have quick serving times and adequate material and time response in larger issues. Instead, what I hear is "They're bad, so lets cut funding." which exasperates the problem by now cutting personnel, time, and physical resources.

I am not sure public sector work pays less than equivalent private sector work on the whole.

I don't know for certain either way. My unsubstantiated belief was that it was higher and sometimes significantly so especially taking into account benefits, vacation time, and overtime policies.

Half of them said that "Private Makes More". The other half said "Public Makes More". The ones that said that Private makes more, usually added in commentary about Right-to-Work states, and discussed unions, whereas "Public Makes More" discussed the excesses and governmental waste, and evils of taxes. I'm sure you can see a trend of biases here. Attacking Private was Democrats and Left leaning orgs. Attacking Public was Republicans and Right leaning orgs.

The best, most impartial was from a reddit posting (https://www.reddit.com/r/engineering/comments/314v7b/does_pr... ) asking specifically about engineering pay between public and private. Of course, by the very definition they are anecdotal. But they seemed to try to answer "What is better monetarily and compensation-wise, rather than bringing in socio-politics in its stead.

The third possibility that is curiously rarely considered by so called 'market' advocates is that it might be a competitive market and both groups are offered more or less equally attractive compensation packages.

I would think a way to discern this, is that absolute cash in hand, private makes more. Public, if you add in the non-cash benefits, makes more. The argument however, of what I was making, is that if attrition destroys the understood contract of the non-cash benefits, Public would make significantly less and be less able to attract good talent. We are already seeing that with regards to K-12 teaching profession in many states.

I was asked to cite sources; kindly at that after respectful disagreement. After some searching, determined that answering that was going to be extremely partisan, and refused to answer the question at hand of "citation needed". And your suggested answer seems to be what the hordes on reddit kind of, not really, sort of agreed to.

In the end, even on reddit, it was back and forth 50% one way, and the other.

It should be expected (and the common wisdom) is that government jobs pay less than comparative work in the private sector, all else being equal.

That's because government jobs are protected by the constitution. Courts have said that government employees have a property interest in their employment such that the due process clauses of the 5th and 14th amendments attach. Firing and even laying people off is much more costly in the public sector because the government has to follow and document detailed procedures when firing or even reprimanding employees. The legal burden is on the government to show legality, whereas in at-will private sector employment the burden is on the employee to show illegality. It's a _huge_ difference.

Also, there tends to be much less funding and employment volatility in the public sector. The [theoretical] ability to increase taxes, and favored rates on municipal bonds, make it easier to cover short-term gaps in funding jobs.

Therefore, given the relative job security, we should expect public employees to make less than their private sector counterparts.

In practice, though, it's more difficult to assess. In almost all states large segments of public sector employment operate basically as a jobs program--for various disadvantaged groups (i.e. blue collar worker without a college degree, minorities, etc). And part of the reason is because similar blue collar jobs in the private sector have disappeared. That makes comparing income difficult.

At the other end of the scale, highly skilled people likely value job security much less. That means there's more pressure to increase salaries to attract those individuals.

EDIT (append):

Also, at the federal level there exists a relatively unknown non-partisan equilibrium / agreement in Congress that has capped the federal civil service. The number of federal civil service employees has remained virtually unchanged since the 1960s.[1] The huge growth in discretionary federal spending has been funneled into out-sourcing. Huge swaths of the "private" economy are basically federal jobs programs. Firing is much easier, but executives and shareholders get to skim cream from the top. The whole dynamic really confounds everything.

I've worked in the public sector. It often pays better with better working conditions and better benefits (even excluding the pension) than private sector jobs. It just doesn't compare well to Silicon Valley tech standards, which is an entirely unreasonable comparison to make.

I don't have an answer as to who pays more for equivalent work, but I don't think that is the only important question.

Suppose a bright young person has the skills to be a great elementary school teacher and to be a software engineer. If being a teacher is known to lead to a life of poverty, then few people who have options will choose teaching. If the only people who teach are those with no other options, then we have a problem.

If you need effective people to make your organization function, you have to compete for them, and not just within your industry.

