If you were hoping this was a sign of the real estate market falling and perhaps its your chance to get a bargain, think again.

> The company is seeking roughly $2.8 billion for the houses, which are being pitched to institutional investors, according to people familiar with the matter.

Institutional investors (Blackstone, Blackrock, Colony, et al) will be being in bulk, in cash, and at a steep discount before they even hit the market. Zillow's loss will be the institutional investor's gain. Of course, they will happily rent to you since that is the the plan all along - own all the assets, and every generation after X gets to rent [1].

I wish this would anger people more, but enough home owners will benefit from this dynamic - it will likely keep home prices elevated for longer, and set up an ugly conflict between those who do not have (and aspire to have) homes and those who currently own homes.

I agree. I wish people understood more of what these "institutional investors" are doing. The Fed has essentially trapped us in a system where the likes of blackrock get access to essentially free Fed printing press money right of the rollers that they then use to buy up real assets at inflated prices, which only drives up the inflation that thereby also drives up the value of previous purchases at near zero rate interest.

If you follow that logic to the final conclusion, you will find that these "institutional investors" only have incentive to not only buy up all the assets they can at near zero interest, but that doing so is a kind of self-perpetuating profit machine as inflation creates profits for them.

Yes, this is IMMENSELY dangerous.

Oh, and I did not mention that if it's not in collusion, the Fed has the tiger by the tail and is paralyzed with fear to such a degree that it simply cannot let go so as to at least have a chance of getting away in time, rather than the guaranteed demise of holding on to the tail and then eventually only getting ever more tired and the chance of survival crashing exponentially.

> The Fed has essentially trapped us in a system where the likes of blackrock get access to essentially free Fed printing press money right of the rollers that they then use to buy up real assets at inflated prices, which only drives up the inflation that thereby also drives up the value of previous purchases at near zero rate interest.

It's a trendy thing to say, especially in certain political circles, but could you substantiate it with something from a serious, non-partisan economist? AFAIK, for example, inflation isn't much related to it - rates have been very low for a long time, sans inflation.

> the Fed has the tiger by the tail and is paralyzed with fear

Again, anything substantive to support this? They are 'paralyzed with fear'?

> could you substantiate it with something from a serious, non-partisan economist?

The fact that printed money is fueling the housing market does not require an economist to see; it is obvious from comparing two simple observations:

(1) Americans expect to be able to get 30 year mortgages at rates around 3%.

(2) Americans expect to be able to invest their retirement savings in stocks and bonds with a long term rate of return of 8% or more.

This state of affairs would be impossible in a free market with a money supply that was not being manipulated; in a free market, nobody would be crazy enough to lend money for mortgages at 3% when they could invest the same money in stocks and bonds and make an 8% return over the same time horizon. The only reason #1 above exists at all is that mortgages are made with printed money from the Fed.

> rates have been very low for a long time

That's because interest rates are not determined by a free market; the Fed has its thumb on the scales (see above), and has for decades.

IME, people have lots of theories that look good to amateurs. Look at physics, as a striking example of how wrong amateurs can be for thousands of years.

Anyway, you aren't required to do research for me, but some person on the Internet writing economic theory is not persuasive to me. Oh well.

Yes I agree with this. In fact, having already done this math myself I am basically maxed out in house loans, i even took a cash out loan on my rental and dumped it into the stock market… I have already made an absolute killing doing this. Unfortunately I am not that smart and like you say, everybody else can come to this same conclusion. It will not end well.

> #1 is less risky, since mortgages have to be collateralized.

Less risky, yes. Less risky to the tune of 5 or more percentage points? Not so sure.

> #1 is also less volatile

That depends on the housing market, which can be subject to large fluctuations that have nothing to do with the underlying value of the assets and everything to do with the availability of newly printed money for mortgage loans. The years leading up to and including the 2008 crash showed how volatile a manipulated housing market can be.

Yep. Fannie and Freddie are buying nearly all of the mortgages in the US right now, so the only people lending money at 3% (or less) is the US government.

No, because the bank can borrow the reserve from another bank. That's the whole point of the overnight market.

But what if no other bank has any reserve to lend? Why then you have a banking crisis as collectively the banking system is short of reserves, at which point the Fed steps in and injects whatever quantity of reserves are necessary to make up the shortfall. So the idea that the Fed would allow a banking crisis in order to limit reserves to some arbitrary quantity is ludicrous. The Fed was created to make sure banks always had enough reserves. That's why we have a Federal Reserve system in the first place.

And in fact there are guarantees -- the bank can take a government bond and automatically borrow reserves with the bond as collateral, directly from the Fed, so the Fed stands ready to convert any bond given by the banks into reserves whenever the banks want. This is the repo market, so you don't need to borrow overnight from another bank if you have a treasury bill or bond, you can borrow your reserve directly from the Fed itself.

In short, the Fed controls the price of reserves -- the interest rate paid when borrowing reserves -- and it stands ready to provide banks with whatever reserves they need at the policy rate. Thus the Fed sets the price, and lets the quantity float.

You may also be interested in other nations such as Canada that have eliminated reserves and switched to a corridor system.

That the Fed doesn't care about monetary aggregates is aptly described in this FRBNY note:

More modern theories that strongly dispute that assertion. And certainly the money needed to pay compound interest on the loan has not been created. (Apparently it's expected that borrowers will materialize it.)

"Banks first lend and then cover their reserve ratios: The decision whether or not to lend is generally independent of their reserves with the central bank or their deposits from customers."

"Inflation" isn't the right technical term, and I'm skeptical of the more conspiratorial implications, but the Federal Reserve is pretty open about the fact that it buys a lot of mortgage debt and mortgage rates are low because of it. See for example https://www.dallasfed.org/research/economics/2021/0826.

I don't think institutionally-owned SFH rentals are viable in the long term.

Apartment complexes make sense as rentals because there's a great deal of efficiencies vis-a-vis property maintenance & management. Plus the added benefit of greatly reduced property taxes per unit. The downside is that they don't appreciate as quickly as other real estate can.

SFHs make a lot of sense for small-time landlords because they can be bought up in increments. But even small-time landlords pretty quickly realize the value in multi-tenant rentals and move to acquire more of them.

Blackrock, et al, will hold onto these so long as they continue to appreciate at double-digit rates. But after a few years of inflation-level appreciation, they will begin to dump these as their profits tumble due to the inherent inefficiencies of SFHs.

Places like Invitation Homes do everything as cheap as possible.

Cheap as possible paint minimal repairs no inspections. Shady things like intentionally covering up gas leaks.

Source: Family nearly died in multiple different ways.

Had an HVAC fall on kids bed In the night, just missed. Massive gas leak they lied about. Walls that were so hot they burned the skin.

Many things a home inspection would have uncovered.

This is the end game of the baby boomers and economy really. Collectively everyone is hoarding onto property for their nest egg, investment funds get piles of their money from 401ks and pensions as well to invest into areas like real estate. A large chunk of retirement is now predicated on maintaining or increasing property values.

The fed is now so fucked it can't even raise rates without immediately causing property value declines as mortgages decrease. There really is no solution and we are in for horrific pain eventually. It's simply a question of how long they can stall it.

The solution is simple. Raise rates and let asset prices normalize, regardless of the consequences.

There will be pain in the short term, but you're creating opportunity for future generations.

Policy right now is all about pulling prosperity from the future into the present. IE higher valuation multiples today enrich current asset holders, but leave little growth for future asset holders

It used to be that the Fed was not too focused on asset valuations, and actually drove policy on the basis of their mandates. Unfortunately they're too cowardly to do that anymore.

It may be partly due to the short term focused political system in the US. China actually is explicitly acting to reduce property values to make homes more affordable for its people. Of course this triggered all sorts of second order effects like the evergrande situation. We will see if they follow through all the way, but so far they aren't backing down, despite what looks like an imminent systemic implosion of the property sector.

Sometimes people lose when they invest. That's how it's supposed to work. Removing that element creates mass amounts of moral hazard, which will end badly on its own at some point.