You don't get share options for one and you haven to take pensions fund valuations with a very big pinch of salt as both sides have interests here.

As long as you have a steady state of members joining at the base DB schemes some of the more extreme cases are very unlikely and would require for example losing 100% of the deferred scheme members overnight.

> I always think, what would our system look like if we adequately funded our programs? Would the DMV be such a cesspool?

I suggest looking at the article's interactive graph. It tells me that

> DMV managers with at least 30 years' service earn an average yearly pension of $51,572. And they are eligible to retire at 55.

Now I don't vouch for the veracity of any of those numbers, but assuming they are somewhat accurate – $55,000/yr for life for 30 years of work (assuming you start at 25) sounds like pretty good funding to me.

> $55,000/yr for life for 30 years of work (assuming you start at 25) sounds like pretty good funding to me.

It would take about $2MM to earn that yearly in dividends from an S&P500 index fund, which is more than they would have earned in salary over that time.

Let that sink in for a second and you'll release how screwed up this system is. These people would need a 80-100% match to have an equivalently valued 401k after 30 years of service. No sane company would offer that.

CHP officers often make $100-200k per year. Their salaries are public record. There's a middle ground to be had between six-figure salaries for 30 years followed by a windfall valued at ~$5MM, and creating punitive incentives.

If they want to provide delayed incentives, then a generous 401k contribution with a very long vesting schedule will suffice. But current pension systems are completely broken. The pension system should only pay out a fraction of earnings and distribute that amount based on "shares" owned of the pension. Shares are earned by paying into the system.

401k's are a bad deal because employees are at the mercy of the stock market at the time of retirement. Pensions should be able to smooth out ups and downs of investments better than a private 401k.

Also, with 401ks, you can invest in anything from small cap / developing world stocks, s&p 500s, large cap dividends, private bonds, public bonds, and U.S. treasury bonds.

If you have a large group of people commencing to draw down your fund, your time horizon can be quite short. Similarly, if you have future workers not in the program, you can't "pyramid scheme" it.

20 years of investing are required for most classic pensions and the CHP example workers are likely to have as many or more years than that. An appropriate age based fund (which would admittedly, likely have huge fees) would reduce risk of the money you'd be drawing down on in the next 10 years.

There are problems in NY State and Illinois as well. Illinois has been in some sort of legislative standoff between the Republican Govenor who is trying to rein in pension costs and the Democratic legislature.

NY State if I recall, has some sort of constitutional amendment that creates huge pension liabilities for taxpayers.

These huge pension liabilities as well as increasing Medicaid costs means that students attending public universities in California, Illinois, and NY State have to pay higher and higher amounts of tuition, in effect subsidizing the pension funds and Medicaid.

It's happening everywhere, and not just at the state level. This is also occurring at the city level, see Dallas[1]. They didn't have enough money to pay out scared people that are all trying to withdraw now, though they have implemented stop gaps[2].

From [1]:

"This month, Moody’s reported that Dallas was struggling with more pension debt, relative to its resources, than any major American city except Chicago."

All pension funds are pyramid schemes. We need to move to fixed contribution plans for giving people money for retirement. The existing schemes can only be propped up by more taxes or by slashing benefits.

All pyramid schemes start out solvent. That's how they convince more people to join.

There is a simple test to see if any of these things are pyramid schemes. If no new money comes in and no new people participate, can all the payouts that have been promised be made? I think it is clear that pension plans don't pass this test.

Yes, a properly funded pension doesn't need new money to pay out existing benefits. The new money coming is a down payment for the people who will eventually retire, not to pay out benefits for those who have retired.

Also, Ponzi scheme is a closer match to what you are implying. Pyramid involves escalating returns based on recruiting new members "under you".

If each persons money was able fund their own retirement then fixed contribution plans can only be better as there is no longer any pension fund to pay for. Also, I am implying that most pension plans are ponzi schemes. They depend on future people to make up for the short falls. A properly funded one would basically be just a managed fixed contribution plan. I don't know of any that are like that. I'd be curious to read about any that are.

Illinois is the real time bomb. My prediction - California will eventually pair property tax hikes (from 1% to 2% on every property in the state; limit prop 13 basis to one property per person) with pension benefit cuts (10%; reduced COLA) to close the gap (after many articles like this one followed by much public wailing and gnashing of teeth). But once the political calculus is settled, at the end of the day, the money is there. California property taxes generate ~ $40 billion annually so you could double them and (factoring in a resultant decline in home prices and local economic activity) still pull out another $30 billion or so in annual revenue. But Illinois (Chicago) has much less ability to raise property taxes, which are already %-wise relatively higher on lower absolute property values, and the state's pension shortfall is significantly worse.

The author doesn't mention it in this article but California's other major problem is Medi-Cal. Free health care for everyone in California below the poverty line. The Feds pay 95% of the bill currently under the ACA medicaid expansion but if/when they start to pay less then California has tens of billions of dollars in new liabilities to contend with. Combine one/both of these problems with another market crash - which would mean lower pension returns, but also decimate California's capital gains dependent tax collections - and it starts to look like a fiscal 'perfect storm'. I give Gov. Brown a lot of credit for talking about the need to build up a rainy day fund but I fear it's far too little too late.

At the same time, many public California institutions are outsourcing their IT and other infrastructure costs while laying off workers because of budgetary pressure. Just another case of the baby boomers destroying future generations for their own personal gain. Pension funds are basically pyramid schemes and are economically doomed.

Ah, the rooster always comes home to roost. Well funded public sector unions and their pocket politicians robbed the state coffers blind. Will we see anyone hang to pay for this thievery? Not likely. I simply expect higher taxes in the future. This state will never learn until there's no more money left to take from its citizens.

Public union negotiations are always against the non-union taxpayers, which are not well represented since the politician "representative" is bought by the union. Public sector unions are the embodiment of moral hazard.

I don't understand why state/federal employees are allowed to unionize at all, let alone why they have such strong ones. Are government employees actually in danger of abuse or is it just because they can?

Because businesses go out of business when they can't meet their financial obligations. Or they declare bankruptcy and restructure the debt. In the meantime, their competitors pick up their slack in the various markets (labor, suppliers, sales).

The same mechanisms don't exist when it comes to governments, who, by definition, have certain kinds of non-negotiable monopoly and monopsony powers.

Of course they can. Every city, county, state, individual and corporate entity in the US can go bankrupt. The federal government can't, technically, but it can default,

States and the federal government cannot meaningfully go bankrupt. The problem is described in the article. While cities and counties can technically go bankrupt, they will externalize the costs and take on debt burdens at taxpayers' expense before they do so, to an extent that private companies are not allowed to. There have been just 9 city and county bankruptcies in the United States since 2008. Only 6 of them resulted in debt shedding, representing less than $30B in debt. That's 0.06 percent of total municipalities that could theoretically go bankrupt. In that time, tens of thousands of business entities and hundreds of publicly traded companies, representing trillions of USD of capitalization, have gone bankrupt. The overall ratio of public:private sector economy in the US is roughly 1:2.

There's an "in Capitalist America" joke in here somewhere, because you really don't have any effective right to union membership in the United States. Organizing any new union is a grinding struggle.

Public sector unions also become more powerful in concert with private sector unions and vice versa - strikes work much more effectively when they are synchronous.

Ah yes, theft by negotiation, why didn't those unions simply make a worse deal for their members, just like we would all expect our lawyer to do for instance if they thought it was better for society. The problem here is short sightedness and over optimism, blaming the unions is just buying into it more.

Well, part of the problem with our current society is that the social norm is to only look out for your own interest, and the public be damned.

This attitude is applicable to lawyers, who only represent their clients, to company executives, who only represent investors, to investors, who only care about their own returns, and to lobbyists, who only care about their lobby's interests.

This sort of system is fine when all parties to a dispute are equally organized and powerful, but it squeezes out the general public, who are not able to mobilize as effectively. It also forces people to focus on how to win, rather than how to cooperate more effectively for mutual benefit.