> It used to be that the Fed was not too focused on asset valuations, and actually drove policy on the basis of their mandates. Unfortunately they're too cowardly to do that anymore.

Could it be that they're essentially captured by the likes of Blackrock, etc. I mean, it's been this way for a while, but it's getting to where government is openly a tool for the corporations without voter involvement.

Well, BlackRock actually manages their bond buying program, believe it or not. So BlackRock is the one executing the Feds QE purchases.

But I think it has more to do with the Fed trying to appease both the political party in power (as they control their renomination) and just people generally.

With all the social media etc nowadays, they have more scrutiny over their actions, and are afraid of making tough decisions. E.g. optimizing for the short run to the expense of the longer run.

But to your point, Powell in particular is much more focused on the stock market and how wealthier Americans (stockholders, homeowners etc) are doing. Past fed chairmen, like Yellen and Bernanke didn't seem to care nearly as much about market movements, and focused more on the economy itself, and their mandate.

> It used to be that the Fed was not too focused on asset valuations, and actually drove policy on the basis of their mandates. Unfortunately they're too cowardly to do that anymore.

From the financial crisis to COVID low interest rates (and inflating asset prices) seemed almost a consequence of their inflation+unemployment mandate: even with the interest rate around zero unemployment was slow to come down and inflation was mostly in financial assets and not the consumer price level.

Post-COVID seems to be a different story though. I guess we'll see in the next year or so how they react if the inflation pressure turns out to be persistent - personally I wouldn't be surprised if they do raise rates, even though that would obviously lower most asset prices.

Well, it's true that inflation was largely in check over the past decade.

But keep in mind that in the 1970's, home prices were actually included in the CPI. If this were still the case today, we would actually see inflation levels similar to what we saw in the 70s.

The CPI formula has been changed many times over the years, to suppress inflation numbers. There are strong incentives to do this, as Social Security and many other things are tied to the CPI.

There are logical arguments for these changes though. Homes are financed goods, and consumption can be considered the monthly carrying cost and not the value of the asset. However, ignoring "asset inflation" has led to much worse wealth inequality IMO. It would be better to continue to include national average home prices. Nowadays, there's a measure called Owners Equivalent Rents that partially gauge this. But there are tons of methodological flaws in how rent equivalent data is collected for CPI that lead to both underreporting, and a lag of ~12 months. e.g. Rents are up about 20% nationally since the pandemic started, but CPI has shown roughly 3.5% so far. The next few months should start to show the full extent of rental increases.

Now that car prices are causing a large increase in CPI, don't be surprised when they alter the measurement of these factors next year. They'll use some measure like average monthly car payment.

Also keep in mind that unemployment was around 10% post GFC, and took about 10 years to get close to full employment. That was quite a large shock that took a long while to recover from.

The market did fall something like 20% in 2018 as the Fed raised rates to preempt inflation, but they chickened out and reversed course and market immediately rallied back all gains.

And as you said, it's pretty clear right now they are dragging their feet on doing anything post COVID. I'm pretty sure Powell is really optimizing for retaining his job, since his term ends very soon... otherwise they really shouldn't care about market movements to such an extent.

They will almost certainly announce the taper tomorrow, but expect it to be wrapped in all kinds of dovish language to juice assets/speculation further.

Regardless of short term interest rate peg, they should absolutely not be buying bonds to suppress long term rates. They have been continuing an "emergency" bond buying program for a full year beyond what was reasonable to most people. I mean, why are they buying 120B worth of bonds every month, as housing prices have gone up something like 30% nationally? They are terminally afraid that if they can't manipulate long term rates lower through QE, that rates will rise and market or housing will tank. Well, we'll find out soon enough

> The solution is simple. Raise rates and let asset prices normalize, regardless of the consequences.

This is the exact policy adopted by the Fed in 1929: purge the bad out of the system. Let the failing banks go bankrupt. That turned what was a recession into a full-blown deflationary credit crunch.

All the high-and-mighty theory and bloviating may not mean much in the face of 25% unemployment, wages falling 50%, and 15%+ contraction of global GDP.

I agree there needs to be moral hazard to investing and interest rates are to low... but be careful what you wish for.

Yeah, but the point of the fed is to smooth the peaks and troughs.

Stimulus in recessionary periods is smart, and prevents prolonged recessions like was seen in the great depression, and somewhat during the GFC.

But the stimulus has already been done at this point. The crisis is over.

The situation we're in now is corporate earnings at all time highs, the gap between open jobs and job seekers at all time high, consumers with spending power at all time high, home prices accelerating at all time highs, inflation running very hot.

So this is the exact time that the Fed should be smoothing the peak, to avoid a full on bubble type of scenario. By not acting, they setup the risk factors for another 1929 or 2008. E.g. encouraging mass speculation, high levels of debt and so on.

So I agree with you. But the goal should be to avoid creating the conditions for systemic failures by letting bubbles get out of hand. China in particular let their real estate bubble get far out of hand, to the point that it's not really possible to resolve without creating a systemic issue.

You fundamentally just have to accept some down periods and small hits to avoid the massive failures that come along with facilitating much larger bubbles/structural risks.

I agree institutional investment into homes is a big issue, and based on our current laws it will drive a lot of people into rental agreements that are unlivable and for the few it'll make mortgages obscenely expensive.

> This is the end game

I disagree with this statement. Firstly, we will likely fix it sooner rather than later. Secondly, if it truly gets horrible, we still have one person one vote. Its not the property owner that gets the vote, its the renter that gets the vote. If you end up in a locality with 100% rentership, they will vote for rental caps, they will increase their living quality through building codes/regulation, and they will vote to remove zoning and the local politicians will follow through because there is no downside to the people in their constituency.

There will still be corruption in the form of state level or federal laws to reduce local autonomy (e.g. with municipal broadband), but thats a problem we already have, and people need to learn to vote for their best long-term benefit rather than ideologically and/or their short term benefit.

Even today, if you want to stop Big Real-Estate from making rentership horrible and keep making housing prices obscene, vote to remove zoning or at the least, vote for zoning that would let the market increase housing 100x. We are all kinda NIMBY regarding the short term, but need to find a way to vote against our short term best interest for the sake of our long term best interests.

They are generally called non-primary residency taxes, and they're definitely a thing, and definitely getting more publicity, and most definitely need to become much stronger and more widespread.

We have these in BC - they were adopted in response to overseas real estate investment (and other factors) driving the Vancouver housing market insane. Canada also has a number of programs that make property purchase for new homeowners more affordable by waving some taxes and allowing interest free borrowing from your retirement fund. So the fight to keep housing affordable for everyone is a difficult one.

One of the issues is that when these sorts of policies initially roll out you tend to see a contradictory effect of sudden spiking in prices as a lot of people who were on the fence suddenly decide to add to the housing market demand - but over time these policies tend to settle in a place where thing are more affordable.

The other issue is that the renewal period for first time home owner benefits is quite long, so if you are exiting a long term relationship or trying to pick yourself up after bankruptcy you can be forced to enter the market as if you were a well established asset holder.

"but over time these policies tend to settle in a place where thing are more affordable."

I seriously doubt that to be true in a low supply situation. In the Netherlands, the government reduced real estate transfer tax from 8% to 2%, and sometimes even 0%. This should make houses more affordable to newcomers.

Another well intended measure was for older people to share their wealth to their children via early inheritance, tax free.

The market simply adds this discount and extra start capital to the price "room". In a situation of perpetual scarcity, the price will rise to the maximum people can afford/borrow.

And with "people", I mean only the buyers. It doesn't matter if 90% of the population is priced out of the market if the richest 10% is still enough people to buy up all supply.

This last bit is most worrisome, because it means that even the nuclear instrument of increasing interest rates is unlikely to resolve the issue. The interest cannot be jacked up much because that would bankrupt the middle class. A minor tweak will be no issue at all for the richest 10%, so the price will not come down.