Unless we are willing to relax this attitude of 'only care about my own or my client's bottom line' at least a little bit, there is going to be little room for changes that are necessary to happen.

I can't see that going well if it's the government that appoints and pays for the public advocate.

And if the public advocate is an elected position, then we have the same problem as exists now -- unions are politically much more organized than the general public.

It's not "negotiation" when you bankrolled the other side into their position of power. The public sector unions in California have bought politicians through campaign donations (and most assuredly less scrupulous means such as bribery) for decades. The REAL problem here is the tax payers have no representation at the negotiation table because their politicians are crooked.

Surely it was someone's job to project these future costs when putting such promises into employment contracts. And I would also presume that these future cost calculations should result in some amount of planning to understand what the minimal amount of tax revenue or investment would have to be to support the future obligation.

However, even if that happens, how do employees prevent politicians from mucking about with those plans so that they can receive the retirement benefits that helped convince them to take jobs? These fears are why someone must have encouraged Congress to muck about in the USPS budgets wrt retirement accounts.

The only solution I see is mandating that (gov't) employers pay, during an employee's employment, into a retirement account such that politicians and bosses can't touch the money, and only the employee can do anything with it during retirement.

Your solution is precisely what is required of all private companies by federal law--all future pension obligations must be 100% funded at any point in time, and the funds are basically untouchable once deposited. Thus, the moment somebody retires, 100% of his expected payout until death is literally sitting in the account. Basically, after N years of employment into an expected M-year career, at the end of year N then N/M of the expected pension payout must be sitting in the account.

To account for unpredictable dips in market value while still following the law, in practice retirement funds tend to be overfunded. This is partly why private companies prefer 401(k)s--you don't need to overfund the accounts. (The other reason is that executives can be given disproportionately more benefits relative to regular workers under a defined-contribution plan (e.g. 401(k)) than a defined-benefits plan (e.g. pension).)

State governments are currently excluded from the federal funding requirements governing the private sector. The easy solution, politically, would be to amend federal law to make state employers subject to the same or similar rules required of private employers. There are some thorny constitutional issues, though, around the federal government placing mandates directly on state governments. So while being the easiest solution (because Congress is less beholden to state employee lobbying interests than local legislatures), it's still not an easy bill to pass.

That said, it's not fool-proof. A big reason for the merger frenzy during the 1990s and 2000s was that mergers provided opportunities for CFOs to extract money from pension funds. That is, mergers allowed them to fudge the numbers much more creatively. The increase in pension funds "bankrupting" companies is related to these shenanigans. The CFOs and other executives didn't care, though, because the shuffling of pension funds provided enough quarterly paper gains to trigger huge bonuses.

Your proposal is essentially what we have in Australia with superannuation. Employers pay a minimum of 9.5% of pre-tax salary into the retirement accounts, and then can't touch it.

>Asked to study differing scenarios for the financial markets, Seeling told the CalPERS board that if the pension fund’s investments grew at about half the projected rate of 8.25% per year on average, the consequences would be “fairly catastrophic.”

8.25% per year? No one averages 8% per year growth. That's not even an optimistic projection, just a stupid one.

Well pedantically that's not far from historical performance of equity markets if NOT adjusted for inflation, which these numbers wouldn't be. But he point stands that (1) pension funds won't be 100% equity, and (2) a pension fund should be assuming more conservative growth figures.

Many people believed the housing crash wouldn't happen, many people often believe incredibly naive things. This should not excuse them. There were people among them trying to be voices of reason, they ignored them -- as they always do.

It doesn't matter that it was a terrible idea. The people who voted in favor got the poll bump they wanted and everyone is gone by the time the bill comes due.

Burn this pattern into your brain, it has happened hundreds of times and will happen hundreds more. Every single time people will exclaim "We couldn't have known!" That is simply misdirection, they didn't even TRY to know.

Yes, there are many stupid but widely believed projections.

.com boom is not a regular boom. It will rise forever!

Housing prices will always rise!

Ad-tech will grow boundlessly!