Increasing supply in a dense and popular area isn't a structural solution. Not only does it meet a lot of resistance, new demand will forever continue to outpace the constraint of delivering new supply.

Which is why I believe in reorganizing demand. These dense areas are dense because it gives people access to jobs and education. If we reorganize that into a more sane distributed way, we truly address the problem.

> Canada also has a number of programs that make property purchase for new homeowners more affordable by waving some taxes and allowing interest free borrowing from your retirement fund

Some further flaws in the system: I was shocked to find out that the new home buyers tax credit only applies to homes under $500k - which in vancouver means it only applies to a handful of small condos. It's also not poolable, so two first-time buyers going in on a $501k condo are disqualified.

I thought Cambridge, MA has a great system — the first $250k of any property value is tax free (or at least it was 10 years ago), and property taxes then only go above that. It had the effect of making property taxes cheap for small home, allowing lower income people to have more affordable housing over the long term.

Homestead exemptions like that are common in most states.[0]

Cambridge does have a lower than average residential property tax rate, mostly due to how much commercial development they have. I still wouldn't point to Cambridge as a particular success in terms of affordable housing though.

> but over time these policies tend to settle in a place where thing are more affordable.

Could you point me at some more reading that talks about this? The increase in prices makes perfect sense to me, but I don't really have a good handle on why things would come back down.

Non primary is one thing - but perhaps the thing that needs to be gone after is commercial residential (as in, if you have more than x properties). Or commercial ownership of single family homes. There is a difference between owning a 10 unit apartment and owning 10 single family homes.

Many places have a (small) rebate for owner-occupied real estate. Cambridge, MA is one; I get a break for living in my house as a primary residence.

Edit to add: I looked up the exemption calculation. It excludes up to $432,666 from the assessed value. Multiply that exclusion by the rate of 0.00585 ($5.85 per $1K per year) and the exclusion reduces a homeowner's taxes by $2,531.10/yr.

We have that in Michigan. Non-homestead property taxes. All it does is make apartments more expensive for renters. The cost is just passed on to the renter.

This, this will be actual result. "Just add more taxes" === the renters pay that delta.

Scale it per property === take the average of taxes / homes, pass it along to the renter.

About the only way I can the cost not getting passed to the renter is for a "the government" to set the rental prices as if the home was under a rolling 30-year mortgage, taking into account PITI. Adding a property tax on top of that ONLY to the property owner, maybe exponentially per property owned, could curb companies like Blackrock.

That being said, I have very faith that a "the government" could do this efficiently/correctly/at all. Trying to trace down umbrella corps and whatnot would be cat and mouse. The US government can't even figure out who is cheating on their taxes as it stands.

Raising property taxes on SFH rentals, but not apartments will make apartments more attractive. Sure, renting a house has advantages, but those advantages have a price, and how many renters are going to be willing to pay 40% more per square foot for a SFH over an apartment.

At some point, even an expensive mortgage is a better deal.

Apartments are great, we should incentivize apartments. They are high density and can be built in a variety of sizes.

Apartments are great, unless you want a yard, a large family, to let your parents[-in-law] move in so you can take care of them, a large dog, more than two cats, more pets than the property owner has arbitrarily decided to allow, equity, a barbecue, frequent parties, or the ability to not have to pay rent or a mortgage someday. Buying apartments is not the norm, nor are ones large enough for a family with more than 1 or 2 kids.

> I don't think I've ever heard of a politician even talking about that though

You have to consider that legislative members tend to own property and tend to be baby boomers. They are far removed form the experiences that younger generations have to deal with - from their perspective, their home value can go up 20% in 2 years and that will be rationalized as a normal market. They are not talking about it because they are benefiting financially, and talking about may make them hurt financially. This will change, baby boomers cannot live forever even though they behave as though no future generations exist.

It won't change. After the boomers come the millennials, and I believe there's still a generation in between (generation Y?).

Many of them may have been just in time to snatch a house from the market, and they see their home value go up. None of them are going to advocate for super high taxes on their "unjust" gains nor will they give a discount to future buyers. They will maximize the return just like everybody else would.

It's not boomer behavior, it's human behavior. Boomers were just lucky to get in earlier. The only annoying thing about some boomers is that they don't acknowledge their luck, and insist it was all due to their hard work or brilliance.

The school going generation always wants a revolution, a redesign of society. To fix its flaws, to make it more fair. It's easy to want to change everything if you have no responsibility or anything to lose. But then they grow up and have skin in the game, and they'll be just like everybody else, protecting whatever wealth they have.

Consider that many boomers were hippies when they were young, rejecting even the notion of personal property. Now they own almost all property. The 21st century version of hippies are even better at managing progressive optics whilst taking in top 1% salaries.

Most baby boomers (the ones getting all the blame) usually own one house, that they live in... even if the value goes up, they need a place to live in, and the high prices are pretty much everywhere, people actually want to live. The only ones profiting from baby boomers are their kids when they inherit the houses.

Politicians are probably getting paid of by companies investing in housing and buying up hundreds or thousands of houses, because the price increases make it more profitable than many other investments, and (unless there's some legislative action) makes the investment safer than most other high-profit ones (eg. cryptocurrencies).

> even if the value goes up, they need a place to live in, and the high prices are pretty much everywhere, people actually want to live. The only ones profiting from baby boomers are their kids when they inherit the houses.

This leaves out one major factor: they need somewhere to live but that doesn't mean it needs to be the same real-estate market or size. Someone who sells a house large enough to have a family in a major market and retires to a cheaper market can see a very comfortable return. Probably nowhere near enough to make up for the other impacts of the policies people voted for to drive up their home value but it's harder to get people to give equal weight to different factors when one of them will show up directly in their personal bank account.

This would be true, if someone old sold a house in san francisco and bought a house in bumfuck alabama...

But considering that people tend to move to a few urban locations, the house prices in eg. florida got very expensive too... yes, they earn a bit more, but I don't believe that single house owners, moving from SF to FL (or wherever) are causing the housing crisis.

It's also true if you sell a house in San Francisco and move to South Florida, or North Carolina, or all of the other places millions of people do exactly what I described. Retirees don't need massive houses, to minimize commutes to downtown, or being in the best school district, which opens up many options which other people might pass up. If your goal is “on the beach in South Beach”, yes, it'll cost a fortune but if your goal is “near the beach, any beach” you have plenty of options for well under $100k.

I don't disagree that this isn't driving the housing crisis — my point was simply that it's not like many older people aren't strongly in favor of the housing market staying high until they can cash out, because for many people their home equity is the largest component of their retirement plan and they aren't interested in continuing to need to deal with the maintenance required by a single-family house.

Whenever people say anything complex can be fixed easily with legislation, I'm pretty sure they don't have a clue.

These types of issues are never easy to fix, because they're cause by many factors that have taken years to form. There are no easy legislative fixes in practice. They only exist in theory.

another thing you can do is raise the interest rate on the mortgage for investment properties. This is already done somewhat but they could increase it quite a bit. Can't really pass the cost onto the renter either because the market supply/demand dynamics sets the rental rates, not the owner.

I mentioned the idea in another thread... but yeah... 0% property tax on your first property and primary residence, 1% on the second, 2% on the third...

Still makes it possible to own several houses/apartments (eg. summer home), but makes it impossible to do at a scale that those companies do.

Own a bunch of shell companies that own a single property each.

Real estate ownership is a mess. It can be nearly impossible for people to figure out who actually owns property if the entity buying wishes to remain secret.

Maybe, but a lot of people have legitimate reasons for holding their home in a trust.

If the savings are great enough, it would make sense to pay someone to "own" the house, with a contract saying that they must act at your direction. This isn't some crazy idea either, that's basically the approach that's already taken by these same people that hide their identities through shell companies. The "owner" of the shell company is some random B'zean who is paid to be a rubber stamp.

Then renters can afford the larger rents, and after the dust settles all you've done is take money from one of the state's pockets and put it in another, no?