In my opinion one of the greatest tragedies of these cycles is that many people desperately want to believe they hype about "This time it's different", and they can find plenty of "experts" to tell them what they want to hear. Regular people who could have had a solid place in the middle class are thrown into chaos because they lack financial savvy.

Is it stupid to expose yourself to a level of risk that can cause this? I think so. However, it seems like we provide more and more opportunities for unsavvy people to do severe and long-term damage to themselves and their families.

If you want to blame someone, blame the accountants. Pension funds' liabilities are long-term and inflation linked. If they had invested fully in inflation-indexed bonds (as the Bank of England pension scheme does), they would mostly be alright now. But pension fund accounting allowed them other options.

During the 1990s and 2000s, pension funds underfunded their liabilities, assuming they'd be able to make up the difference from gains in equities, property and other high-yielding assets. In the process they created quite a few hedge fund billionaires and funded the venture-capital tech boom. Many of those investments subsequently turned sour.

But their most significant error was to assume that bond yields would stay high. Today's low yields mean that they can't discount their future liabilities as heavily. The icing on the cake has been a moderate increase in longevity, which has been enough to tip the whole industry into crisis.

During the 1990s and 2000s, pension funds underfunded their liabilities, assuming they'd be able to make up the difference from gains in equities, property and other high-yielding asset

Not in the UK - if a company is deemed to be overpaying, according to the Revenue, they pay tax penalties. The Revenue don't care that the value of investments can go down as well as up, their pensions are paid from taxation...

If you've got a link explaining the tax rules I'd be interested to see it. Seems to me like companies should prudently fund their pension obligations before minimising their tax bill.

I'll just throw for the opposing side and point out that "Gov. Pete Wilson, took $1.6 billion from CalPERS accounts in 1991 to help close a state budget gap". A random internet calculator tells me that investing in the S&P 500 with reinvested dividents since July, 1991 has had a 844% return. I wonder impact $1.3 trillion would have on the CalPERS shortfall (edit: this would only be $13 billion).

In the private sector there's a balance: First, union and management are adversarial, since management's pay is often partly/wholly in stock/options or otherwise tied to the company's financial performance. Second, if the union pushes too far then the whole enterprise will sink.

But in the public sector, neither of these things are true. Unions and management can collude to fleece the taxpayers, since management's tenure is tied to votes, not financial performance. Additionally there'll be increased taxes, a federal bailout, or some other steps taken to allow the government of California to continue to operate no matter how much their pension obligations rise.

US government pension funds (state, city, etc.) are basically doomed universally.[0] Tax payers cannot stomach having to pay more for less services so that a small fraction of society can retire much earlier and with cushier benefits than the vast majority. As happened in Detroit, benefits will be cut in order to prevent catastrophe. It's both the morally right solution and realistically the only solution.

The alternative interpretation is that politicians and the people who elect them (meaning all of us) tend to be short sighted and underfund pensions for public workers. Many of those public workers are willing to work for less pay because of the pension, so in effect we are defrauding them. Detroit is an odd example to use as there we are dealing with a severe population crash, that's not the situation in California.

Public workers don't settle for less pay than private sector workers, that is an often repeated talking point that simply isn't true.[0] A garbage man, janitor, administrator, etc. working for the government isn't going to magically make more salary by quitting and going to the private sector. Top level employees can make more in the private sector, but the average worker cannot. Public employees make more money, are very difficult to fire, and have far more benefits than most workers.

"Other studies based on comparisons between similar federal and private workers find either no wage gap or a federal wage advantage. A 2012 Congressional Budget Office (CBO) study found that, for comparable workers, federal wages were similar to private wages overall, with just a small two percent advantage for federal workers"

Looking at that report it looks like from a bachelors on up public sector workers get less compensation then private.

They absolutely do settle for less. I moved from public sector to private sector and tripled my total compensation. I did go to a lot more meetings, though. :-)

At lower skill and compensation levels public sector jobs do have a pay advantage. At much past high school graduate levels of skill the advantage shifts to private pay, and that shift goes exponential for any skill that is in demand.

> Public workers don't settle for less pay than private sector workers

That's...Complicated. In unskilled labor and skilled trades positions, it's often the case that public salaries are competitive, or at least that total compensation (including benefits) is.