The problem is the financialization of housing in the first place. You have to figure out a way to reverse that. Making speculation illegal probably isn't feasible, but could you require that renters earn equity offsetting some portion of rental profits?

100% agree. Institutional investors are setting themselves up to be landed barons that will seek perpetual rent from working people who can no longer afford housing as the supply has shrunk and housing prices skyrocket. Oh and if these institutions fail they get bailed out by govt(they are too big to fail!). Imagine if these 7000 houses were offered to buyers, this would allow so many families opportunities to homeownership, this whole scenario makes me mad as hell and I hope this practice will be banned in the future.

No. Landlords do not "produce" rooms by taking raw materials and transforming them into goods. In the current market, the rent is determined by how much the marginal renter is able to pay. Increasing the cost to the landlord doesn't magically increase the renter's ability to pay

Since institutional owners like this make up a tiny percentage of ownership, your solution would have a huge impact on small landlords, which would be passed along to the tenants.

Basically you're asking renters to pay for this behavior...

"A" government[1] could telegraph that major (as major as is necessary) policy changes are coming that will affect SFH investors in a detrimental way, and that it would be in their best interests to prepare accordingly.

If this does not happen, I suspect Mother Nature will eventually intervene, and that usually doesn't go well for anyone.

[1] I do not presume that any arbitrary Western government is actually capable of this in the real world as it relies on many prerequisites, some of them policy, some of them psychological/ethical.

I don't get this thinking. What is the difference between one landlord with 2 properties or 2 landlords each with one property? Why is the latter better than the former?

Does it matter? If you want to achieve maximum dwellings for renting, changing the distribution of units / owners doesn't seem like a practical way to go about it.

You would want to make more units, as many as possible.

Every person or corporation that owns more than one residential dwelling should pay increased property taxes based on the number of residential dwellings they own.

This is an easy problem to legislate away, our politicians are just too cowardly to decommodify housing.

There are probably easy loopholes to get around your suggestion. Just form another LLC and purchase the property under that LLC instead of you as an individual, then each entity owns only one property, so they get the standard tax rate instead of what you are proposing.

Of course this would be a giant pain of a workaround to scale, but for the non-mega corporations it'd probably work. I'm sure that the huge corporations owning large swaths of residential properties would figure out scaleable loopholes.

Just tie the "first home" tax exemption back to a person by making business entities a pass-through to the registered agent (or some other single officer). i.e., an LLC can't claim the exemption, but the agent can pass their exemption through the LLC to a property.

They could also add in a carrot, to reduce capital gains on sale of non-primary residences.

There are too many incentives currently to hoard properties like the damn monopoly man, so you need to start clawing away at them. Taxing the eventual sale just encourages people to not ever sell, so tax them for hoarding directly.

This is an interesting idea! Some graduated tax rate for the number of dwellings + properties that way a second home or small time landlord can own say a dozen properties before the marginal taxes take too much of the marginal profits. What efficiencies are we giving up in this model?

This has a dependency on the government actually enforcing the law though, in Canada when it comes to real estate, it has been well demonstrated that they will not. Hopefully for the US it is different.

Make it 5 houses per person (10 for married couples), then.

Plenty of families out there own rental houses as an investment, which I think is a good thing. It allows people an alternative to investments like the stock market if they aren't into that, and it gives a path to turn labor into wealth through DIY maintenance, repairs, and improvements.

Plus it allows individuals to better manage situations like parents dying and leaving them a house that they may not want to sell immediately.

Won't that just mean less investment in new housing, so over time less housing stock, resulting in (delayed) price rises and more people excluded from the housing market.

I mean in general the only possible solution is more housing ... which would mean

1) zoning up neighborhoods

2) make it financially interesting to convert properties and make them denser

I'll be the YIMBY broken record here. These institutional investors are suddenly interested in housing because decades of artificial constraints on new construction have created a situation where prices are rising quickly as demand outpaces supply. Don't believe me? Here's the SEC filing from one such investor:

> We have selected locations with strong demand drivers, high barriers to entry and high rent-growth potential.

Understand that "high barriers to entry" is referring to legal regimes that limit new housing.

Later, they say:

> We have selected markets that we believe will experience strong population, household formation and employment growth and exhibit constrained levels of new home construction.

These companies aren't driving up prices. They're reacting to high prices. That's what's making these markets attractive.

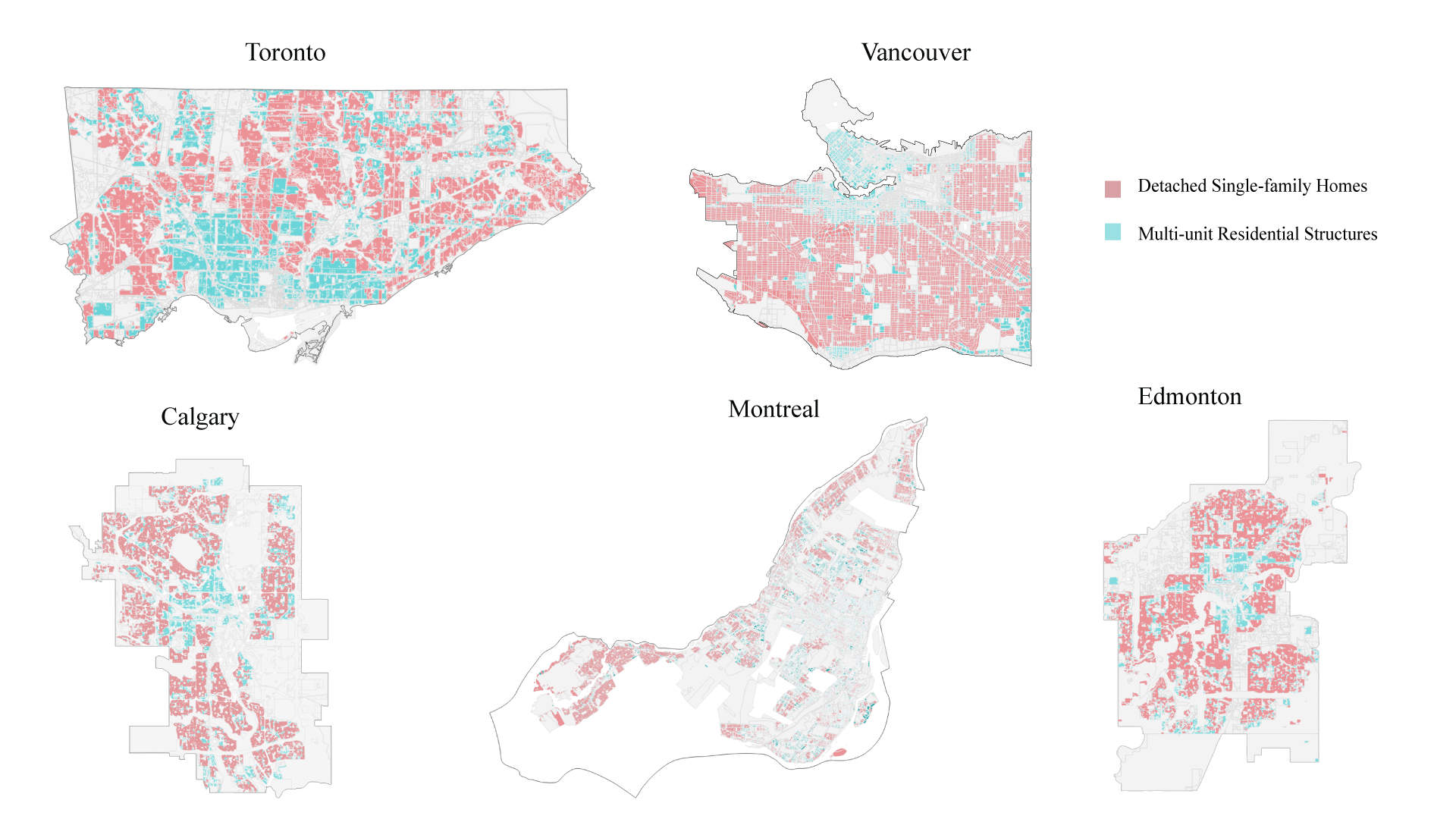

There is a global surge in housing prices. There are cities like Vancouver and Toronto where there has construction of 1000s of units has accelerated for decades, but the same crises exists.

Are you sure you aren't just thinking within the box of the United States?

I don't accept the premise. Vancouver sure looks a lot different than it did 30 years ago, right? Well, certainly the peninsula/downtown does, but most of the city is still zoned for single-family housing:

Even Vancouver isn't building anywhere near what the demand would support. If people were allowed to build more housing in Vancouver, then they would. [0]

In general, people's intuition on this stuff isn't great, for a few different reasons:

1. Status quo bias. Any change tends to look like a lot of change. This is the, "I can see three cranes from where I'm standing, so we must be in a construction boom" fallacy.

2. Illusion that concentrated change indicates widespread change. People see a lot of development in one part of town and discount that such development is prohibited in 98% of the city. (This one definitely applies to Vancouver.)

3. Failure to account for proportionality. If somebody hears that a city added 5000 units, they'll probably think that's a lot. But is it? What if we're talking about a metro area with 10 million people? It's nothing. Big numbers can end up being small numbers when the scale is large enough.

3. Failure to account for growth in demand/population. We build fewer houses than we did 100 years ago, but we also have many times as many people! So even a static supply is bad, because you have to at least build enough to keep up with growth. And since some cities have seen a sustained surge in demand for the last 2 or 3 decades without enough construction, even seemingly large amounts of recent development might mean that you're still way behind.

[0] I'm aware that Vancouver has made some progress on this. I think they're going to start allowing more duplexes and more housing near SkyTrain stops. I don't follow Vancouver that closely, so I'll just note that I'm aware it's changing.

Vancouver is the 4th densest city in North America (> 250k people). They have plenty of multi-story condos/apartment buildings, they also had these 30 years ago (as a kid growing up in Seattle, I would always marvel at how dense Vancouver was compared to our city in the south). So while sure, Vancouver could become even more dense until speculators had enough of the market (same thing happened in the late 1980s during the Japanese bubble, Vancouver got burned for it in the 90s), they are already doing plenty well comparatively.

I'm I guess what you would call a supply and demand absolutist. There's no "correct" amount of development or "optimal" level of density (wrt prices, I mean; obviously people have preferences). If you let demand outpace supply, then you should expect the available market-rate housing to increase in price. (And that's true even if you think your city is building a lot, or if you think it's already really dense, or if you think it already has a lot of people and big buildings, and so on.)

There are limits to how many people land can carry. Vancouver builds up onto a mountain, which is crazy. Yes, for some price, we could terrace the mountain or even remove it.

Vancouver is a boom bust town for real estate, now it is in a boom, it will bust eventually, just like it has many times before. There is just too much speculation going on to represent stable demand.

This is the difference between constrained and unconstrained areas. For example, San Francisco is a constrained area since it's already bounded by other cities and can only increase housing by building higher or getting rid of parks.

But the San Francisco bay is quite unconstrained, with extremely low population density and massive undeveloped tracts all over. Here, only regulation and laws prevent the cities from becoming bigger.

In general, the vast majority of people live in unconstrained areas, not constrained areas. But because constrained areas are where you get the windfall wealth from housing, people in the physically unconstrained areas clamor to make themselves legally a constrained area by making it illegal for the city to grow out.

So yes, there are limits, but these are political limits, not physical or environmental limits, and they are driven by incumbent owners with dollar signs in their eyes, not concern over nature.

Sorry to have to keep disagreeing, but we are nowhere near any geological limits in Vancouver. As I pointed out above, most of the city is still composed of single-family homes. It's not just that it's not all massive towers. It's not even duplexes or quad-plexes or small apt complexes. It's low-rise bungalows on single-family-only lots.

There's tons of space in the Vancouver metro to add density. The issue is that it's illegal.

This framing feels backwards to me - I thought the reason institutional investors see it as a valuable asset is because of NIMBYs constraining supply for them via local policy and obstruction. The institutional investors are a symptom of that policy, but the NIMBYs (and incentives that exist for existing owners like prop13) are the cause.

Real Estate scaling supply to meet demand is in direct conflict with old properties increasing in value forever. You can't really have both and we're stuck a valley of bad incentives that favor existing owners.

If we let people build housing to meet demand it would fix it, but existing owners are motivated to leverage enormous amounts of equity (and local political power) to stop any new building in order to keep property scarcity high. Their explanations beyond that are all just motivated reasoning rationalizations. Hopefully stuff like RHNA will force local municipalities to act.

I can empathize somewhat with someone who spent $3M on a crappy house being afraid of being under water from increased supply, but I have no empathy for someone who bought a $300k house 30yrs ago that's now worth millions acting to obstruct new construction.

I've seen this argument touted frequently in housing related threads and it always confuses me. Housing prices have soared over the majority of the developed world - dozens of countries[1]. Is NYMBYism and prop13 driving the housing crisis in Luxembourg? Chile? Estonia? Do you think the entire world property market, taxation and legislation is structured exactly like in the California bay area?

The whole "just zone more high rises" argument is so obviously reductive, I can't help but think it's pushed primarily by property developers and speculators.

Housing prices continuously rising to slurp up any marginal income has been studied by economists for a couple of centuries (rent extraction), and taxation solutions such as a Land Value Tax were suggested by Adam Smith himself.

I agree. Here in the Netherlands, NIMBYism isn't really a thing. If you don't own the land, you as existing resident have very little say in new developments around you, exceptions aside.

Even in this situation where almost every development is approved, it doesn't lower prices at all. The reality is that when demand is continuously high, you can never keep up with supply. It just keeps coming.

Which is what happened to my town. A small, quiet, rural town. That was 20 years ago. Now it's packed. Every inch used. Traffic jams just to get to the center. Agricultural and nature areas transformed into concrete.

Quality of life is down whilst prices just keep rising regardless. Do these people have a right to live here? YES. Do I have a right to forever preserve my old town? NO. I'm just saying NIMBYism isn't some roadblock standing in the way of an actual solution.

Yup. Essentially, housing is an in-elastic demand, and livable land is a finite resource, further exacerbated by the realities of emigration. Combined with extreme wealth inequality, it brings us to this type of dystopia - https://ssir.org/articles/entry/tackling_the_housing_crisis_...

I agree that livable land is finite, but far from scarce. The US has an enormous supply of livable land, it's just that everybody clusters into hot zones. It's obviously not easy to break that pattern, but I consider it the only real solution.

Yeah, the US is at a point where there is a lot of built environment that is underutilized because job opportunities are concentrated in other places, never mind the large amount of land that can readily be developed.

He's just wrong - in cities that have more building (Austin TX for example) the housing is more affordable.

That doesn't mean 'cheap' if demand is also increasing, but it does cause prices to be lower relative to cities that restrict supply. This is just basic economics, people twist themselves in knots to come up with reasons why the obvious supply/demand is somehow not applicable in this case.

If you allow building in capitalist markets then increased supply will reduces prices as demand is met.

It's not a question of "would it work", the point is that real-estate prices are rising in dozens of countries, and thousands of cities. Zoning is a local issue. Assuming that the reason homes prices are out of control in Santiago, Chile and in Tel Aviv, Israel for the same reasons as in San Fransisco is, well, silly.

The investors themselves agree with you. Here's one such company's SEC filing:

> We have selected markets that we believe will experience strong population, household formation and employment growth and exhibit constrained levels of new home construction.

Yeah I can’t fault the investors really, they’re just observing the world and making a bet because of the reality that is - they’re not the ones creating it.

Meanwhile the NIMBYs that are creating it blame everyone else and play victim.

This is exactly right. You show up to a local planning commission meeting or city council and it is not Blackrock there ranting about new homes being built. It's your neighbors.