In most general analytical/management positions, it's not close, public employees get paid far less.

In IT and some other fields the gap is even greater.

Who promised anyone a job? How is it that someone interprets "you need a college education to get a good job" as some kind of guarantee?

On the other hand folks nearing retirement today had actual promises in hand, on paper, "work at this pay for this period and you will receive a deferred benefit of X". Much harder to make a case that anyone was bamboozling anyone in that transaction.

By the way, this generational warfare theme is extremely destructive and does its proponents no good. It doesn't help when proponents exhibit the kind of thinking that asserts someone was guaranteed a job.

Go to college and you'll be fine was the implicit contract made over and over to kids growing up. "Just go to college, it doesn't matter what you study." People my age were told this, over and over and over. Ad naseum. Of course, the people saying it probably believed it.

Now you're right that there was no paper on hand. There was no explicit written agreement between adults - just an implicit one between adults and children. When this agreement wasn't upheld because of the housing crises and a change in the economy, there was nobody to sue; no agreement to say "this was violated" other than the implicit social contract between the new adults and those who raised and guided then through an often inane, ridiculous system.

I know people paying over a thousand bucks a month in student loans, and they aren't making much money because they studied digital/graphic design instead of computer programming. This guy would love to start a company, but a 1k/month loan payment puts a bit of a dent in his budget.

I didn't have that problem. I studied computer science and physics and never had an issue. The people i've seen struggle with this were people who were a) good and b) wanted to do something good for the word. People who haven't struggled were those who just wanted to get money and didn't really care a bout their impact on the world, and then those who went into certain classes of sciences - i.e. not biology.

I agree that the generational warfare is destructive. I've seen so much shade thrown at millennials by the people who raised them, but you're right that it does no good to play that same game.

I think you're right if you say that college students should be self-aware enough to know that studying a major not tied to a career will make it harder to earn a good living. By the same token, I think it's also accurate to say "if you wanted your pension paid, you should have ensured that the government would remain solvent."

Public and private pensions are going away, most are underfunded, 401ks are dramatically underfunded, and there are constant calls to cut social security to save it.

Instead of making private retirement benefits competitive we're looking at cutting everyone back.

I don't know where we're going but it doesn't look good.

I'm not sure how you can portray taking away pensions as "the morally right solution". It's at best a moral grey area.

These folks took jobs with pensions as one of the understood, agreed-upon benefits, and likely made their retirement and investment decisions accordingly.

If the answer is to bankrupt the state and make millions suffer so thousands live in early retirement luxury, the morally right solution is to bring benefits back to reality. Down vote me all you want, when push comes to shove over the coming years, it won't be everyone bending over backwards to pay someone 90% of their highest income when they retired at 50. It didn't happen in Detroit and it won't happen anywhere.

401k accounts are defined contribution. A public pension is underfunded by the recipient and are guaranteed for life with no cap on receiving. This is a model that leads to bankruptcy, they are unaffordable.

Traditional media outlets are desperate to save themselves but instead of trying to serve customers what they want they are indulging in tech dodads and hypermedia push assaults. LA Times won't be around much longer by their own projections. Attempting to force feed people content they don't want might be a factor in that.

Anyway, just goes to show that its not just big corporations that are greedy.

Any reform will be difficult without adjustments to the promised pensions. With an economic slow down coming in 2017-2018, the gap isn't going to get smaller.

"One of the few voices of restraint back in 1999 belonged to Ronald Seeling, then CalPERS’ chief actuary. Asked to study differing scenarios for the financial markets, Seeling told the CalPERS board that if the pension fund’s investments grew at about half the projected rate of 8.25% per year on average, the consequences would be “fairly catastrophic."

Who decided on the projected rate of 8.25%, in the first place? Wouldn't that have been the work of the CalPERS’ chief actuary, Ronald Seeling?

The root cause of the problem was the actuarial assumption of an 8.25% rate of return. This is what allowed the new Defined Benefits to appear to be "free," and that is what enabled the board and politicians to ram this through.