OP's comment makes sense if you assume BlackRock is going to continue gobbling up properties at current prices & rates - but is there any evidence to support that?

If BlackRock doesn't continue to gobble up homes at current prices & rates - then his argument falls apart.

Does anyone have evidence that BlackRock is STILL buying properties en masse?

It is... But what are you going to do about it? Especially in the US, big business owns the politicians who can do something about it. And prop 22 shows that even if the public gets to decide, big business manages to control public opinion to their benefit.

I believe this is only going to get worse for the next couple of decades. Something major would have to happen for this to change.

So wait. Either big business owns the politicians and so nothing gets done, or people vote but they're too stupid to do it in their own interests because of big business? This sounds like the typical "the election was fair as long as I won" trope. Have you considered that maybe your opinion is just in the minority?

> Either big business owns the politicians and so nothing gets done, or people vote but they're too stupid to do it in their own interests because of big business.

> This sounds like the typical "the election was fair as long as I won" trope.

How's that? It does not sound like anything but modern American politics. Not to say it's 100% true, but it's largely true on the West Coast USA for the last 40 years...as I can only speak to what I've seen. It's a legitimate surprise when grassroots efforts are not coopted with riders/judicial nullification or drowned by propaganda.

I see what you're getting at, but Brexit is objectively shit for the majority of people, yet the majority voted for it. There are plenty more examples like it.

This article may not be a sign, but a different[1] article is a pretty decent sign

Zillow is also selling individual homes, not just this package. In their main algorithmic buying market of Phoenix they're selling individual homes, 93% of whom they payed more for than the new current listing price (and they usually do renovations before listing)

So Zillow VCs are essentially paying people to take a discount on houses in those markets. pretty sweet

I'm a 39 year renter flush with cash from 15 years of a professional job while living in austerity for the entire time. Soliciting free advice.

You sound bullish so I wanted to share five risks in the short term that have been on my mind lately:

1) Evictions now allowed in 43 states after a pandemic moratorium on them. My state allowed them October 3rd. Supply.

2) A China conflict at any point. Disruption.

3) Taxes going up on the wealthy. Disruption.

4) Rates going up to counter inflation. I want this one since I have cash and don't care if rates are 2% or 20%. While I do want the free loan (2%), I prefer the market to crash. Disruption.

5) Vaccine mandate job losses. Supply.

Given this, I've been extremely hesitant lately. So I've been trying to hold off until January for my purchase to see how correct I am, or not, on these risks impacting the market. I don't see the point in waiting years as rent drains about $18,000 a year and you have to balance that with home ownership costs. Even with repairs, I don't mind slightly overpaying if it means getting out of rent slavery. I'm also buying a home that I can nearly buy outright. I'm determined to never lose a home due to job loss, tired of working for someone else, so a 30-year mortgage isn't happening under any circumstance. 15-year only.

The one way I've been trying to protect myself is at least seeking a 15% discount off market rate for any home that I do purchase. I see that happening in my city enough that I'm confident. Eats into the 40% buffer from 2019, so I'm still at significant risk but does take some bite off in the event of a market catastrophe.

Any thoughts are welcome. Definitely would appreciate it. Whether the answer is: buy now, or, buy in 15 years. I'll try to integrate them into my view and choices.

A note on the mortgage: I understand your aversion to debt, but choosing a shorter duration mortgage can increase the probability of default, even if it shortens the time to the point that you are debt free, because for any given amount of cash reserves you have it shortens the runway you have if you lose your income.

As long as mortgage money is cheap, the most profitable course of action is to use the 30 year mortgage, but keep a large chunk of money in reserve and invest the rest in the market for the long term. And never allow yourself to not be well-cushioned.

Debt gets people in trouble when they use it to get things that put them on the edge, where losing a job causes them to miss a payment. For people who stay far away from the edge, and are good with money, it's very profitable.

Compound interest means that you will be paying a lot more money for the same house if you buy over 30 rather than 15 years.

However, for someone disciplined, taking a 30 year mortgage and paying it off like a 15 year mortgage with significant over payments is a good strategy. It means if you need to tighten your belt you can always drop down to the normal payment for a spell without so much as having to speak to the bank.

The worst option is to take the 30 year mortgage and then buy the larger house that the longer period allows you to afford.

You’re not allowing for leverage, inflation and incredibly low interest rates.

In real terms cash is losing significant money every year while assets are gaining money. Debt makes sense as long as you have a margin of safety and can multiply the impact with leverage.

IF you believe inflation will be significant over 30 years say, and can lock in a low rate, it is better to go with a longer term.

People use all kinds of accounting tricks to convince themselves that some purchase or other makes financial sense. Trading in their perfectly good 2 year old car for a brand new one, buying on finance when they could buy a cheaper one outright. I'm sceptical that it ever pays off that way.

It's not an accounting trick; it's historically low rates. At the beginning of 2021 would you rather have paid 350k cash for a house or taken a 30 year mortgage and invested the remaining 80% (after a 20% down payment) into the sp500? Your house might be up around 10-25% depending on the market making your 20% stake worth more. and your 280k cost-basis that you invested would be worth 350k. You'd have already earned your down payment back before the end of the year.

If you think the return of your investments will >= 3% mortgage rates then you're losing money by not taking on debt (albeit with a bit of risk).

If instead of buying the house cash I put it all into bitcoin at the begining of the year I'd now have enough to pay off the mortgage, the early repayment fee and have change to spare.

This being the utter fucking fallacy of hypothesising with the benefit of perfect information.

Personally I wouldn't touch bitcoin, nor do I consider it an asset. Returns on stock investments are historically high for the last couple of decades it's true, but if you take the average of say 5% a year, it's still much better than putting that money into a mortgage, when you can borrow the money over a long time period at < 1% (as in the UK for example), or even at 3%.

It's not a trick, it's simple maths. It certainly doesn't always work, and there are risks involved, so not everyone will agree on the right decision, but there is clearly a path where borrowing money to pay for a large asset makes sense.

No. I wasn't suggesting investing to pay off the mortgage (endowment mortgage), but investing as an alternative use of funds compared to paying off a debt held at low interest rates in a rapidly depreciating currency.

Imagine a more extreme example:

Interest rates 0.1%, Inflation 10%, 30 year term, leverage meaning your 50k becomes say 500k invested.

Now it makes sense to take on as much debt as you can get over say 30 years, and to put off paying it as long as possible, because even after a few years the payments will be quite minor compared to your inflating income, and at the end of the 30 years the debt you have left and the interest payments on it will be trivial compared to your income.

> for someone disciplined, taking a 30 year mortgage and paying it off like a 15 year mortgage with significant over payments is a good strategy.

This is the worst of both worlds. You pay the interest penalty of a 30 year, with the payment of a 15 year (well, slightly more). The interest difference between a 30 and 15 year mortgage is about 30% (2.x% v 3.x% APR).

I did a 15 year mortgage, then refinanced it every 12m or so ($250 each time), resetting the payments back to 180 months each time. That way, I get the interest savings of a 15 year, which is significant, and each refinance makes your payment quite a bit lower because a 15 year loan actually pays back principal. After six years, my mortgage will be the same as it would have been if I originally got a 30 year, but it will be paid off in 21 years instead of 30.

There's a risk interest rates rise, or I lose my job and can't refinance. But so far, so good. And honestly, my mortgage now is so close to what it would have been with an original 30 year loan that it doesn't even matter if I can never refinance. The hardest part was the first two years.

Depends on how much better the same amount of money would perform if invested in an index fund. It could be more profitable to throw the difference in monthly payments into a vanguard account instead of a higher 15yr monthly payment.

Personally my view is exactly your second point: Buy small enough that you can consistently put $x extra each month against the principle + one full extra payment each year. It's a good middle ground to maintain flexibility

And absolutely-- buying the biggest you can fit into monthly expenses may even seem responsible: "I'm not living beyond my means!" but is a razors edge of risk for unanticipated expenses or more significant life disruptions.

This was the approach that made the most sense to me.

Purchase a house where you can afford the 15-year fixed mortgage, but take out the 30-year fixed mortgage. Pay it off as if it were the 15-year fixed (ensure that your loan has no penalties for prepayment or extra payments, and that 100% of extra payments go toward the principal).

If things go smoothly for you, you’ll pay a marginal amount of additional interest (because your % will be higher as a 30-year than a 15-year). However, if you run into cash flow issues, you have a good amount of reduction in mortgage payments that you can make while keeping the bank completely satisfied.

I agree that produces a better expected return, however the downside-risk from a bad outcome is worse for me than the expected upside gain.

Essentially, I don't expect my overall happiness and satisfaction to be linearly correlated with my finances, and I expect that non-linearity to be such that I'd rather be more risk-averse in such a way that I have to give up some of the potential gain.

If there were a world where I could _guarantee_ the avg. stock market return, then I'd of course take that offer, but sadly such guaranteed returns only exist in the form of scams and ponzi schemes.

A better strategy is to use the 30 year, and then invest the monthly difference in the market. Why pay down long-term funding of 3.25% cost of money and lose out from a long-term market return of 7%?

You're right about the compound interest, but compound interest can work for you as well.

The answer to this dilemma is to have an offset mortgage. Your savings offset the amount borrowed, and you only pay interest on the difference. Once you've saved enough to cover it, you pay no interest.

Huh, I just assumed that the US would have any financial instrument that was available elsewhere. I guess the same US statutory intervention into the mortgage market, that makes long fixed-rate mortgages possible, also makes it difficult to have custom mortgage instruments?

Fiscal cushion. If an emergency comes up, rather than having no money to pay for it, you instead can cover it, and just pay a little extra each month going forward until you recover.

I haven't done it for a while but when I last compared 15 to 30 year rates the interest was outrageous, pure usury, for the 30 year. But that isn't my main motivation to sticking to a 15 year, it's just a mechanism to limit how much I can borrow and spend. It caps me at a reasonable amount without me having to think about it, while granting a lower interest rate. It just nicely lines up with an amount that my spouse or I can afford with even one job, or a very basic low paying job. I'm definitely doing what you're suggesting and staying away from the edge.

True, with a 30 year it looks like you're paying a lot of interest, and in nominal terms (i.e., the total amount during the loan), you are.

But consider a thought experiment where you could borrow $1m at a low rate of interest, suppose 3%, from a generous lender who requires no collateral and requires an amortizing repayment. You take the $1m and reserve, say, $100k in "no-touch" cash (your cushion) and invest the remainder in the market, and suppose that the market returns an average of 7% over the long run.

In this scenario, you obviously pay much more interest than not taking the loan. The interest you pay is nearly $500k, which sounds like a lot - almost half the loan! Yet you make a tidy profit over 30 years: after paying back the loan, you have a portfolio worth over $4 million, plus the $100k reserve you still have.

While that's just a thought experiment, the math works fairly similarly for a mortgage. So long as the market returns more (over the long term - it'll be bumpy short term) than the cost of money, you will be paid handsomely for assuming lots of long-term, fixed low-interest debt and investing the proceeds.

And this leads to a second surprising conclusion: you should not pay off your mortgage. Once you've built equity, releverage the house and borrow more, so long as you take the proceeds and invest it in an instrument that will pay more than the cost of money over the long run. If interest rates rise, the math might not work.

This is bad advice for some people, because a pile of savings and investments can be a tempting target to use for luxury vehicles, or boats or whatever, and that can upset the math, although eventually you make enough with it that might be OK. But for people who can live as if those investments were illiquid, it's quite a rewarding path.

And for some people, the psychological value of living in a house with no mortgage exceeds whatever financial gains come from continuing to pay for a mortgage. And while there's nothing wrong with that, it does come at a stiff financial cost.

I'm 45 and in the same boat as you ... except I've been waiting for a crash since 2016. I also made the mistake of keeping my cash in very cautious investments (and out of the SP500) ... thus missing the most historic bull run of my lifetime.

Regardless though, as a result of working at a successful unicorn and selling a lot of my equity on the secondary market, I ended up benefitting from the Fed's insane money printing anyway (the prices offered for my equity doubled and doubled again in 24 months).

I'm now sitting on a pile of cash. I invested a small amount (about 25%) into stocks (mostly REITs and dividend yielding stocks), but the rest I left in cash with the hopes of buying a home without debt (I can always take out a mortgage later to invest).

But the homes just keep increasing in value. The homes I looked at in 2016 in the Bay Area that were 600K are now 1.5M and up. I took my family out of the Bay Area into the Sacramento area, and even here houses have gone up 30% in the last year. Houses that were 800K are now going for about 1.2M.

But I'm still being patient. Now we're looking to leave the state entirely. I could buy a home here, but I'm looking at the economics for someone who is entry level or working a blue collar job (or being a teacher or caretaker), and I realize I don't want to live here. Apart from housing, I also have to think about what kind of teachers my kids will have, what kind of chefs will be at resteraunts, etc. A California that is unaffordable for everyone but me is a lame place to live.

After checking out Texas, Colorado, and Florida, we've decided we'll get way better value for our money, in terms of lifestyle for the family if we leave. California is bad and only getting worse.

You likely have a lot more money than I do, from what you said. I did live in a couple of major cities in Texas over the course of 5 years. I'd recommend the Dallas area. Easily one of my favorite areas in the country, especially for someone starting off. Doing it all over again, knowing what I know now, I might have moved there long ago and stayed. It has also exploded though, but probably nothing near CA proportions. I also like Washington State but have only visited once. I took multiple trips to Oregon in consideration of moving there, but declined in the end. CA is where I'd live if money is no object.

I share your holistic view, I don't want everyone around me suffering and acting tense. Its been that way in most of the country for a couple of decades now. A lot of people must really enjoy that, but I don't really see a true benefit to holding everyone down in such a way. To get a fairer society means less profits for employers so there's a lot of effort to contain those costs. My spouse is a teacher so I know what you mean, though teachers are fairly compensated where I live for sure. She makes more than I do with better benefits by a longshot. Most public school teachers in big cities are bad because the families/students are bad, and they have no authority to discipline them. Most teachers that care don't last and go teach for less money in the suburbs.

I'm in Chicago and while dangerous in 80% of the city, if you lived in the suburbs and don't mind winter, I've never known anyone that doesn't like it here. It's my favorite city in the country, it's the only city that the times I've driven out to move or visit elsewhere that I felt heartbroken. The only other place I've lived where I felt that way was France. I've lived all over and multiple countries on top of it. Crime and undesirable weather for most people keeps costs down here. I like Florida but it's such a diverse state that each area needs examined by itself. Just some thoughts.

My thoughts on buying for you are the same for me: at least wait until January. There's just too many near-term risks. My conclusion has been if things are still the exact same as today in Q1 2022, then go ahead and buy, my crystal ball is broken. That said, I'm deal hunting so if I can get anything for 15% off going rate or more, I'll probably just do it. I'm looking at homes that are in blue collar neighborhoods.

I agree with most of what you've said, but I think the core issue of affordability is not dependent on private enterprise profits. I think the core issue in California is that its so difficult to build homes in high density, and NIMBYs prevent new development everywhere, creating more and more sprawl as people move ever out of the range of existing NIMBYs to form new towns, where they in turn become NIMBYs.

If California would allow anyone to build an apartment complex nearly anywhere (as Minneapolis does in many neighborhoods) then there would automatically be more housing, and more affordable housing for blue collar workers and entry level workers. Instead, we have so many neighborhoods where each house is forced to be on .25 acres, or .15 acre, with forced single family occupancy. Affordability is a construction, zoning, and permission problem in California.

And that high expense for housing then trickles up and makes everything more expensive from child care to healthcare to services ... as everyone has to pay workers ever more just so they can get a roof over their heads. People are making $25/hour with no college degree and feel poor.