Assuming an "average case scenario" of consistent 8.25% annual return on a pension investment portfolio is subjectively irresponsible, even in 1999. But more egregious is the fact that the actuarial profession failed miserably to recognise that the Defined Benefit was a financial guarantee similar to a put option, which means that the value of the put option should have been explicitly calculated - which would have been done by projecting scenarios using the "risk-neutral" rate of return (i.e. the yield on US government bonds) instead of the "real-world" rate (i.e. the super-optimistic assumption of 8.25% annual returns).

The article goes on to explain that the Chief Actuary ran 3 different scenarios: a "pessimistic" scenario of 4.4% returns, "average" scenario of 8.25% and "optimistic scenario" of 12.1%. This is the crux of the problem, and it is not the first time that such actuarial calculations have blown up a pension plan like this. The right thing to do would be to calculate a single "scenario" using the risk-neutral rate, which would have been lower than 4.4% in 1999 and today it would be closer to 0% ... That would have correctly valued the economic cost of pension benefit as a multi-billion dollar expense that no politician would be able to so easily ram through the legislative process.

"Lou Correa, then a freshman Democrat who carried the bill in the Assembly, said he fell victim to inexperience. He remembers seeing actuarial reports and assuming he’d “kicked the tires” and asked the right questions. Correa, now running for Congress in Orange County’s 46th district, said he should have sought independent financial advice."

I think Correa was reasonable in assuming that actuarial reports, signed by the Chief Actuary of CalPERS, would have properly "kicked the tires." That is what the actuarial profession is supposed to do. Just like if an engineer signs off on the construction of major transportation bridge, we can reasonably expect that that the bridge won't be be designed with fundamentally incorrect physics calculations.

Agreed. If I knew someone who was investing for retirement on the assumption of an 8.25% growth I'd be worried about them. The fact that a government agency did it is scary.

This is a routine practice for actuaries. Here's an actuary from 2008 in New York's pension system calling his calculations "voodoo:"

"In an interview on Thursday, Jonathan Schwartz, an actuary, called his job “a step above voodoo” and conceded he skewed his work to favor unions. He also admitted to erroneously claiming that a controversial early retirement bill, backed by District Council 37, would have no cost, explaining, “I got a little bit carried away in my formulation.” [1]

Again, my point is not just that 8.25% growth is a very optimistic assumption. My point is that we you guarantee a rate of return on investment, then you need to calculate the value of the guarantee explicitly, and the established formulas [2] for calculating the value of such guarantees do not require any assumptions about future growth rates - you are supposed to just use the "risk-neutral rate" rate, which is like the yield on US government bond.

An example of the guarantee that I'm talking is this (from the article): "Highway Patrol officers could retire at 50 and receive as much as 90% of their peak pay for as long as they lived" ... So the pensioners are guaranteed to receive X% of their peak pay, regardless of what the actual rate of return turns out to be on the pension investments. This is equivalent to a put option, and the valuation methodology that the Chief Actuary used for this (according the article) is inexcusable - but not surprising.

See above, the problem does not lie in the subjective question of whether or not 8% return is a reasonable assumption for an investor. The problem lies in how the actuarial liability was (mis)accounted for - specifically, the value of the guarantee was accounted by assigning it zero cost - which is completely incorrect.

It is as if an incompetent real estate appraiser were to assign zero value the Golden Gate Bridge, and then your local politician legally transferred ownership of the bridge to some friends for free because the appraisal assigned zero value to the bridge. And then those friends started charging tolls on the bridge, and pocketing the money for themselves. That would normally be considered fraud or embezzlement.

The worst part is not even the 8% (which is bad enough). These pension (pyramid schemes) plans also generally are modeled on healthcare tracking (generally) with inflation and that salaries also track upward with inflation. The salaries go up so the contribution is greater that the same percentage 10 years ago. But then healthcare costs start growing 50% year over year and salaries get frozen for budget cuts and all three corners of the pyramid fall down.

{kind=link}

It is simply not possible economically to support these type of benefits. Look no further than the Greece or Italian austerity crisis to see how these type of government payments will play out.