That's interesting. I've never lived anywhere where that's a problem, at least not to that degree. The places I've lived have low costs of living with the wage disparity holding most people down. A truly urban city where half the people are in a high rise, like myself, has its problems too. Which is what the NIMBYs are worried about I would presume. Tough to scale transportation and everything else around it. It really takes one of the older cities that were designed from nearly day-one to be densely populated. Everything is already in place. For example here all the roads are mostly perfectly square making for efficient movement and trains are the heartbeat of the city.

I'm a mid 30s renter also flush with cash, living in a high COL area.

I have found a happy (to me) medium - I invest all of it diversified across low to high risk assets (muni bonds, i bonds, tips, mREITs, dividend stocks, stablecoins, growth stocks), and at this point just the interest/dividends (NOT counting unrealized gains!) almost cover even my crazy rent (3500/month, for the house we are renting which is valued at about 1.5m). I just don't have the time or the energy for a house. Also a house doesn't MAKE anything other than provide shelter. Psychologically it doesn't make much sense to me to "invest" in a single house, tied to one area, such a large % of my networth. My friends bought houses recently, and even the "flips" turned out to be fixer/uppers. The supply is so bad right now you can really get burned.

Once the supply improves - and really this means most of the government distortions disappear, I would reconsider. By government distortions i mean specifically 0) stimulus checks 1) extra unemployment (bonus monthly $, extra time, and expanding benefits to people that would not have otherwise been covered) 2) mortgage forbearance programs 3) student loan forbearance 4) super low rates. i agree at one point these distortions were necessary when we were all hunkered down and hospitals were being overrun, but we are far from that these days.

Personally I went through a lot of the same considerations and the indecision and flip flopping got quite tiring.

Eventually I just simplified things. Living in a property you own gives so much more for your money compared to what one could afford at the same level renting. And on a long enough timeline crashes have had minimal impact. Many of those disruptions would affect the financial markets too so unless you’re extremely conservative leaving the money in stocks is not very safe either. I’m not renting for another 5 to 15 years with a small place and a nosey landlord jacking up rent regularly. So I bought.

>Living in a property you own gives so much more for your money

This isn't true everywhere. Prop13 in California for example means that a long-time owner can rent out a property at below market and still make money since they're paying near-zero property tax. Both the renter and landlord come out ahead.

I bought back in 2014. Ultimately the question I asked myself was: would I rather have a house in a place I wanted to live but overpaid for, or would I rather wait and get priced out of the place I wanted to live?

Ultimately I chose the former. Because at the end of the day, a house represents shelter to me. And roughly speaking, shelter is fungible. If the value of my shelter goes up by 50%, the value of the other shelter around me goes up 50%. If it goes down by 50%, so does the shelter around me. So buying into the market gives me a foot in the door to, roughly speaking, be able to move to similarly desirable dwellings regardless of where they are.

This is obviously a bit simplistic, but I think its a fair way to look at it.

1) A large increase in evictions will mostly affect the rental market. There would be some single family home rentals affected, but mostly it would affect apartments.

A lot of homeowners who needed help during the start of the pandemic were able to get a forbearance on their mortgage. Thus, there was not a huge increase in foreclosures and instead people just had extra payments tacked onto the end of their mortgage.

3) If anything, wealthy homeowners are getting a tax break. Congress is considering a repeal of the SALT deduction limit, which helps homeowners.

5) The number of people who were fired or quit due to mandates has been very small.

What's your dilemma? If you're gonna live there for 10 years, get a large utility out of the house in general and also owning your own place, then just go for it.

My dilemma is balancing inflation risks through all this increased government spending, with short-term market timing. I think that these risks are more likely than ever, and imminent.

On the inflation risks. I really wish the Democrats would cancel all their ideas about child care and what not, and just shift the tax burden from the working class that punch a clock, to the investment class that live off of IRS-defined unearned income. So much easier, simpler, doesn't engage in designing society, rewards working, helps the economy more than anything else you could do through increased spending, and would be far more popular. But that's an aside.

The specifics of your aside aren't especially interesting here, but they are quite important to you before making such a large investment. My time machine's just as good as yours, and anyone that claims their's is any better is trying to sell you something. Risks is inherent in everything. If I were trying to sell anything "rock solid" in Feb 2020; it's possible time would have proven that to be a total lie.

If you have a great mistrust of the future, then there's never going to be a good time to buy a house. If you think politicians are going to mess things up yet again, buying a house is foolish. Hanging off every word the next three or four presidents make is going to make your heart sink and your blood pressure rise on bad news, and curse the name of whomever convinced you to buy an millstone of a house to hang around your neck.

If, however, you're convinced that buying a house (for you to live in, not as part of a basically-liquid REIT) is your path to financial freedom, then when the refrigerator or other large appliance breaks, that's just part of owning a home, and you'll relish in picking the one you want.

How do you want to live for the next few years? (One thing to keep in mind is that houses can be sold before the full 15-30 years is up, which may be advantageous, depending on your finances.)

I definitely have a great mistrust of the near future. It just seems pretty ominous right now. We'd be lucky to have mere stagnation, but I'm afraid these "bad times" are about to be made to look like child's play soon, by at least 2026 and likely sooner.

You raise really good points. Insightful, like many of the responses here. My main thought in reading is this is why I'm buying as cheap as home as I can that is functional. My strategy is just to buy the cheapest home that I'm happy with. If things go to hell, and I really don't have much to lose with the anchor around your neck that home ownership is. If the fridge breaks that's annoying, but I've been renting a long time, few to no landlords want to spend a dollar anyway. They don't lose so owning is the ticket to financial freedom, even if it's not a money maker and merely a way to get expenses down to taxes + utilities. Which is how I see it.

I'd say number 2 is a long shot. Political risk is not terribly simple. Eg I worked for a firm that thought the Iraq war would mean oil would rocket and markets crater, didn't go down that way. Point is even if the thing you think will happen happens, the effect is not as obvious as you think. More examples are the monthly NFP figures, you might naively think job losses means economy is doing badly, thus market goes down. But it's rarely that clear.

4 you have to ask yourself about real rates, not nominal rates. Yes you want to get paid interest, but you also have a loss on inflation. Also, you pay tax on nominal but you don't get a credit on inflation.

What you really want to think about is whether rates will get so high that people can't afford to refinance, and are thus forced to sell.

As sad as it sounds, you may want to look into that forced seller thing. When someone hits hard times, it gets even harder due to them having to sell at a loss compared to the market, which for you as a buyer is straight up money in your pocket. See about your local foreclosure markets, I think a lot of them might still be done in an old fashioned show-up-in-real-life and shout way. Depends on where you live.

Finally, it's good to list risks as you do. The big question though, is always whether the market already reflects your thoughts.

This takes a bit more patience though. They can drag on for a while as the bank & "owner" possibly reconcile or the owner fights things tooth & nail. These deals tend to fall through a bit more than traditional sales. Given patience though, you can get a good deal: Banks don't want to be in the business of actually owning houses & their carrying costs, so they generally sell at a market-clearing rate instead of waiting for the best possible offer.

2 is not only a long shot but it's also not like if there were a third world war there would be some asset classes that escaped unscathed. If China went to war and that somehow crashed real estate prices, it's not like stocks would be soaring.

My scenario isn't meant to be WW3. It's just a conflict over Taiwan, presuming that it doesn't spiral into WW3. WW3 changes everything in such ways, my home ownership doesn't matter. Good chance my city is bombed and I die. What I'm focused on is the chance of a temporary dip in the market as I'm interested in buying in the short term (12-24 months).

How into the geopolitics of China-US relations are you? I ask because my reason that we're at high risk for a conflict and now low over Taiwan is that China just upgraded their navy, while we have a refresh going on right now. Once that investment is complete China will have essentially the window closed on any hope of winning the conflict. They have to move relatively quickly to have a realistic chance at taking over Taiwan, if US determination is resolute in stopping them at least. It could happen at any time.